What defines a crypto credit score in 2026

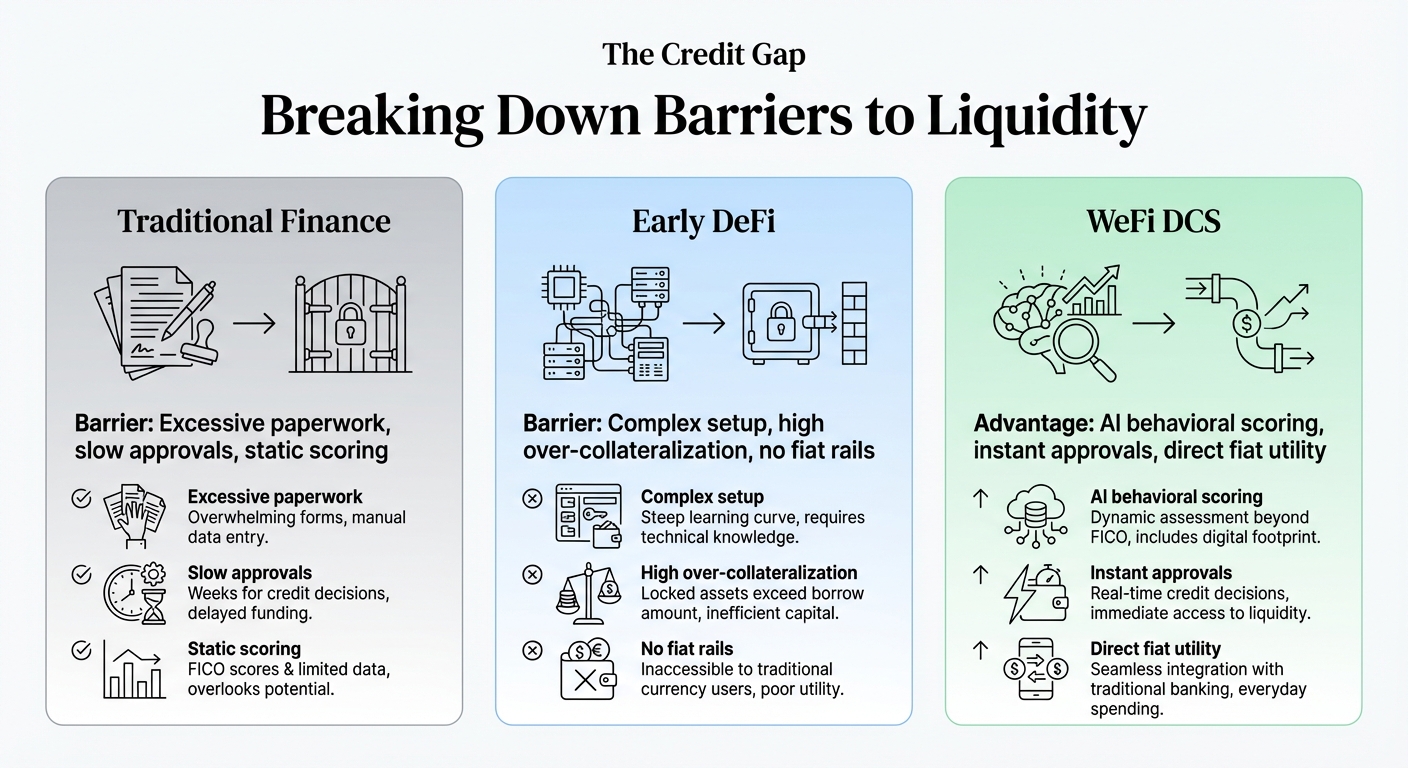

A crypto credit score in 2026 is a reputation metric derived from on-chain activity rather than personal identity. Unlike traditional FICO scores, which rely on credit history tied to a Social Security number or government ID, DeFi credit scores evaluate the financial behavior of a public wallet address. This shift moves credit assessment from an identity-based model to an activity-based one, where your transaction history, collateralization ratios, and repayment consistency serve as the primary evidence of trustworthiness.

In the decentralized finance (DeFi) ecosystem, lenders cannot easily verify who you are, but they can verify what you do. A wallet that consistently repays loans, maintains healthy collateral buffers, and engages with reputable protocols builds a strong on-chain reputation. This reputation becomes the "credit score," allowing the wallet to access better loan terms, higher borrowing limits, or lower interest rates without revealing personal identity. The FICO Crypto Credit Score initiative, for example, aims to bridge this gap by evaluating credit risk and repayment ability directly within the DeFi context, though it remains one of many evolving models rather than a universal standard.

The core difference lies in the data source. Traditional credit bureaus pull data from banks and credit card companies, creating a lagged and often opaque view of financial health. On-chain credit scores are transparent and real-time. Every transaction is recorded on the blockchain, creating an immutable ledger of financial behavior. This transparency allows for more nuanced risk assessment, where a user’s ability to manage complex DeFi positions can be a stronger indicator of creditworthiness than a simple history of on-time mortgage payments.

This model also changes who gets access to credit. In traditional finance, credit scores can exclude individuals with thin files or no credit history. In DeFi, a new wallet with no prior history starts with a neutral baseline, not a penalty. As soon as the wallet begins interacting with lending protocols—whether by providing liquidity or taking out small, repaid loans—it starts building a score. This merit-based approach rewards financial discipline and active participation in the ecosystem, regardless of geographic location or traditional banking status.

However, this system is not without limitations. On-chain activity only reflects behavior within the blockchain environment. It does not capture off-chain income, employment stability, or other financial obligations. A user might have an excellent on-chain credit score but significant hidden debt in the traditional banking system. As the industry matures, hybrid models that combine on-chain data with verified off-chain identity (via zero-knowledge proofs or decentralized identity standards) are likely to emerge, offering a more comprehensive view of creditworthiness.

CeFi versus DeFi credit models compared

Building a crypto credit score in 2026 generally follows one of two paths: centralized finance (CeFi) or decentralized finance (DeFi). The choice determines whether your creditworthiness is judged by traditional bureau algorithms or by on-chain transaction history. Each model offers distinct advantages for privacy, accessibility, and integration with the broader financial system.

The CeFi Route: Bureau Reporting

Centralized exchanges like Coinbase or Binance act as intermediaries. They collect your identity information (KYC) and transaction data, then report this activity to major credit bureaus such as TransUnion. This approach allows your crypto activity to directly influence your traditional FICO score. It is the most straightforward path for users who want their digital asset holdings to help them secure traditional loans, mortgages, or credit cards.

However, this model requires surrendering significant personal data. You are trusting a single corporate entity to handle your financial history. If the exchange fails or faces regulatory scrutiny, your credit reporting relationship may be disrupted. The trade-off is convenience and traditional credit impact for reduced privacy.

The DeFi Route: On-Chain History

DeFi protocols build credit scores using smart contracts and on-chain data. Services like Tally or Goldfinch analyze your wallet history, collateralization ratios, and repayment behavior across various protocols. This method is permissionless and privacy-preserving; you do not need to provide a Social Security number or government ID to start building a score.

The primary limitation is that DeFi scores currently have little to no direct impact on traditional credit bureaus. Your on-chain reputation is powerful within the crypto ecosystem, allowing you to access undercollateralized loans on specific platforms, but it does not yet help you qualify for a bank loan. This model favors those who prioritize privacy and are fully immersed in the decentralized economy.

Side-by-Side Comparison

The table below outlines the core differences between these two approaches to establishing a crypto credit score.

| Feature | CeFi (Centralized) | DeFi (Decentralized) |

|---|---|---|

| Data Source | Exchange KYC & transaction logs | On-chain wallet history |

| Privacy Level | Low (shares data with bureaus) | High (pseudonymous) |

| Traditional Credit Impact | Direct (reports to TransUnion/Experian) | Indirect or None |

| Accessibility | Requires ID verification | Open to anyone with a wallet |

| Primary Use Case | Securing traditional loans/credit | Accessing DeFi lending protocols |

Market Context

The value of the assets used to build these scores fluctuates with the broader market. Understanding current crypto market conditions is essential when leveraging assets for credit. The following chart tracks the performance of Bitcoin, the most common collateral used in both CeFi and DeFi lending models.

Which Path Fits Your Goals?

If your goal is to improve your ability to buy a home or get a traditional car loan, the CeFi route is currently the only viable option. By reporting your stable crypto activity to bureaus, you can demonstrate financial responsibility to traditional lenders. However, if you are a privacy advocate or operate primarily within the decentralized ecosystem, DeFi credit scores offer a robust alternative for accessing capital without exposing your identity.

As regulatory frameworks evolve, the line between these two models may blur. Initiatives like TransUnion’s partnership with blockchain protocols suggest a future where on-chain data might eventually feed into traditional credit reports, combining the best of both worlds.

Integrating on-chain history with traditional ratings

The bridge between decentralized finance and traditional credit reporting is no longer theoretical. In 2026, the integration of on-chain activity with established credit bureaus has moved from experimental pilots to operational infrastructure. This convergence allows lenders to assess risk using a dual-lens approach: the anonymity and velocity of blockchain transactions paired with the regulatory stability of legacy credit systems.

The most significant development in this space is the partnership between major credit reporting agencies and blockchain data providers. TransUnion, for example, has begun delivering credit scores for crypto lending by analyzing on-chain behavior without exposing sensitive personal data. This mechanism allows users to build a credit profile based on their repayment history on decentralized protocols, which is then translated into a format recognizable by traditional financial institutions. This process effectively turns wallet history into a verifiable financial identity.

For borrowers, this integration means that responsible activity in DeFi—such as consistently repaying flash loans or maintaining healthy collateral ratios—can contribute to a higher traditional credit score. Conversely, defaulting on a smart contract loan can now have tangible consequences in the off-chain world, creating a more robust accountability framework. This linkage is particularly valuable for the unbanked or those with thin credit files, as it provides an alternative pathway to establish financial trustworthiness.

However, the technical challenge lies in standardizing this data. Blockchain transactions are pseudonymous and highly complex, requiring sophisticated algorithms to map wallet addresses to real-world identities in compliance with privacy laws. The solution involves zero-knowledge proofs and secure data enclaves that verify creditworthiness without revealing the underlying transaction details. As these technologies mature, the distinction between "crypto credit" and "traditional credit" will likely vanish, replaced by a unified view of global financial behavior.

Regulatory frameworks reshape the crypto credit score 2026 landscape

The intersection of traditional credit scoring and decentralized finance is being defined by stricter regulatory oversight. In 2026, the primary focus for regulators has shifted toward stablecoin frameworks and standardized risk assessment protocols. This shift aims to integrate crypto activity into mainstream financial systems while mitigating systemic risks.

Stablecoin issuance models are now subject to rigorous reserve and redemption requirements. Supervisory frameworks, as highlighted in the PwC Global Crypto Regulation Report 2026, emphasize transparency in over 50 jurisdictions. This regulatory clarity allows lenders to treat stablecoin holdings as viable collateral, a significant departure from the volatility-driven skepticism of previous years.

Simultaneously, risk assessment standards are evolving to address illicit activity. The TRM Labs 2026 Crypto Crime Report indicates that illicit wallets received an estimated $158 billion in incoming value in 2025, a sharp increase from $64.5 billion in 2024. This surge underscores the necessity for robust credit scoring mechanisms that can distinguish between legitimate DeFi activity and high-risk transactions.

Traditional credit bureaus are also adapting. The FICO Score Credit Insights Spring 2026 Edition notes that lenders are increasingly incorporating alternative data sources to assess borrower reliability. This hybrid approach enables a more nuanced crypto credit score 2026 model, one that balances innovation with the compliance demands of modern financial regulation.

Choosing the right path for credit building

Your approach to a crypto credit score depends on whether you prioritize traditional financial integration or on-chain privacy. The landscape splits into two distinct methods: CeFi reporting, which feeds data to bureaus like FICO, and DeFi on-chain history, which relies on blockchain activity.

CeFi reporting suits users who need immediate access to traditional loans. Platforms like Centicio integrate with FICO to translate your crypto activity into a recognizable score. This path removes the friction of lengthy approvals but requires sharing your identity and financial data with centralized entities. It is the pragmatic choice for bridging Web2 and Web3.

DeFi on-chain history is better for privacy-focused builders. As noted in recent analysis, crypto-backed loans are collateral-based rather than credit-based, meaning your on-chain repayment history builds reputation without exposing your identity. This method ignores traditional credit scores entirely, focusing instead on your ability to pay through smart contract verification.

If your goal is to secure a mortgage or car loan, CeFi reporting provides the necessary documentation. If you are building a decentralized identity or prefer self-custody, focus on establishing a robust on-chain history. The right path is determined by your end goal, not just your asset holdings.

Frequently asked questions about crypto credit

What is the 2026 crypto report?

The 2026 crypto report typically refers to the PwC Global Crypto Regulation Report 2026. This document maps the shifting regulatory landscape for digital assets, with a specific focus on stablecoin issuance models, reserve requirements, and supervisory frameworks across more than 50 jurisdictions. It serves as a primary reference for understanding how traditional compliance standards are being applied to decentralized finance.

How is a crypto credit score calculated?

Unlike traditional FICO scores that rely on loan repayment history, a crypto credit score analyzes on-chain behavior. Lenders look at wallet age, transaction frequency, and asset diversity to assess reliability. While the FICO Score Credit Insights Spring 2026 Edition highlights traditional benchmarks, crypto scoring algorithms prioritize real-time liquidity and historical chain activity over past debt obligations.

Can crypto activity improve my traditional credit rating?

Not directly. Most traditional credit bureaus do not yet ingest on-chain data for standard credit reports. However, as DeFi protocols begin integrating with traditional banking rails, this may change. Currently, a strong crypto credit score helps you access decentralized lending platforms but does not automatically boost your score with Equifax or TransUnion.

No comments yet. Be the first to share your thoughts!