In the fast-evolving landscape of decentralized finance, onchain risk scores are rapidly reshaping the way under-collateralized crypto lending is structured and accessed. Historically, DeFi lending has been dominated by over-collateralized models, requiring borrowers to lock up assets worth more than their loan amount. While this approach mitigates lender risk, it also creates a substantial barrier for users without significant crypto holdings, effectively sidelining vast segments of potential borrowers and stifling capital efficiency.

From Over-Collateralization to Data-Driven Credit

The introduction of under-collateralized lending platforms marks a paradigm shift for DeFi. Instead of relying solely on collateral as the primary safeguard, these platforms harness decentralized identity credit scoring and transparent onchain repayment history to assess borrower risk. This model unlocks new opportunities for users who may lack substantial digital assets but have demonstrated reliable repayment behavior or positive engagement with DeFi protocols.

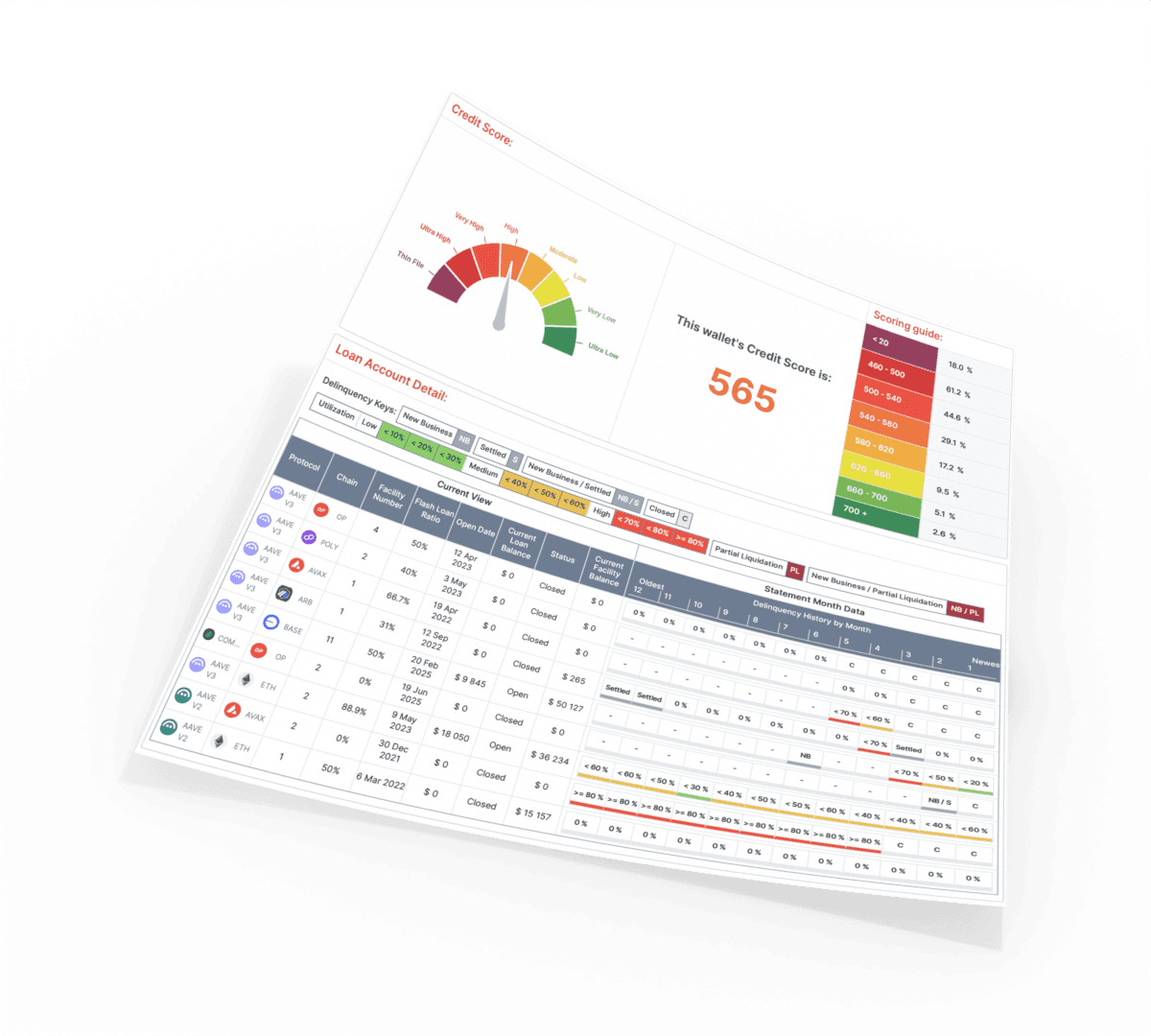

Protocols like Cred Protocol exemplify this trend by developing decentralized credit scores tied directly to wallet addresses. These scores analyze a borrower's transaction history, protocol interactions, and even liquidation events to estimate the likelihood of repayment or default. Notably, this approach is not about identifying individuals but rather building a robust financial reputation based on verifiable blockchain activity.

The Mechanics of Onchain Risk Scoring in Practice

Onchain risk scores aggregate a wealth of data points from blockchain activity: frequency of borrowing and repayment, participation in different DeFi platforms, wallet age, and even patterns that may indicate fraudulent behavior. For example, RociFi has launched an under-collateralized credit protocol on Polygon that assigns borrowers to different lending pools based on their assessed risk profile, balancing fraud risk management with capital accessibility (source). By leveraging these granular metrics, platforms can calibrate collateral requirements dynamically instead of enforcing rigid thresholds across the board.

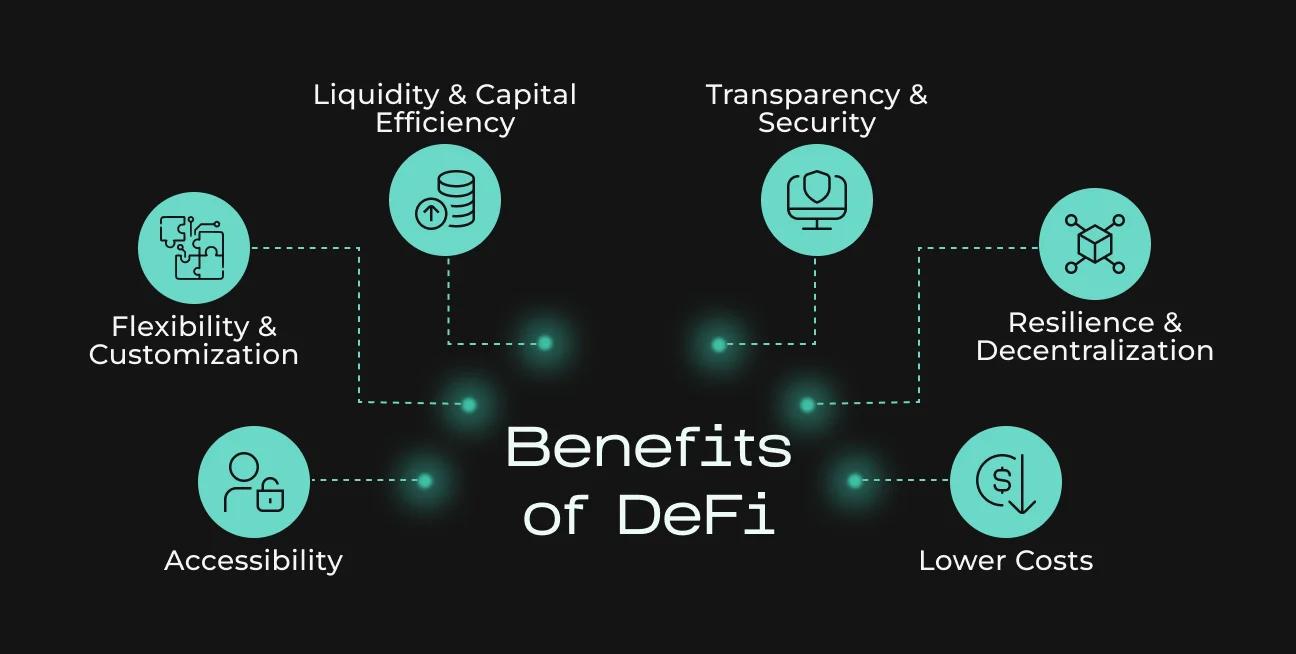

Key Benefits and Challenges of Onchain Risk Scores in DeFi Lending

- Expanded Access to Credit: Onchain risk scores allow platforms like Cred Protocol to offer under-collateralized loans, enabling users without substantial crypto holdings to participate in DeFi lending and broadening financial inclusion.

- Enhanced Capital Efficiency: By reducing or eliminating the need for over-collateralization, protocols such as RociFi improve capital utilization, allowing borrowers to access more funds with less locked collateral.

- Data-Driven Risk Assessment: Onchain credit scores leverage transparent blockchain data—such as transaction history and protocol interactions—to create objective, auditable risk profiles for borrowers.

- Security and Data Integrity Concerns: The reliability of onchain risk scores depends on accurate, tamper-resistant data. Vulnerabilities like oracle manipulation or Sybil attacks can undermine score validity and platform security.

- Potential for Exploitation and Fraud: Attackers may attempt to game the system by creating multiple wallets or manipulating onchain behavior, posing challenges for protocols in detecting and mitigating fraudulent loan applications.

- Ongoing Model Development: The effectiveness of onchain risk scoring relies on continual improvements to analytics and risk models to adapt to evolving market behaviors and threats.

This evolution means that users with strong crypto repayment history, but limited upfront capital, gain access to better loan terms, potentially transforming DeFi into an engine for broader financial inclusion.

Inefficiencies Addressed: Capital Efficiency and Inclusion

The inefficiency of over-collateralization is increasingly apparent as DeFi matures. Locking up more value than borrowed restricts liquidity and reduces overall yield opportunities within the ecosystem. By contrast, under-collateralized models powered by sophisticated DeFi risk assessment tools can unlock dormant capital while maintaining prudent risk controls. As noted by industry research (source), this transition is critical for onboarding underserved communities who lack legacy financial credentials but are active participants in digital economies.

This momentum is not merely theoretical, market leaders are already demonstrating product-market fit for under-collateralized loans secured by transparent onchain reputations instead of static asset reserves.

Yet, as with any financial innovation, the proliferation of under-collateralized lending platforms introduces new vectors of risk. The reliability of onchain risk scores depends on the integrity and completeness of blockchain data. Malicious actors may attempt to manipulate their onchain behavior or exploit protocol vulnerabilities, such as oracle attacks or sybil strategies, to artificially inflate their creditworthiness. To mitigate these threats, platforms are investing in advanced analytics, multi-factor risk models, and continuous monitoring of wallet activity to flag anomalies before they escalate into systemic risks.

Another challenge is ensuring privacy and data sovereignty for borrowers. While decentralized identity frameworks can provide pseudonymity, they must also protect sensitive user data from unwanted exposure or misuse. Innovations like privacy-preserving oracles (e. g. , DECO) are beginning to address this gap by enabling confidential attestation of off-chain financial information without compromising user privacy (source). As these tools mature, they will play a pivotal role in balancing transparency with confidentiality, a core tension in the next phase of DeFi lending.

What’s Next for Onchain Credit Scoring?

The trajectory for onchain risk scores is clear: as more wallets build verifiable repayment histories and protocols refine their assessment algorithms, the volume and diversity of under-collateralized loans will grow exponentially. This evolution could ultimately bring trillions in untapped capital into DeFi markets by lowering entry barriers for new participants (source). The resulting increase in capital efficiency stands to benefit not only borrowers but also liquidity providers seeking higher yields without assuming disproportionate risk.

Key Trends in Onchain Credit Scoring & Under-Collateralized Lending

- Decentralized Credit Scoring Protocols Are Gaining Traction. Platforms like Cred Protocol and RociFi are pioneering onchain credit scores, enabling under-collateralized loans by analyzing wallet activity, payment history, and DeFi interactions.

- Enhanced Capital Efficiency Through Reduced Collateral Requirements. Onchain risk assessment allows DeFi platforms to move beyond traditional over-collateralization, making lending more accessible and efficient for users without large crypto holdings.

- Integration of Advanced Blockchain Analytics. The use of sophisticated onchain analytics tools is improving the accuracy of credit risk evaluations, helping lenders better predict default probabilities and manage risk.

- Privacy-Preserving Technologies Are Emerging. Innovations such as Chainlink DECO enable confidential verification of off-chain data (e.g., bank balances), supporting secure and private under-collateralized lending.

- Growing Emphasis on Risk Management and Security. As under-collateralized lending expands, DeFi platforms are prioritizing robust risk models and security measures to address vulnerabilities like oracle manipulation and Sybil attacks.

The competitive landscape is already shifting as more platforms adopt hybrid models that combine traditional collateral requirements with dynamic risk-based adjustments powered by real-time blockchain analytics. Expect to see further integration with decentralized identity solutions and cross-chain reputation systems, expanding access across diverse digital ecosystems.

For developers and institutions considering entry into this space, robust due diligence remains paramount. Evaluating the transparency of scoring algorithms, governance structures around risk assessment updates, and mechanisms for dispute resolution will be essential to ensure long-term viability and user trust.

Building Trust Through Transparent Risk Assessment

The maturation of onchain risk scores signals a move toward a more meritocratic financial system where access is based on proven behavior rather than arbitrary thresholds or opaque criteria. As protocols continue to iterate on these models, incorporating richer datasets and more nuanced analytics, we can anticipate a future where under-collateralized crypto lending becomes both safer and more inclusive.

No comments yet. Be the first to share your thoughts!