Why on-chain identity matters in 2026

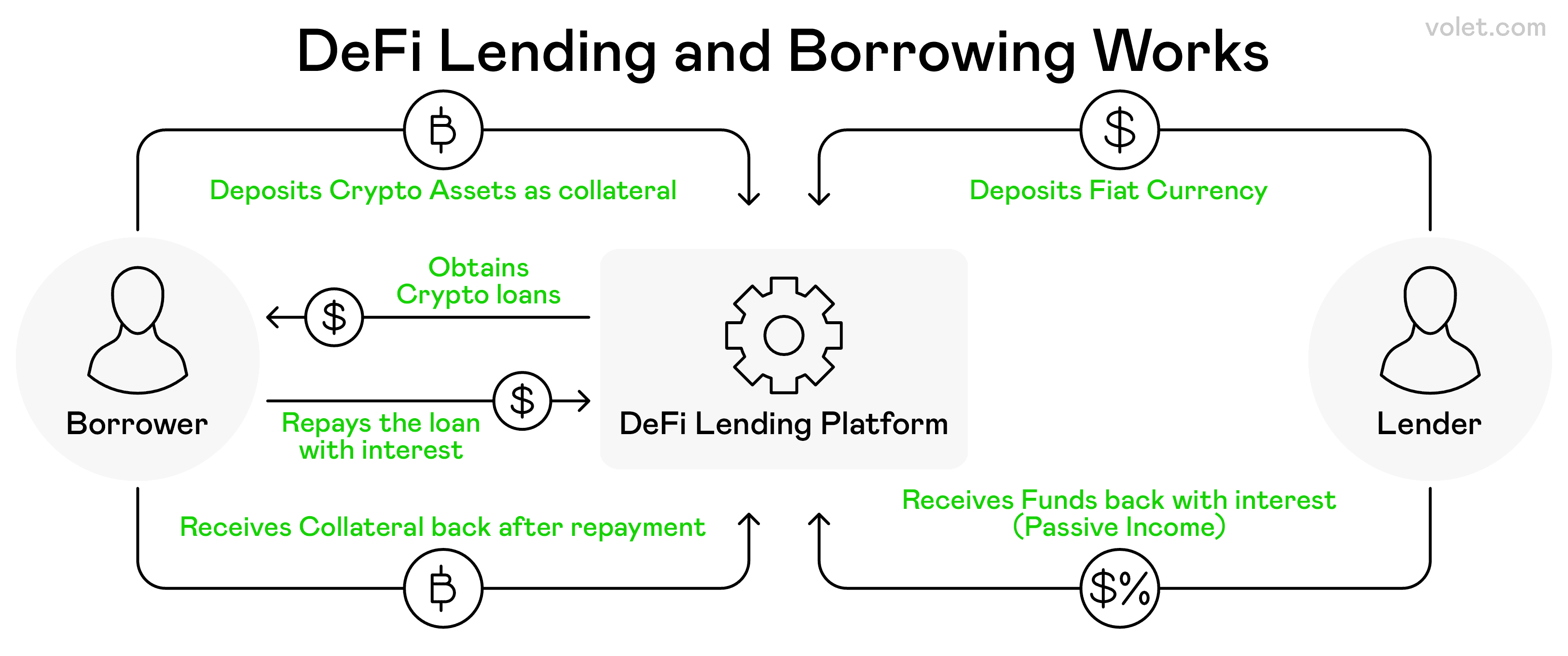

The DeFi lending landscape has shifted from anonymous, over-collateralized vaults to identity-based credit lines. In 2025, outstanding DeFi loans grew by 37%, a surge primarily driven by real-world asset (RWA) tokenization and institutional demand for yield. This growth signals a structural change: lenders now trust historical on-chain behavior more than locked-up collateral.

This transition relies on on-chain identity protocols that aggregate transaction history, repayment records, and interaction patterns into a verifiable credit profile. Instead of requiring users to lock 150% of their loan value in volatile assets, lenders can now offer unsecured or under-collateralized lines based on reputation. This model mirrors traditional banking but operates entirely on public ledgers, where every transaction is immutable and auditable.

The result is a more efficient capital allocation system. Institutional investors, who previously avoided DeFi due to opacity and risk, can now participate with greater confidence. On-chain identity reduces information asymmetry, allowing lenders to price risk accurately without demanding excessive collateral. This shift not only expands access to credit for individual users but also deepens liquidity for institutional players seeking yield in a maturing market.

How on-chain credit history is calculated

DeFi credit scoring moves away from centralized bureaus like Equifax or TransUnion. Instead, it builds a financial identity directly from your wallet’s public ledger. This approach relies on probabilistic measures of repayment behavior, debt-to-income ratios, and wallet activity rather than traditional bureau data.

The technical mechanism behind this shift is best exemplified by frameworks like the On-Chain Credit Risk Score (OCCR Score). As detailed in research from arXiv, the OCCR Score quantifies credit risk by analyzing historical transaction patterns. It treats every repayment, loan closure, and liquidity provision as a data point in a larger probability model. This allows protocols to estimate the likelihood of future default without needing a Social Security Number or a bank statement.

To calculate these scores, algorithms look at several key metrics. First, they assess repayment consistency. Did you pay back a flash loan or a fixed-term credit position on time? Second, they evaluate debt-to-income ratios. In DeFi, "income" often translates to consistent cash flow from staking rewards or yield farming, while "debt" is the total value locked in leveraged positions relative to your total portfolio. Finally, wallet activity depth matters. A wallet that interacts with multiple reputable protocols over a long period is viewed as less risky than one that appears only when seeking high-yield, high-risk opportunities.

This data is then processed into a standardized range, typically 300 to 850, mirroring traditional FICO scores. Platforms like DeFi Scoring provide per-protocol risk heatmaps, allowing users to see exactly how their on-chain history is interpreted by different lending markets. This transparency lets borrowers understand why they might be offered a lower loan-to-value (LTV) ratio on one platform versus another.

The volatility of crypto assets adds a layer of complexity to these calculations. Unlike a salaried income in fiat, crypto holdings can swing 10% or more in a single day. Therefore, on-chain scoring models must account for this instability. They often apply dynamic risk adjustments based on the current market environment, as seen in the BTC/USD chart above. A score that looks strong in a bull market might be downgraded in a bear market if the underlying collateral becomes too volatile.

By using these probabilistic models, DeFi protocols can offer undercollateralized loans to users with strong on-chain histories. This replaces the need for over-collateralization, which locks up capital and reduces capital efficiency. The result is a credit system that is accessible to anyone with a wallet, verifiable by anyone, and built on actual financial behavior rather than opaque institutional data.

Top DeFi credit score platforms compared

Use this section to make the DeFi Credit Scoring decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Impact on borrowing costs and LTV

Use this section to make the DeFi Credit Scoring decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Risks and regulatory outlook for 2026

DeFi credit scoring relies on on-chain history to replace traditional collateral, but the system faces significant headwinds. Moody’s Investors Service warns that while default rates are projected to decline in 2026, the margin for error is thin. A relatively small economic shock could reverse this trend, causing defaults to spike across protocols that lack the safety buffers of traditional banking.

The regulatory environment remains equally precarious. As the FDIC and other financial watchdogs scrutinize decentralized finance, protocols must navigate a complex web of compliance requirements. The gap between rapid innovation and regulatory oversight creates uncertainty for both lenders and borrowers. Firms are currently preparing for this shift by prioritizing data-driven decisions, yet the data infrastructure behind private credit and low-default portfolios often lags behind the speed of growth.

Data privacy stands as another critical risk. On-chain identity is permanent and public, meaning that a borrower’s financial history cannot be erased. This transparency raises concerns about how sensitive financial data is aggregated and used. Borrowers must ensure that the protocols they interact with prioritize secure data handling, as a breach or misuse of on-chain history could have long-lasting reputational and financial consequences.

Improving your on-chain credit profile

Building a strong DeFi credit score requires treating your wallet like a traditional bank account. Lenders look for evidence of reliability, so your primary goal is to demonstrate consistent repayment behavior and responsible liquidity management.

Set up automated transfers or calendar reminders for every loan maturity. A single missed payment on a DeFi lending protocol can permanently lower your score, as on-chain history is immutable and visible to all future lenders.

Avoid maxing out your credit lines. Keeping your borrowed amount below 30% of your available limit signals financial stability. High utilization suggests you are overextended, which increases your perceived risk profile.

Lenders prefer users with varied transaction histories. Regularly use different protocols for lending, borrowing, and staking. This breadth of activity provides more data points for credit scoring algorithms to verify your financial habits.

Use real-time alert tools to track your collateral health. Sudden market drops can trigger liquidations before you can react. Proactively adding collateral or repaying partial debt during volatility protects your score from severe penalties.

Your on-chain identity is your most valuable financial asset in 2026. By consistently demonstrating responsible borrowing habits, you unlock access to lower interest rates and higher credit limits across the decentralized lending landscape.

Frequently asked questions on DeFi credit

How do I improve my on-chain credit score?

Unlike traditional credit, your DeFi score is built from verifiable on-chain history. The most effective way to improve it is by maintaining a clean repayment record across decentralized lending protocols. Avoid maxing out your borrowing limits; keeping your utilization low signals reliability to credit oracles. Consistent, on-time repayments of stablecoin loans or liquidity positions are the primary drivers of a higher score.

How is DeFi credit scoring different from traditional FICO?

Traditional credit relies on centralized banking data and personal identifiers, often excluding those with thin credit files. DeFi scoring uses public blockchain data to assess financial behavior without revealing your identity. It focuses on actual asset movement and repayment history rather than income verification. This allows anyone with an active wallet to build a portable reputation that travels across different protocols.

Is DeFi credit scoring reliable for large loans?

Yes, but it depends on the protocol. Major DeFi lending platforms now integrate sophisticated credit scoring models that analyze multi-chain history to determine loan-to-value ratios. While smaller protocols may still rely heavily on over-collateralization, leading platforms use these scores to offer under-collateralized loans. The reliability increases as more data points are aggregated across the ecosystem.

Can I use my DeFi score across different platforms?

Reputation is becoming portable. Some decentralized identity protocols allow your credit history to be verified by multiple lenders without re-submitting documents. However, adoption is not yet universal. It is best to check if a specific lending platform integrates with the credit scoring oracle you used to build your history.

No comments yet. Be the first to share your thoughts!