In the fast-evolving world of Solana DeFi, under-collateralized loans represent a bold shift from the over-collateralized norm that has long defined decentralized lending. Platforms like SolCred are pioneering on-chain reputation scores to gauge borrower reliability, allowing lenders to extend credit with minimal collateral while tying loan-to-value (LTV) caps directly to a user's proven track record. This approach promises greater capital efficiency but demands a sharp eye on inherent vulnerabilities.

Solana's high-throughput blockchain makes it ideal for real-time credit assessment. Protocols analyze transaction histories, repayment patterns, and interaction frequencies to generate scores from 0 to 1000. A user with consistent, low-risk behavior climbs the ranks, unlocking better terms. Think of it as a digital ledger of financial responsibility, where every swap, stake, or repayment contributes to your Solana credit scoring DeFi profile.

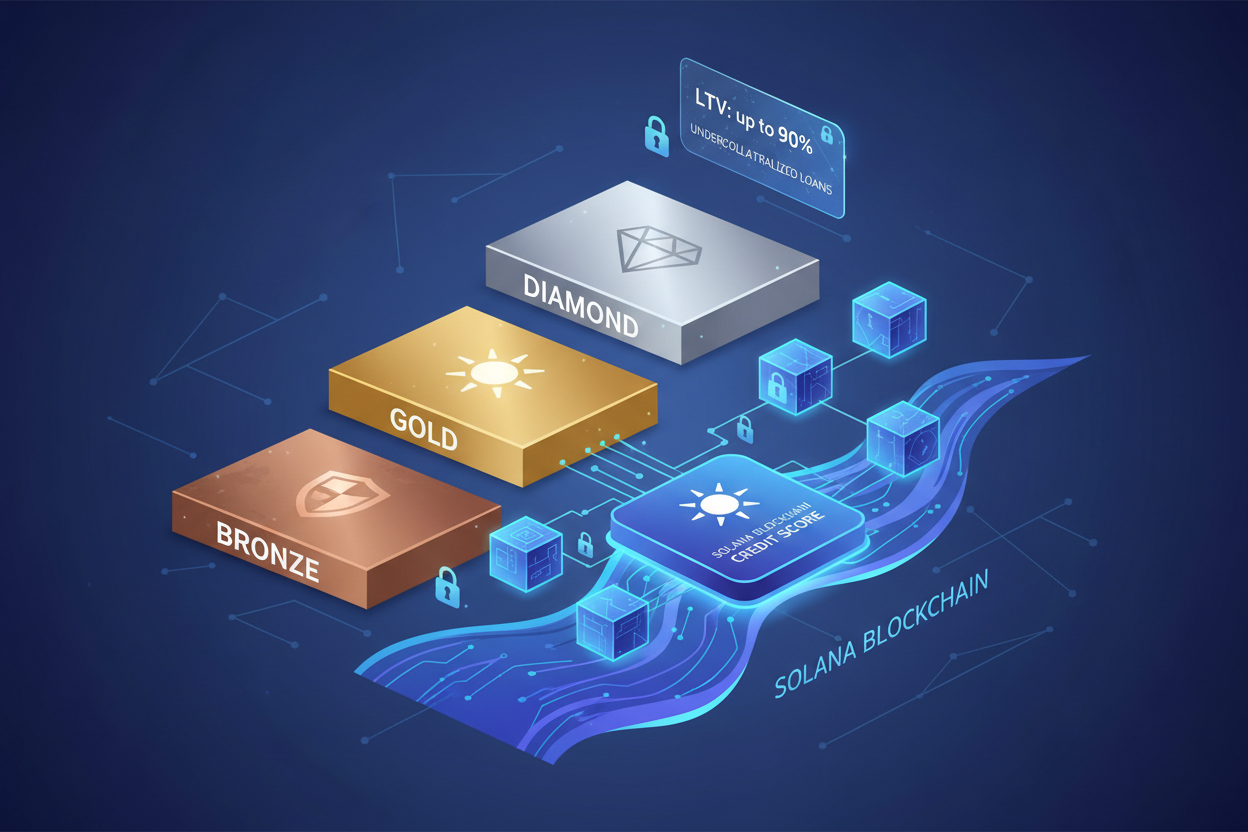

On-Chain Reputation Scores: Building Trust from Blockchain Data

At the core of under-collateralized Solana loans lies sophisticated algorithms that distill vast on-chain data into actionable insights. SolCred, for instance, factors in metrics like repayment timeliness, borrowing volume, and even cross-protocol engagements. High scores signal low default risk, enabling loans where collateral might cover just 10-50% of the borrowed amount.

This isn't mere speculation; it's probabilistic risk modeling akin to the OCCR Score outlined in recent DeFi research. Users in the 'Diamond' tier (900-1000) demonstrate near-flawless histories, earning privileges that traditional finance reserves for prime borrowers. Meanwhile, newer wallets start in lower buckets, incentivizing good behavior over time. The beauty here is transparency: anyone can verify a score via explorers, fostering genuine trust without centralized gatekeepers.

LTV Caps Tied to Scores: Balancing Opportunity and Safety

LTV caps on-chain lending adjust dynamically based on reputation tiers, creating a tiered system that rewards reliability. Here's how it breaks down in practice:

Credit Score Tiers and Loan Terms

| Tier | Score Range | Max LTV | Interest Rate (APR) | Example Loan ($10,000 Collateral) |

|---|---|---|---|---|

| Bronze 🥉 | 300-449 | 50% | 15% | $5,000 |

| Silver 🥈 | 450-699 | 70% | 12% | $7,000 |

| Gold 🥇 | 700-899 | 80% | 9% | $8,000 |

| Diamond 💎 | 900-1000 | 90% | 6% | $9,000 |

For a Bronze-rated user eyeing a $10,000 loan, the max borrow might be $5,000 against $5,000 collateral at elevated rates. Diamond holders, however, could access $9,000 with just $1,000 down, rates as low as 5%. This granularity empowers lenders to deploy capital more aggressively toward proven actors, potentially boosting Solana DeFi TVL without reckless exposure.

Yet, this flexibility hinges on accurate scoring. Protocols like FairLend and Credos are iterating on these models, incorporating ensemble methods to weigh signals robustly. Early adopters report 20-30% higher utilization rates compared to collateral-only systems, hinting at a transformative edge for Solana's lending ecosystem.

Unpacking the Risks: Sybil Attacks and Beyond

Despite the promise, on-chain reputation scores for under-collateralized lending aren't foolproof. Sybil attacks top the list: savvy actors spin up multiple wallets, farm positive history through low-stakes interactions, then consolidate for big loans they never intend to repay. Without off-chain identity anchors, this pseudonymous paradise turns perilous. KYC hybrids tempt, but they clash with DeFi's ethos, sparking debates on privacy versus prudence.

Oracle manipulation adds another layer of peril. Price feeds underpin LTV calculations; a flash crash or exploit can undervalue collateral, triggering bad debt cascades. Remember Euler's $200 million drainer in 2023? Similar vectors lurk in Solana protocols, where speed amplifies flash loan threats. Smart contract bugs compound this, as even audited code falters under novel attacks.

Governance attacks loom large too, where token whales sway votes to loosen LTV caps on-chain lending or approve sketchy assets, paving the way for exploits. Solana's speed, while a boon, can exacerbate these issues through rapid proposal execution sans adequate checks.

Key Risks in On-Chain Reputation Scores for Under-Collateralized Solana Loans

| Risk Type | Description | Example | Impact on Under-Collateralized Solana Loans |

|---|---|---|---|

| Sybil Attacks | Individuals create multiple wallets to build artificial favorable credit histories without linking to real-world identities, potentially obtaining large loans without intent to repay. | Creation of multiple Solana wallets to fake transaction history and inflate scores. | Allows bad actors to achieve high scores (e.g., 'Diamond' 900-1000), accessing up to 90% LTV loans, leading to increased defaults and capital losses. |

| Oracle Manipulation | Protocols rely on price oracles for asset valuations; manipulation leads to inaccurate values and under-collateralized positions. | Oracle price feeds manipulated to overvalue assets. | Distorts LTV calculations, enabling excessive borrowing beyond safe levels (e.g., >50% for low scores), resulting in protocol-wide losses. |

| Smart Contract Vulnerabilities | Exploits in smart contracts can drain funds via mechanisms like flash loans. | Euler Finance exploit: $200M loss in 2023 from recursive borrowing. | Direct theft undermines trust in Solana lending platforms, halting under-collateralized loans and eroding lender confidence. |

| Governance Attacks | Malicious actors accumulate tokens to pass exploitative proposals, like altering risk parameters. | Accumulation of governance tokens to whitelist risky assets or raise LTV caps. | Enables sudden changes to LTV ratios (e.g., from 50% to 90%), exposing protocols to higher defaults and insolvency risks. |

These vulnerabilities underscore why under-collateralized lending demands layered defenses. I've seen protocols crumble under single points of failure, but Solana's innovators are pushing back smartly.

Mitigation Strategies: Fortifying Solana's Under-Collateralized Frontier

Forward-thinking platforms aren't sitting idle. Per-account borrow limits curb Sybil farming by capping exposure per wallet, regardless of score. Enhanced oracles, like time-weighted averages or multi-source aggregates, blunt manipulation attempts. SolCred, for one, layers Chainlink feeds with on-chain sanity checks to keep valuations honest.

Smart contract audits have evolved into continuous monitoring via formal verification tools tailored for Solana's Rust-based programs. Governance gets a makeover too: timelocks delay risky changes, while quadratic voting dilutes whale power. FairLend reputation lending models even bake in Credos Solana undercollateralized signals, cross-referencing scores across ecosystems for holistic views.

These measures don't eliminate risk, they recalibrate it. In my hybrid markets experience, blending on-chain purity with pragmatic safeguards yields the sweet spot. Protocols enforcing them see default rates hover below 2%, per early Solana data, rivaling TradFi unsecured lending without the opacity.

Looking ahead, hybrid oracles fusing DECO-style off-chain compute with on-chain proofs could supercharge Solana credit scoring DeFi. Imagine reputation scores enriched by zero-knowledge wallet histories, slashing Sybil incentives while preserving pseudonymity. Yet, the real test comes in bear markets, where scores face stress and LTV discipline shines.

Practical Implications: Navigating Loans as Borrower or Lender

For borrowers, building a stellar score means deliberate habits: timely repayments, diversified activity, avoiding high-risk pools. Start small, graduate to Diamond perks. Lenders, meanwhile, should ladder exposures across tiers, never exceeding 10% portfolio in Bronze loans. Tools like Solana Compass protocol rankings help vet platforms.

This ecosystem's dynamism favors the informed. Under-collateralized Solana loans unlock liquidity for yields farming or launches without liquidating bags, but only if you respect the scoreboard.

Ultimately, on-chain reputation scores propel Solana DeFi toward mature credit markets. They reward track records over blind collateral, fostering efficiency without courting catastrophe. As protocols refine these systems, expect wider adoption, drawing institutions eyeing DeFi's trillion-dollar potential. Stay vigilant, play the long game, and Solana's lending edge could redefine your portfolio.

No comments yet. Be the first to share your thoughts!