What a crypto credit score measures

A crypto credit score is a distinct metric derived from on-chain behavior rather than traditional bureau data. While it draws parallels to conventional credit scoring, it evaluates the financial activity and behavior of users based on their digital footprint. This approach aims to bridge the gap in risk assessment, rendering DeFi lending more robust and inclusive for those without established credit histories.

The system assesses credit risk and the ability to pay crypto loans by analyzing transaction history, collateralization ratios, and repayment consistency. By focusing on verifiable on-chain actions, it provides a transparent view of borrower reliability that does not rely on centralized identity verification.

This shift allows lenders to make data-driven decisions based on actual financial behavior rather than static demographic data. It represents a structural change in lending mechanics, moving from identity-based risk models to behavior-based risk models.

Why DeFi needs on-chain reputation

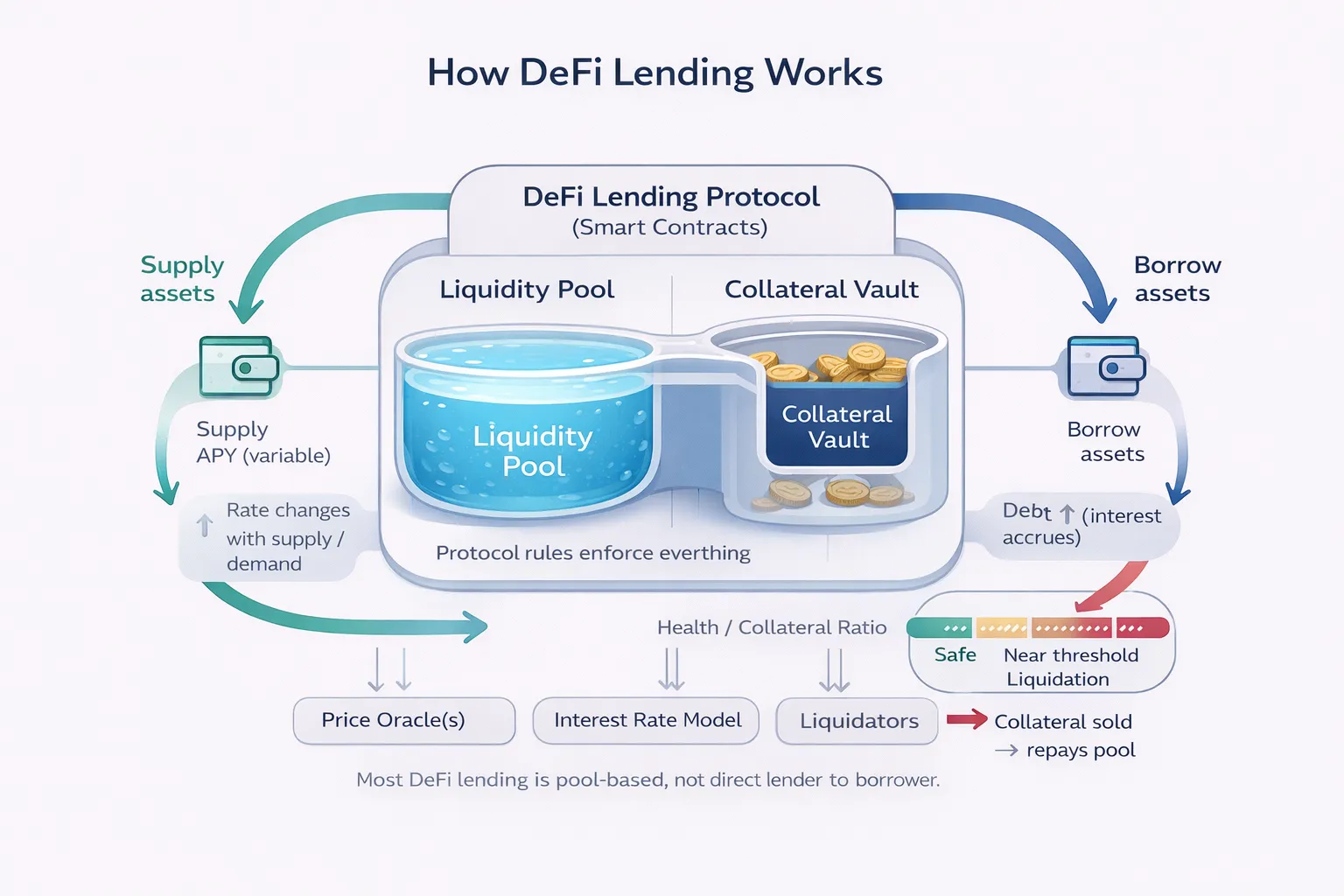

Traditional financial systems rely on centralized credit bureaus to assess borrower risk, a mechanism that systematically excludes cryptocurrency holders. For many users, assets stored in non-custodial wallets or transacted on public ledgers leave no footprint in conventional credit reporting agencies. This structural gap forces DeFi lending protocols to rely exclusively on over-collateralization, where borrowers must lock up more value than they wish to borrow to mitigate default risk.

While over-collateralization ensures protocol solvency, it severely limits capital efficiency. Borrowers are forced to tie up significant liquidity in idle collateral rather than deploying it for productive use. This model creates a friction point for institutional adoption and high-net-worth individuals who possess substantial on-chain assets but lack the traditional credit history required by legacy finance. The result is a market where capital remains stagnant, and borrowing costs remain artificially high due to the lack of nuanced risk assessment.

On-chain credit scores address this inefficiency by translating blockchain activity into a reputation metric. As noted in legal analyses of decentralized finance, this approach evaluates the financial behavior of users based on their digital footprint, rather than relying on external, siloed data sources. By analyzing transaction history, repayment behavior, and asset diversity, protocols can assign a risk score that reflects actual on-chain conduct. This allows for under-collateralized or partially collateralized loans, unlocking liquidity that was previously inaccessible.

The shift toward on-chain reputation represents a fundamental change in lending mechanics. It moves the industry from a binary model of "collateralized or nothing" to a nuanced risk-based framework. This evolution not only improves capital efficiency for borrowers but also expands financial inclusion for those operating outside traditional banking infrastructure. The integration of these scores into lending protocols marks a critical step toward a more mature and accessible decentralized financial system.

How lenders calculate risk today

Use this section to make the How Crypto Credit Scores Change DeFi Lending decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Uncollateralized loans and real rates

The integration of crypto-native credit scores is shifting DeFi lending from a purely asset-backed model to one that incorporates behavioral risk assessment. This structural change allows high-reputation users to access liquidity without posting excessive collateral, effectively lowering their borrowing costs. As noted in legal analyses, this approach aims to bridge the gap in risk assessment, rendering DeFi lending more robust and inclusive by evaluating financial activity based on their digital footprint rather than relying solely on static asset value.

This shift enables the emergence of crypto mortgage-like products, where loan-to-value ratios are determined by on-chain history rather than just collateral type. For borrowers with strong transactional integrity, this means access to capital at rates that reflect their actual creditworthiness. The mechanism mirrors traditional unsecured lending but uses immutable on-chain data to mitigate counterparty risk. This creates a more efficient capital market where liquidity flows to users based on proven reliability.

To understand the practical impact, it is essential to compare the mechanics of traditional over-collateralized loans with these new credit-score-based uncollateralized options. The table below outlines the key structural differences.

| Feature | Traditional DeFi Loan | Credit-Score Loan |

|---|---|---|

| Collateral Requirement | 150-300% over-collateralization | Minimal or zero collateral |

| Risk Assessment | Asset price volatility | On-chain transaction history |

| Borrowing Cost | Higher due to capital inefficiency | Lower for high-reputation users |

| Capital Efficiency | Low | High |

| Eligibility Basis | Asset possession | Behavioral reputation |

The emergence of these products requires rigorous regulatory scrutiny. While the technology offers significant efficiency gains, the legal framework for enforcing unsecured debt on-chain remains underdeveloped. Lenders must rely on smart contract logic and reputation systems rather than traditional legal recourse, creating a new paradigm for financial inclusion that balances innovation with risk management.

What borrowers should know

Borrowers must distinguish between traditional credit checks and decentralized credit scoring. The latter evaluates on-chain financial activity and behavior based on their digital footprint rather than relying on centralized bureaus. This structural shift means your wallet history, not your bank statement, determines your lending eligibility.

To build a strong crypto credit score, prioritize consistent on-chain behavior. Repay loans on time, maintain healthy collateral ratios, and avoid frequent maxing of borrowing limits. Lenders use this data to assess risk, so demonstrating reliability through transparent transaction history is the most effective way to lower borrowing costs.

Privacy risks are inherent in data aggregation. Since scoring models require access to wallet addresses and transaction logs, borrowers must understand which protocols collect this data. Review the terms of any credit scoring service to ensure you are comfortable with the extent of your financial data being exposed to lending algorithms.

Borrowers should also verify the reputation of the scoring protocol. Not all on-chain scores are treated equally by lending platforms. Using a score from a widely recognized oracle or protocol ensures your reputation carries weight across multiple DeFi applications, reducing friction during the loan approval process.

No comments yet. Be the first to share your thoughts!