Crypto lending is evolving fast, and the next wave is all about capital efficiency. For years, DeFi lending protocols forced users to lock up more collateral than they borrowed. This over-collateralization protected lenders but kept a massive number of would-be borrowers on the sidelines. Enter onchain risk scores: a breakthrough that lets protocols finally assess borrower risk directly on the blockchain, opening the door to under-collateralized crypto lending for the first time. If you’ve ever wondered how DeFi could scale to trillions or bring real-world credit access onto the chain, this is where it starts.

Why Over-Collateralization Holds DeFi Back

Traditional DeFi loans require users to post more collateral than the loan amount, sometimes by 150% or more. This model makes sense when you don’t know who’s borrowing - it’s trustless, but not exactly accessible. The result? Most people can’t participate unless they already have substantial crypto assets lying around.

Undercollateralized lending flips that script. By assessing user risk through transparent onchain data - things like repayment history, protocol interactions, and wallet behavior - platforms can offer loans with much lower collateral requirements. That means more users get access to credit, and lenders can deploy capital far more efficiently.

The Mechanics of Onchain Risk Scores

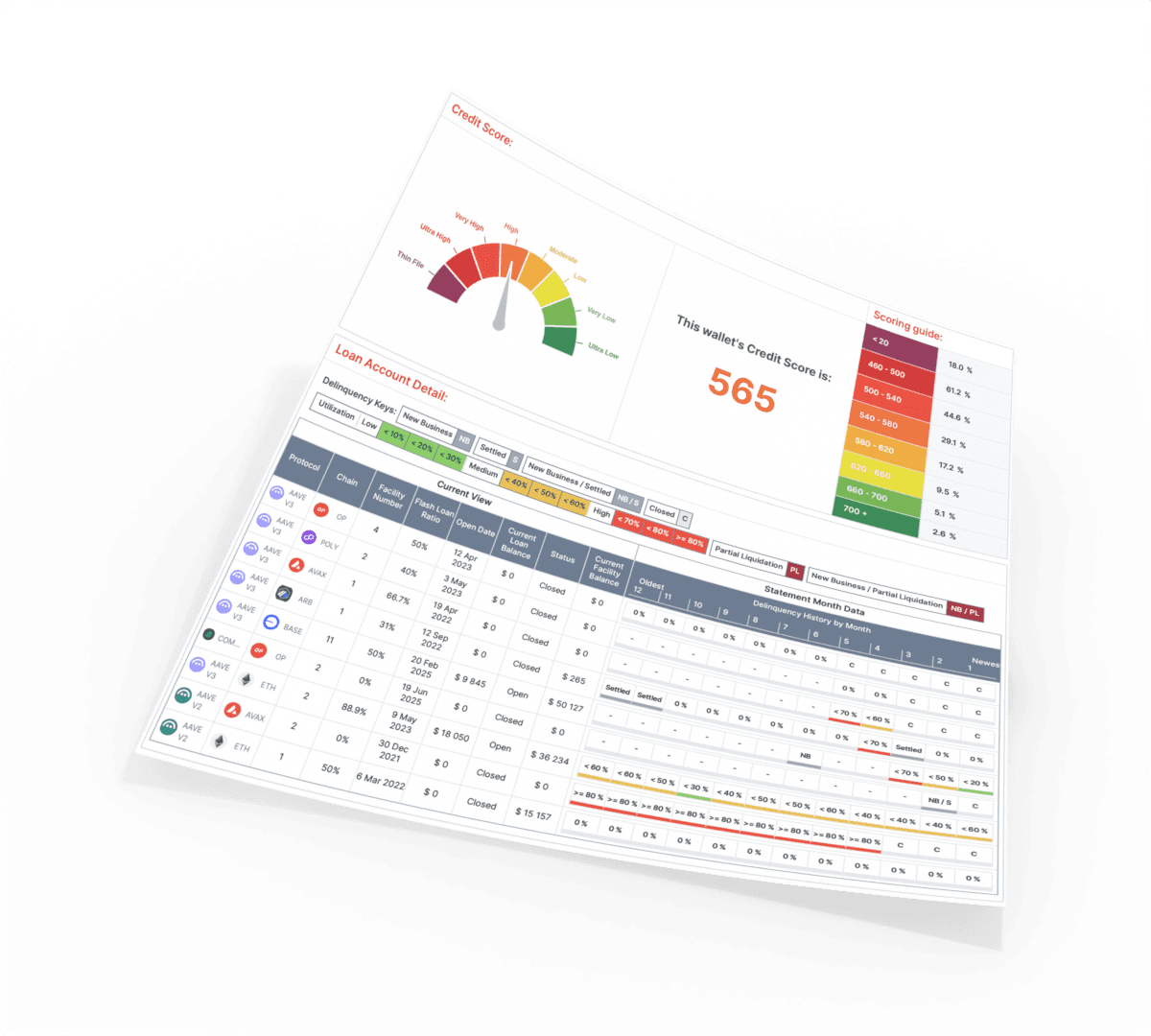

So what exactly goes into an onchain risk score? Think of it as a blockchain-native version of your FICO score - except instead of banks and bureaus, smart contracts crunch the numbers. These systems analyze:

- Wallet transaction history: Frequency and volume of transfers

- Asset holdings: Diversity and stability over time

- Lending/borrowing activity: Repayment track record across multiple protocols

- DID (decentralized identity): Optional links to offchain reputation or KYC data for extra context

The result? Lenders get a real-time snapshot of borrower trustworthiness without having to rely on opaque third parties or outdated paperwork. Protocols like RociFi are already live with this approach, using fraud databases and reputation layers to inform lending decisions (bravenewcoin.com). Others like Credora leverage zero-knowledge proofs so borrowers can prove solvency without exposing personal details (medium.com).

The Real-World Impact: More Credit, Less Friction

If you’re thinking this sounds like a game-changer for crypto credit access, you’re right. Here’s what happens when under-collateralized lending goes mainstream in DeFi:

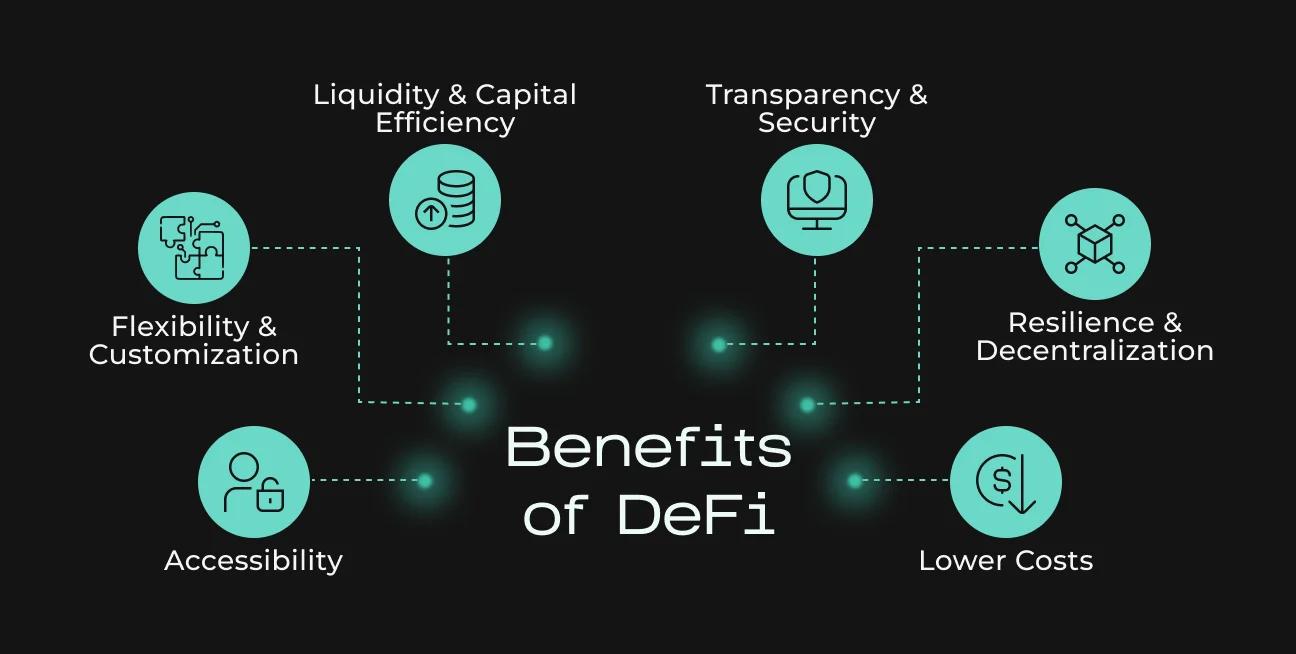

Top Benefits of Onchain Risk Scores for Under-Collateralized Crypto Lending

- Broader Access to Loans: Onchain risk scores let more users borrow with less collateral, opening DeFi lending to those without large crypto holdings.

- Dynamic, Personalized Loan Terms: Platforms like Credora and RociFi use onchain credit data to tailor interest rates and collateral requirements to each borrower’s profile.

- Enhanced Capital Efficiency: By reducing over-collateralization, capital can flow more freely, allowing lenders and borrowers to put their assets to better use across DeFi protocols.

- Transparent and Data-Driven Risk Assessment: Onchain risk scores leverage blockchain’s transparency, letting lenders make informed decisions based on real transaction history and protocol interactions.

- Seamless Integration with Offchain Agreements: Lenders can link onchain scores with offchain legal contracts, enabling real-world recourse if loans go unpaid and bridging DeFi with traditional finance.

Lenders aren’t just guessing anymore - they’re making informed decisions based on real data that’s visible to everyone. Borrowers with good repayment histories can finally unlock better rates and terms instead of being penalized by blanket requirements.

This isn’t just theory either. According to recent research from arXiv, dynamic scoring models allow protocols to adjust loan terms in real time as borrower profiles change - something impossible in traditional finance (medium.com). And because everything happens transparently on-chain, there’s less room for fraud or backroom deals.

What’s especially exciting is how these advances are already attracting institutional attention. Galaxy’s SeC FiT PrO framework, for example, is pushing the boundaries of DeFi risk assessment by providing sophisticated tools for investors to analyze protocol safety and creditworthiness. This kind of infrastructure is crucial if DeFi is going to support lending at the scale of traditional finance.

But it’s not just about big players. Everyday users now have a path to build their own onchain reputations, leveraging decentralized identity in crypto and transparent onchain repayment history to access capital that was previously out of reach. The playing field is leveling, and fast.

The Tech Behind Trust: Privacy, Oracles, and Zero-Knowledge Proofs

Of course, none of this works without robust tech under the hood. Privacy-preserving tools like zero-knowledge proofs let borrowers prove their solvency or repayment history without exposing every detail of their wallet activity. Protocols like Credora are pioneering this approach by allowing loan underwriters to verify balances and behaviors while safeguarding user privacy (medium.com).

Meanwhile, secure oracles bridge the gap between offchain and onchain data, making it possible to factor in everything from traditional credit scores to real-world legal agreements for recourse when loans go unpaid. Solutions like DECO (highlighted by Chainlink) are shaping this hybrid future where both digital and physical identities can be part of your DeFi risk profile.

Are Onchain Risk Scores Ready for Prime Time?

The momentum is real, but there are still hurdles ahead. Data quality is paramount, garbage in means garbage out, even with fancy algorithms. Protocols must also guard against Sybil attacks (where one user creates many wallets to game the system) and ensure that scoring models don’t accidentally reinforce old biases or exclude worthy borrowers.

That said, the upside dwarfs these challenges. Dynamic loan terms based on live credit assessments mean protocols can respond instantly to changes in borrower behavior or market conditions, something banks can only dream about (medium.com). And as more data flows onto public ledgers, future DeFi risk assessment will only get sharper.

What’s Next? Your Credit Moves With You

The long-term vision goes far beyond just lowering collateral requirements. Imagine a world where your crypto credit score follows you across blockchains and apps, a portable reputation that lets you borrow, trade, or even rent an apartment with nothing but your digital wallet and DID credentials.

This isn’t science fiction anymore. As under-collateralized crypto lending matures and more protocols adopt transparent scoring standards, we’re moving toward a truly open financial system, one where opportunity isn’t locked behind legacy paperwork or arbitrary gatekeepers.

If you’re a builder or investor looking to get ahead of the curve, now’s the time to dig into these emerging standards around onchain risk scores and decentralized identity in crypto. The next trillion dollars in DeFi will be unlocked not just by code, but by trust built transparently on-chain.

No comments yet. Be the first to share your thoughts!