How DeFi Lending Shapes Your Score

The shift from traditional credit checks to on-chain reputation systems is no longer theoretical. In 2026, DeFi activity has become a primary factor in credit assessments, replacing the opaque black box of FICO scores with transparent, verifiable ledger data. This transition removes traditional barriers such as lengthy approval processes and rigid income verification, allowing borrowing power to be determined by actual asset behavior rather than historical paperwork [src-serp-2].

Institutional lenders now measure counterparty risk using real-time on-chain metrics. These systems analyze wallet balances, transaction flows, reserve composition, and specific transaction behaviors to build a dynamic risk profile [src-serp-1]. Unlike a static credit report that updates monthly, this on-chain reputation updates with every interaction, providing lenders with a granular view of your financial discipline.

For borrowers, this means your creditworthiness is directly tied to your DeFi footprint. Consistent repayment of loans, healthy collateralization ratios, and active participation in reputable protocols contribute positively to your on-chain score. Conversely, defaulting on a smart contract or maintaining a dangerously high loan-to-value ratio immediately impacts your ability to access future capital.

This new paradigm rewards transparency. Your DeFi history serves as a digital resume, proving your reliability to lenders who previously lacked the data to assess crypto-native individuals. As the market matures, this on-chain reputation will likely serve as the bridge between traditional finance and decentralized credit, making your DeFi lending habits the foundation of your financial identity.

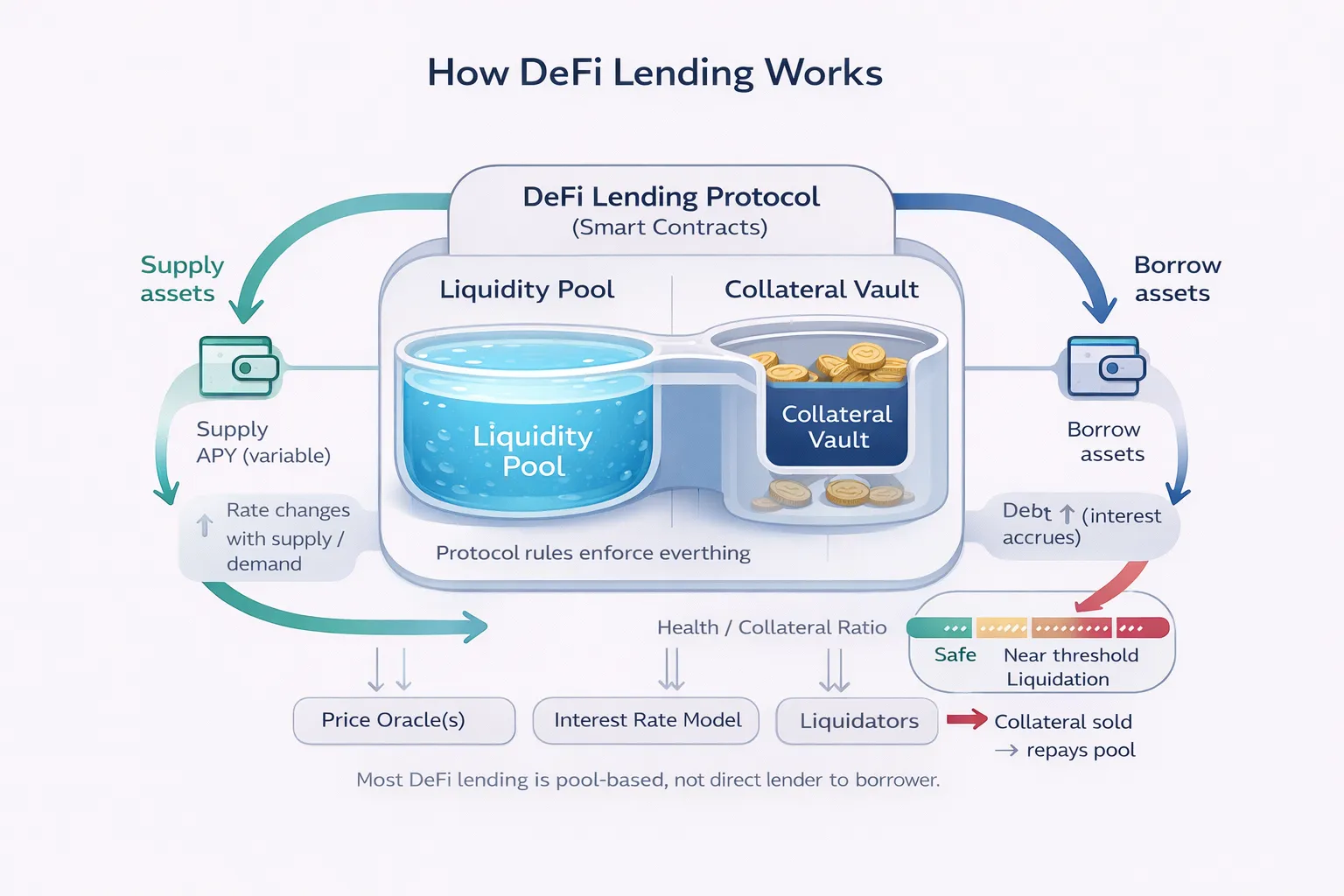

On-chain history and risk metrics

Traditional credit bureaus rely on payment history and debt-to-income ratios. DeFi lending platforms build a different profile entirely. They look at your wallet balance, transaction behavior, and how you manage leverage. These on-chain metrics create a transparent, auditable record of your financial discipline.

Unlike traditional credit, DeFi scores are often transparent and auditable on-chain.

The most critical metric is your Loan-to-Value (LTV) ratio. Lenders track how much you borrow relative to the collateral you provide. Consistently maintaining a low LTV signals that you can manage risk without relying on liquidations. It shows you understand the volatility of crypto assets.

Transaction history also plays a major role. Lenders analyze the frequency and type of your trades. Regular, stable activity suggests a serious investor. Sudden, high-frequency trading or interactions with known mixer protocols can raise red flags. Your wallet balance provides a baseline for your net worth, but it is your flow of funds that tells the real story.

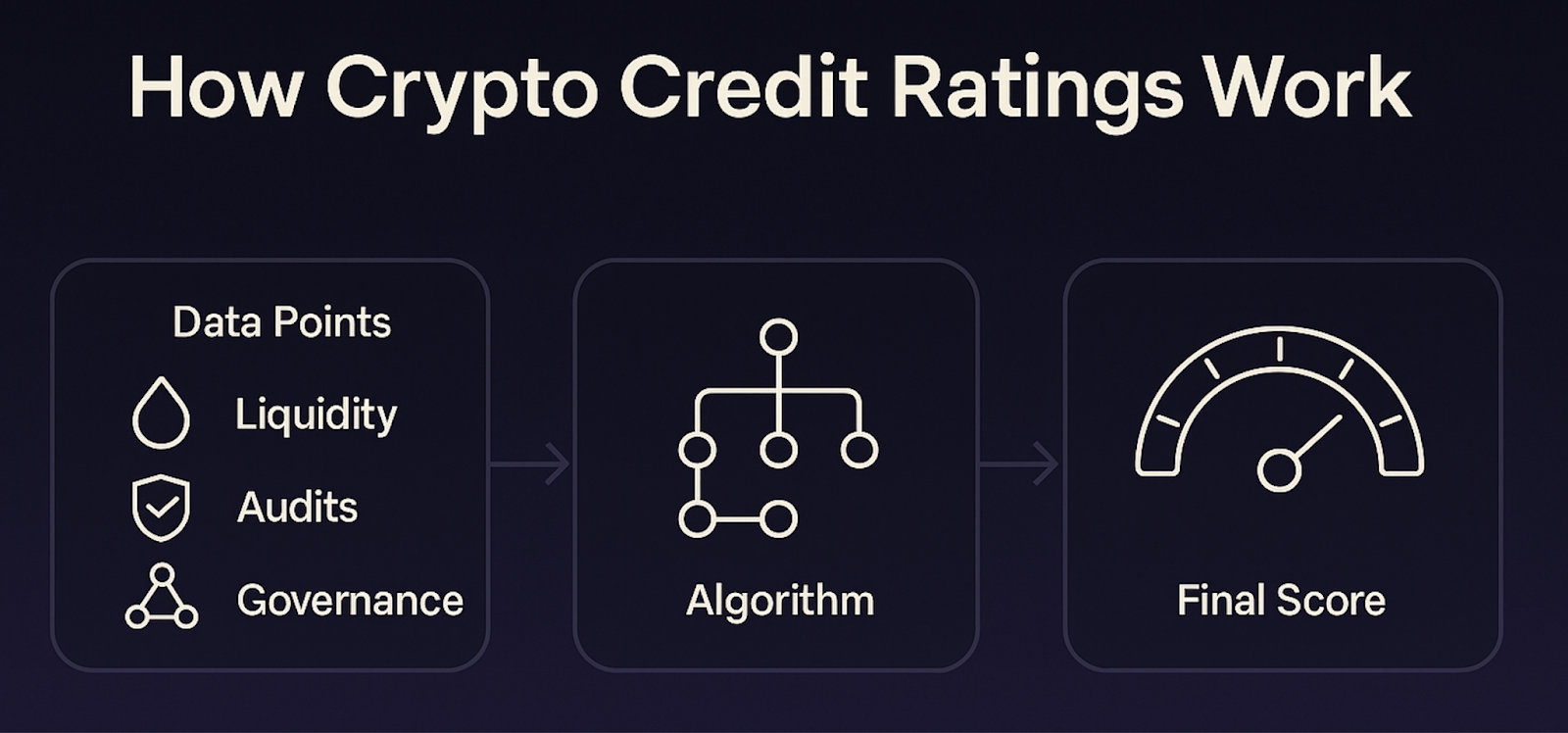

Agio Ratings and other on-chain analytics firms combine these data points into a single score. They look at wallet balances, reserve composition, and transaction behavior to measure counterparty risk. This approach allows lenders to assess you as a borrower, not just a holder of assets.

This shift from identity-based scoring to behavior-based scoring is changing the landscape. As noted by Nizan Geslevich Packin in the Cardozo Law Review, crypto-native credit scoring aims to bridge the gap in risk assessment. It renders DeFi lending more robust and inclusive by focusing on actual financial behavior rather than external credit history.

Institutional reporting standards

Traditional credit bureaus are no longer ignoring blockchain activity. TransUnion, a major credit reporting agency, has begun integrating crypto data into its reporting framework. This allows DeFi users to build recognized credit histories without exposing their on-chain identity to the entire financial system.

The process works by linking a user's off-chain identity to their on-chain lending behavior. When you apply for a loan on a blockchain protocol, TransUnion can provide a traditional credit score based on your repayment history. This bridges the gap between decentralized finance and traditional financial recognition, allowing your crypto activity to influence your eligibility for conventional loans.

This integration marks a significant shift in how creditworthiness is measured. It moves the industry away from purely off-chain data and towards a hybrid model that includes on-chain assets and liabilities. For borrowers, this means that responsible DeFi participation can now contribute to a broader, more inclusive credit profile.

| Credit Source | Data Type | Privacy Model | Recognition Scope |

|---|---|---|---|

| TransUnion | On-chain lending history | Identity-linked, score-only | Traditional banks & lenders |

| DeFi Protocols | Raw wallet transactions | Anonymous by default | Crypto-native platforms only |

| FICO | Traditional debt & payment history | Full personal data required | Broad US financial system |

Manage your DeFi credit profile

Your crypto credit score is a reflection of your on-chain behavior, not just your balance. Platforms like FICO Crypto Credit Score evaluate your ability to repay loans and manage risk, rewarding responsible borrowing with better rates and higher limits. To build a strong profile, you must treat your DeFi positions with the same discipline as traditional finance.

Building a strong DeFi credit profile takes time and consistency. By following these steps, you can improve your creditworthiness and access better financial opportunities in the crypto ecosystem.

Common Questions About Crypto Credit

The intersection of decentralized finance and traditional credit systems raises specific questions about data privacy, institutional adoption, and the future of credit scoring. Here are the most common concerns addressed by current market data and regulatory developments.

No comments yet. Be the first to share your thoughts!