How on-chain credit scoring works

Use this section to make the Crypto Credit Score decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

How DeFi Lending Shapes Your On-Chain Reputation

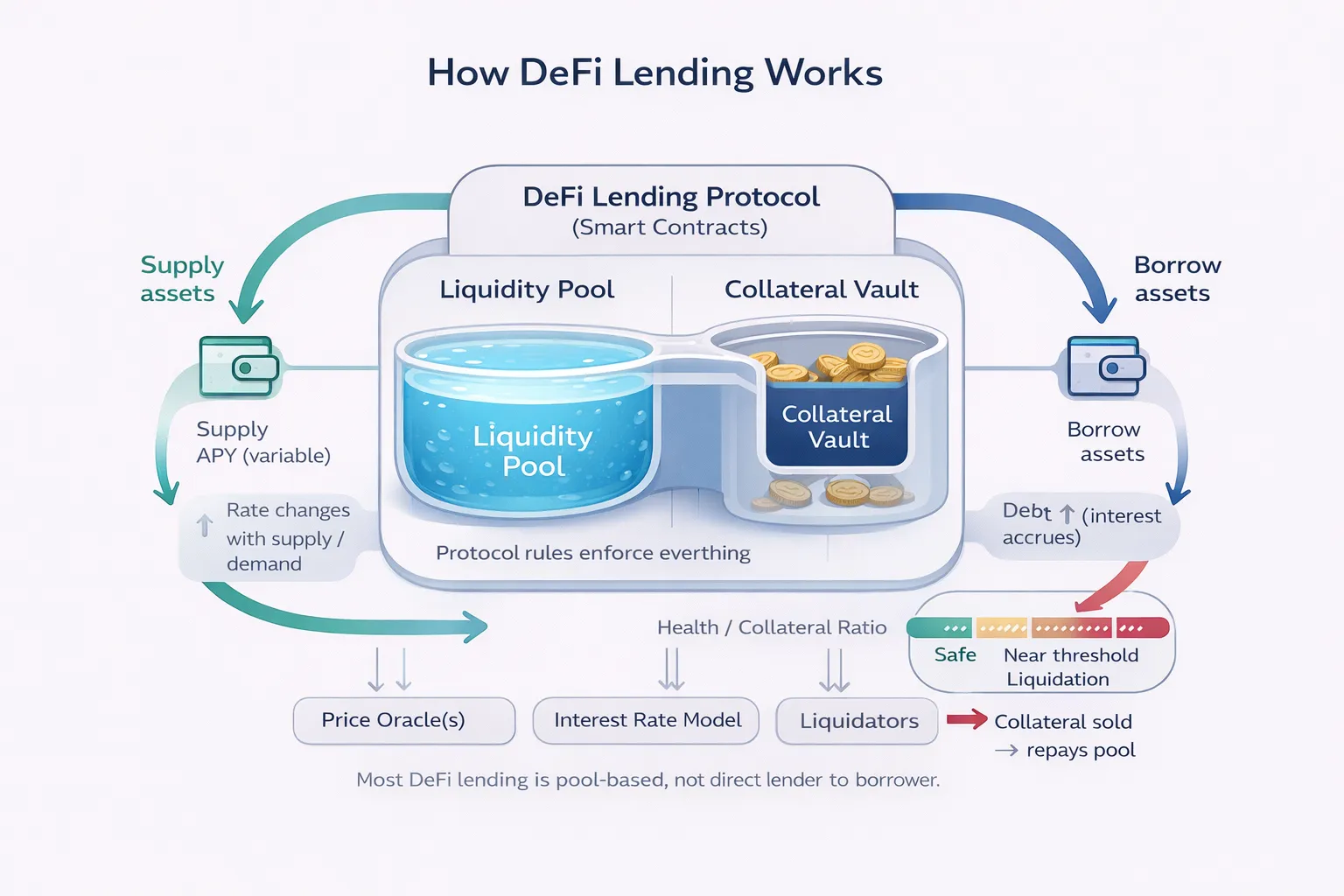

Unlike traditional banking, where a loan application triggers a hard inquiry that temporarily dents your FICO score, decentralized finance (DeFi) operates on an open ledger. Your borrowing and repayment history on protocols like Aave or Compound is not just a record of debt; it is a permanent, public signal of your financial reliability. This on-chain behavior forms the backbone of what institutions now call "crypto credit ratings." These ratings augment traditional counterparty analysis with granular data points, including wallet balances, reserve composition, and consistent transaction behavior [src-serp-1].

When you borrow against collateral, you are essentially proving your ability to manage leverage. Repaying a loan on time demonstrates liquidity management and respect for protocol constraints. Conversely, defaulting or triggering a liquidation event creates a public blemish that can persist indefinitely. Lenders and aggregators use this data to assign risk scores that determine future borrowing limits and interest rates. In this system, your wallet address acts as your corporate identity, and its creditworthiness is built through consistent, verifiable actions rather than opaque credit bureau reports [src-serp-2].

This shift from identity-based to behavior-based credit allows for a more dynamic risk assessment. A user with no traditional credit history but a strong record of repaying DeFi loans can access significant capital. However, this transparency cuts both ways. A single liquidation event can severely impact your ability to borrow at favorable rates across multiple protocols. Understanding that every transaction contributes to your on-chain reputation is critical for long-term financial health in DeFi.

To understand the collateral risks that drive these reputation metrics, consider the volatility of the primary asset used in these loans.

Comparing on-chain scoring models

DeFi lending protocols and third-party raters use different lenses to assess borrower risk. While some focus on immediate collateral health, others build a broader profile of on-chain behavior. Understanding these differences helps you choose the right credit score for your needs.

Key scoring models

Agio Ratings focuses heavily on institutional-grade data. It augments traditional inputs with on-chain metrics like wallet balances, reserve composition, and transaction behavior to measure counterparty risk [[src-serp-1]]. This approach is ideal for protocols requiring deep due diligence.

FICO Crypto Credit Score adapts its established financial scoring logic to the crypto space. It evaluates credit risk and the ability to pay crypto loans, bridging the gap between traditional finance expectations and DeFi realities [[src-serp-6]].

Metrics at a glance

The following table compares how these models evaluate key risk factors. Note that native DeFi protocols often rely on simpler, real-time collateralization ratios, whereas third-party raters incorporate historical data.

| Model | Primary Data Source | Risk Focus | Update Frequency |

|---|---|---|---|

| Agio Ratings | On-chain wallet flows & reserves | Counterparty & asset risk | Near real-time |

| FICO Crypto | Credit history & loan repayment | Ability to pay | Periodic |

| Native DeFi Protocols | Collateral value & health factor | Liquidation risk | Real-time |

Building a strong blockchain credit history

Your on-chain reputation is not a fixed number but a living record of how you handle digital assets. Unlike a traditional credit score determined by a bureau, your DeFi creditworthiness is built through transparent, verifiable interactions on the blockchain. In 2026, as institutional access expands, this data trail becomes the primary metric for lenders evaluating your reliability.

The foundation of a strong history is consistent collateral management. Most DeFi lending protocols require overcollateralization, meaning you must lock assets worth more than the loan you take out. Paying back these loans on time, or even early, signals financial discipline to the protocol. This behavior creates a positive feedback loop, often resulting in lower interest rates and higher borrowing limits in the future.

Diversifying your collateral can also strengthen your profile. Relying solely on volatile assets like meme coins may raise risk flags for lenders. Instead, holding a mix of stablecoins and blue-chip assets like Bitcoin or Ethereum demonstrates stability. As Grayscale notes, the industry is moving toward an institutional era where asset quality matters more than speculative hype.

Finally, avoid frequent liquidations. A liquidation event is a public record of your inability to meet margin calls, which can severely damage your on-chain reputation. By maintaining healthy collateralization ratios and monitoring market trends, you protect your credit history and keep your borrowing power intact.

Frequently asked questions about on-chain credit

Is 2026 a good year for crypto adoption?

With clearer regulation, expanding institutional access, and improving macro liquidity, 2026 may be the year the industry's groundwork begins to pay off. While 2025 saw crypto under-deliver on price, it over-delivered on fundamentals, setting the stage for 2026.

Can DeFi lending build a traditional credit score?

No. DeFi lending activity does not report to Equifax, Experian, or TransUnion. Your on-chain reputation is a separate metric used by lending protocols, not your FICO score.

How do protocols verify my on-chain reputation?

Protocols use on-chain analytics to assess your wallet history. They look at your loan repayment speed, collateralization ratios, and transaction consistency to assign a risk tier.

Is my on-chain data private?

No. All transactions are public on the blockchain. While your identity might be pseudonymous, your financial behavior is transparent to anyone who analyzes the address.

No comments yet. Be the first to share your thoughts!