What the 2026 crypto credit score actually is

The term "crypto credit score" in 2026 does not refer to a single, standardized metric issued by the SEC or a central authority. Instead, it describes a hybrid evaluation method that combines traditional off-chain financial data with on-chain transaction history. This distinction is critical for borrowers and lenders navigating the evolving regulatory landscape, as it clarifies that no universal "crypto FICO" exists yet.

Traditional credit scores, such as the FICO model, rely heavily on debt repayment history and credit utilization from banks and credit card issuers. In contrast, the crypto credit score attempts to assess risk based on wallet activity, collateralization ratios, and interaction with decentralized finance (DeFi) protocols. Because blockchain transactions are immutable and public, these scores can theoretically offer a more transparent view of a borrower's financial behavior, provided the data is accurate and not manipulated.

Major credit bureaus have begun integrating crypto data into their models. For instance, TransUnion has started delivering credit scores for crypto lending, bridging the gap between traditional creditworthiness and blockchain activity. This allows individuals without extensive traditional credit histories to demonstrate reliability through their on-chain behavior, such as consistently repaying crypto-backed loans or maintaining healthy collateral ratios.

However, the lack of a unified standard means that a "high" crypto credit score on one platform may not translate to better terms on another. Lenders often develop their own proprietary algorithms to interpret on-chain data, leading to a fragmented ecosystem. Borrowers must understand which data points are being evaluated—whether it is solely transaction volume, repayment history on decentralized exchanges, or a combination of off-chain and on-chain factors—to effectively manage their digital reputation.

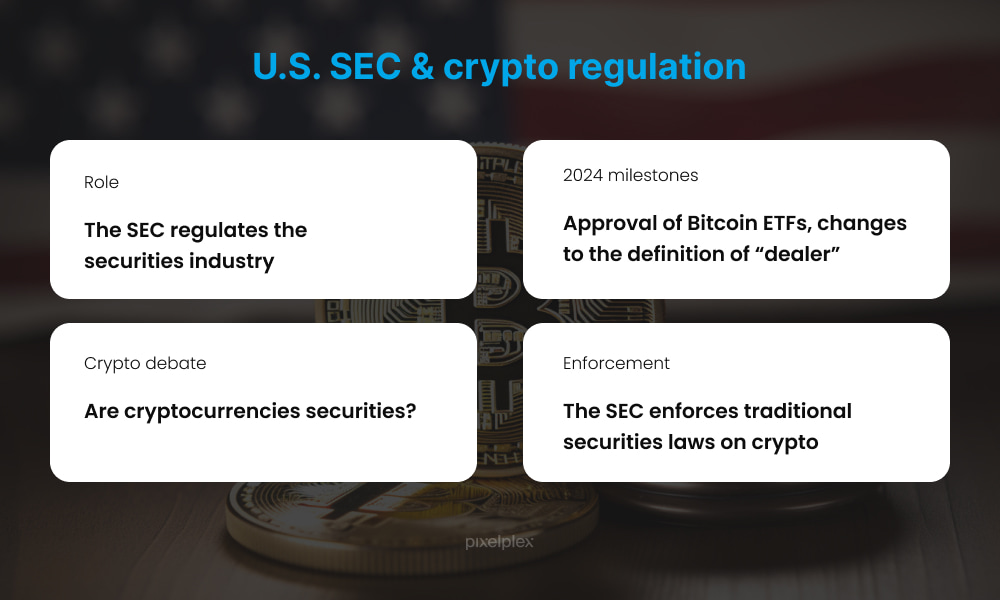

SEC compliance and DeFi lending protocols

The Securities and Exchange Commission’s 2026 regulatory framework fundamentally alters the operational landscape for decentralized finance (DeFi) lending platforms. Historically, DeFi protocols operated in a regulatory gray area, but the new rules explicitly bring on-chain lending under the purview of federal securities laws. This shift forces platforms to integrate traditional financial compliance mechanisms into their smart contract architectures, effectively blurring the line between anonymous code and regulated financial institutions.

At the core of this change is the mandatory implementation of Know Your Customer (KYC) and Anti-Money Laundering (AML) checks. Protocols that previously allowed pseudonymous participation must now verify user identities before granting access to lending pools. This requirement is not merely advisory; it is a condition for legal operation. Failure to implement robust identity verification systems results in immediate exposure to enforcement actions, including heavy fines and operational shutdowns. The integration of these checks often occurs at the wallet level or through integrated identity oracles, adding a layer of friction that challenges the core DeFi ethos of permissionless access.

Equally significant is the new mandate for credit data reporting. Lending platforms are now required to report borrower behavior and loan performance to traditional credit bureaus. This transparency aims to build a verifiable on-chain credit history, allowing users to leverage their repayment records for better terms in the future. However, it also means that defaulting on a DeFi loan can have tangible consequences for a user’s traditional financial standing. This convergence of on-chain activity and off-chain credit scores creates a unified financial identity, increasing accountability but also raising privacy concerns.

The impact of these regulations is visible in the broader market sentiment. Institutional adoption is accelerating as regulatory clarity reduces legal risk, while retail participation faces new hurdles. As noted in industry outlooks, the dawn of the institutional era is driven by these very compliance structures, which provide the legal certainty required for large-scale capital deployment. The market is adapting, with protocols that prioritize compliance gaining trust and market share.

On-chain reputation vs. traditional credit scores

The shift toward on-chain lending requires a fundamental re-evaluation of how creditworthiness is measured. Traditional credit scoring relies on off-chain financial data, whereas on-chain credit history derives from transparent blockchain activity. This distinction creates two distinct models for assessing risk in digital asset markets.

Traditional credit scores, such as those from FICO, are built on off-chain financial history. They analyze payment behavior, debt utilization, and credit age to generate a standardized numerical rating. These scores are private, centralized, and often require explicit consent to access. In contrast, on-chain reputation is built directly on the blockchain. It aggregates wallet transaction history, collateralization ratios, and protocol interactions. This data is public, immutable, and accessible to any smart contract without third-party intermediaries.

The trade-offs between these systems are significant. Traditional scores offer familiarity and regulatory alignment but lack granularity for crypto-specific assets. On-chain metrics provide real-time, granular data but can be manipulated through wash trading or lack historical depth for new users. The industry is currently seeing hybrid approaches, such as TransUnion integrating off-chain credit data into on-chain lending protocols to bridge this gap [src-serp-2].

| Metric | Traditional Credit Score | On-Chain Reputation |

|---|---|---|

| Data Source | Off-chain bank records, loans, and payments | Public blockchain transactions and wallet history |

| Privacy | Private; requires explicit consent to access | Public; visible to all network participants |

| Accessibility | Limited to centralized credit bureaus | Open; accessible via any blockchain explorer |

| Update Frequency | Monthly or quarterly updates | Real-time with every transaction |

| Regulatory Status | Highly regulated and standardized | Emerging; lacks universal standards |

How to build your crypto credit score in 2026

Establishing a verifiable crypto credit score in 2026 requires shifting from anonymous, collateral-only transactions to a documented history of on-chain activity. Because the SEC’s evolving framework emphasizes transparency and compliance, lenders now rely on aggregated data from regulated entities rather than raw wallet balances. Building this score involves a deliberate sequence of actions designed to prove financial reliability through compliant channels.

The first step is to link your primary wallet to a recognized credit reporting agency that supports digital assets. Unlike traditional banking, crypto credit scores require a middleware layer to translate on-chain transactions into a standardized format. Use platforms that are registered with the SEC or operate under clear regulatory guidelines to ensure your data is legally recognized by lenders.

Lenders analyze patterns over time, not just isolated events. Avoid sudden, high-volume transfers that might trigger anti-money laundering (AML) flags. Instead, maintain a steady rhythm of deposits, repayments, and small, regular transactions. This consistency demonstrates stability and helps build a robust historical record that credit algorithms can trust.

Borrowing through unregulated DeFi pools may not contribute to your formal credit score. Focus on lending platforms that are fully compliant with 2026 SEC regulations and report data to major credit bureaus. These institutions are more likely to recognize your repayment behavior, turning your crypto assets into a verifiable credit asset rather than just a collateral lock.

If your wallet has been associated with mixers or high-risk addresses, your score will suffer. Proactively clean your portfolio by moving funds from unverified sources to compliant exchanges or wallets. Disputing incorrect flags with your credit aggregator is essential; provide transaction hashes and proof of legitimate origin to clear your record.

Regularly check your crypto credit report for accuracy. Many compliant platforms now offer real-time score updates. Treat this metric like a traditional FICO score: small improvements in repayment speed and debt-to-income ratios can significantly raise your standing, unlocking better loan terms and lower interest rates in the regulated crypto market.

Building a crypto credit score is not instantaneous. It requires patience and a commitment to operating within the legal boundaries established by the SEC. By following these steps, you transform your digital assets from opaque holdings into a transparent, trusted financial identity.

No comments yet. Be the first to share your thoughts!