How crypto lending affects your credit now

For years, the prevailing wisdom in digital finance was that crypto loans existed in a vacuum. Because these loans are collateral-based rather than credit-based, borrowers could pledge Bitcoin or Ethereum to access liquidity without triggering a hard inquiry or appearing on a traditional credit report. This structure removed traditional barriers, allowing users to bypass lengthy approval processes and credit score checks entirely [[src-serp-1]].

That silence is ending in 2026. The landscape is shifting as major credit bureaus begin integrating on-chain activity into their reporting frameworks. TransUnion, one of the "big three" credit reporting agencies, has started delivering traditional off-chain credit scores for individuals applying for loans on blockchain-based protocols [[src-serp-2]]. This means that borrowing against crypto assets is no longer invisible to the broader financial system.

This integration creates a new reality for borrowers. While you still don't need a high FICO score to secure a loan, the act of borrowing may now be recorded on your credit file. Lenders are moving toward a hybrid model where on-chain behavior informs off-chain risk assessments. Understanding this shift is critical for anyone planning to use crypto assets for collateral in the current year.

CeFi vs DeFi credit reporting

The way your lending activity is recorded and reported differs fundamentally between centralized and decentralized finance. This distinction determines whether your borrowing history contributes to a recognized credit profile or remains invisible to traditional financial institutions.

Centralized finance (CeFi) reporting

CeFi platforms operate similarly to traditional banks. They collect personal identification information, perform credit checks, and report loan activity to major credit bureaus like Equifax or TransUnion. If you repay a crypto-backed loan on time, this positive history can improve your FICO score. However, these platforms require strict Know Your Customer (KYC) verification and often reject applicants with poor credit histories before issuing any loans.

Decentralized finance (DeFi) reporting

DeFi protocols are built on public blockchains and rely on smart contracts rather than personal identity. Loans are secured by overcollateralization, meaning you must deposit more value than you borrow. Because there is no central entity to verify your identity or report your behavior, DeFi lending does not currently build traditional credit scores. While new initiatives like the FICO Crypto Credit Score aim to bridge this gap, most DeFi activity remains anonymous and disconnected from mainstream credit reporting systems.

Comparison of reporting models

The table below highlights the key differences in how credit history is handled across these two models.

| Model | Credit Reporting | Collateral | Identity Required |

|---|---|---|---|

| CeFi | Reports to bureaus | Undercollateralized | Yes, KYC required |

| DeFi | No traditional reporting | Overcollateralized | No, anonymous |

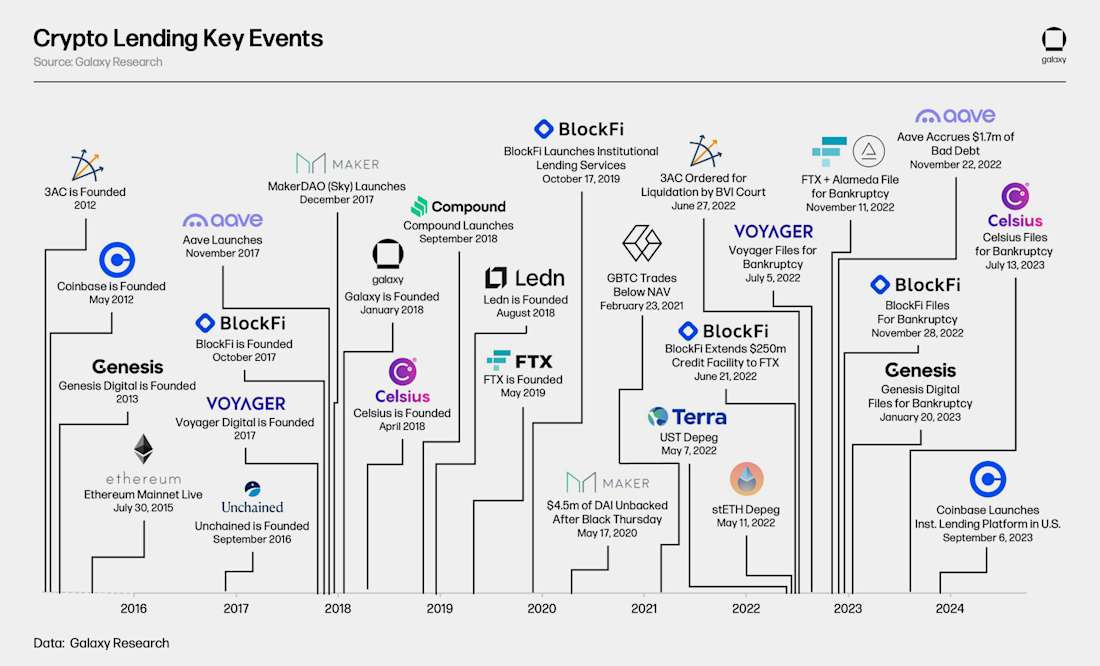

Market Size and Institutional Adoption

The 2026 crypto credit score landscape is no longer a niche experiment; it is a core component of the broader digital asset economy. As institutional capital flows into the sector, the scale of crypto lending has expanded significantly, creating a data-rich environment where creditworthiness is increasingly measurable and tradable. This growth validates the need for robust credit scoring models that can manage the volatility inherent in digital assets.

The shift toward institutional-grade infrastructure is evident in the rising valuation of crypto lending platforms and the entry of traditional finance players. According to Grayscale’s 2026 Digital Asset Outlook, the sector is experiencing a "dawn of the institutional era," with rising valuations across all major crypto sectors driving demand for sophisticated credit tools [[src-serp-6]]. This institutional adoption is not just about volume; it is about the standardization of risk assessment, which directly impacts how crypto credit scores are calculated and utilized.

Onchain credit markets are also scaling rapidly. 21Shares reports that tokenized credit funds may exceed $50 billion in assets under management by 2026, a 150% increase from previous years [[src-serp-8]]. This surge in capital has led to the creation of investment-grade vaults, further legitimizing crypto as a serious asset class. As these markets mature, the integration of CeFi and DeFi lending models will rely heavily on accurate, real-time credit scoring to manage risk and ensure liquidity.

To understand the current market context, it is helpful to observe the broader price trends of major assets like Bitcoin, which serve as the primary collateral for many crypto credit products. The TechnicalChart below illustrates the recent price action of BTC/USD, highlighting the volatility that credit scoring models must account for.

Liquidation risk and credit damage

Crypto-backed loans operate on a thin margin between access to liquidity and total loss. Unlike traditional mortgages, where home equity provides a buffer, crypto collateral is subject to extreme volatility. A sharp market correction can trigger an automatic liquidation event, wiping out your principal asset while leaving you with debt or reduced holdings.

How liquidations trigger

Lenders monitor your Loan-to-Value (LTV) ratio in real-time. If the value of your collateral (e.g., Bitcoin) drops relative to your loan, your LTV rises. Once it crosses a predefined threshold—often called the liquidation threshold—the lender’s smart contract or trading desk automatically sells your collateral to cover the loan. This process is instantaneous and non-negotiable, regardless of your personal financial situation or long-term investment thesis.

The speed of these sales can exacerbate losses. In a falling market, mass liquidations create a feedback loop: forced selling drives prices down further, triggering more liquidations. This "liquidation cascade" can erase significant portions of your collateral in minutes. For example, if you borrowed against Bitcoin at a 50% LTV and the price drops 20%, you might lose a substantial portion of your Bitcoin stack, potentially leaving you with less value than the amount you originally borrowed.

Credit reporting consequences

The impact extends beyond lost crypto. Many CeFi lenders report loan activity and defaults to traditional credit bureaus. While this can help build credit for responsible borrowers, it also means that a liquidation event or failure to repay can damage your credit score. A negative mark on your credit report can hinder your ability to secure mortgages, auto loans, or other traditional financial products for years.

DeFi protocols, while often anonymous, don’t report to credit bureaus. However, they lack the safety nets of CeFi. If you fail to repay a DeFi loan, your collateral is simply seized, and you have no recourse to negotiate or rebuild credit. The risk profile is binary: you either keep your collateral and maintain your position, or you lose it entirely with no middle ground.

2026 regulatory changes and reporting

The regulatory landscape for crypto credit scores has shifted from advisory guidelines to enforceable mandates. In 2026, investors using CeFi vs DeFi lending models face stricter scrutiny, particularly regarding tax reporting and transaction transparency. The primary focus for compliance is no longer just on holding assets, but on the granular reporting of every lending and borrowing event.

In jurisdictions like India, the 2026 tax season introduced enhanced enforcement through Schedule VDA (Virtual Digital Assets). Taxpayers must now report each crypto transaction individually, with authorities cross-checking these filings against exchange data. This level of detail applies to both centralized exchanges and decentralized protocols that have begun integrating identity verification.

For crypto credit scores, this means that on-chain activity is no longer anonymous by default. Lending platforms are required to flag high-frequency trading or large-scale lending that could indicate tax evasion. Investors should prepare for a 2026 environment where creditworthiness is directly tied to compliant reporting. A clean tax record is now a prerequisite for high credit limits in DeFi lending pools.

No comments yet. Be the first to share your thoughts!