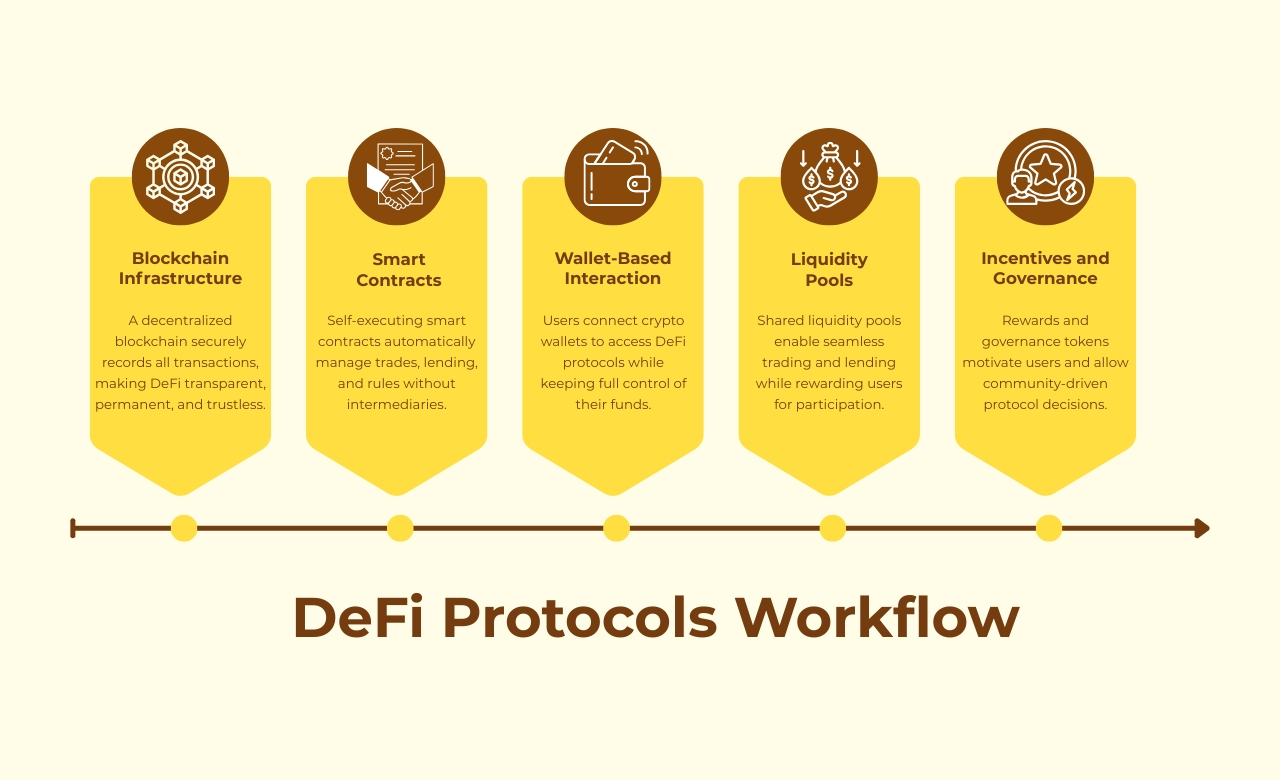

DeFi credit protocols in 2026

The landscape of decentralized lending has shifted from experimental code to institutional infrastructure. As of April 2026, DeFi lending protocols hold approximately $54 billion in deposits across more than 380 distinct platforms, according to DefiLlama data. This scale reflects a maturation of credit scoring mechanisms that now prioritize on-chain behavior over traditional identity verification.

Leading protocols such as Aave, Morpho, Spark, Compound, Fluid, and Euler dominate the sector by offering varying degrees of capital efficiency and risk management. These platforms have moved beyond simple over-collateralized loans to integrate sophisticated credit scoring models. These models analyze transaction history, collateral health, and repayment consistency to determine borrowing limits and interest rates without relying on centralized credit bureaus.

The transition to 2026 has also introduced greater interoperability between these protocols. Lenders can now access liquidity across multiple chains while maintaining a unified credit score. This integration reduces the fragmentation that previously hindered large-scale adoption. However, it also means that a default on one platform can impact borrowing power across the entire ecosystem.

For users navigating this space, understanding the specific risk parameters of each protocol is essential. While the total value locked provides a snapshot of trust, the underlying credit scoring algorithms vary significantly in their sensitivity to market volatility. Choosing the right protocol depends on whether you prioritize maximum liquidity or lower interest rates based on a strong on-chain credit history.

Defi credit protocols 2026 choices that change the plan

Choosing a DeFi credit protocol in 2026 requires balancing yield, risk, and flexibility. With $54 billion in deposits across 380+ protocols, the market has matured beyond simple lending pairs. You are no longer just borrowing against collateral; you are selecting a credit infrastructure layer that defines how your on-chain identity is valued.

The primary tradeoff is between centralized efficiency and decentralized transparency. Major protocols like Aave and Compound offer deep liquidity and institutional-grade audits, making them safer for large positions. However, this comes with higher barriers to entry and stricter collateral requirements. Newer entrants like Euler and Morpho focus on capital efficiency and permissionless risk markets, offering better rates but requiring users to conduct their own due diligence on smart contract risk.

To navigate this, compare protocols across four concrete factors: liquidity depth, interest rate models, collateral flexibility, and governance risk. Use the comparison below to evaluate which model aligns with your specific use case.

| Protocol | Primary Strength | Key Tradeoff | Best Use Case |

|---|---|---|---|

| Aave | Deep liquidity & institutional audits | Higher collateral requirements | Large, stable positions |

| Morpho | Capital efficiency & yield optimization | Higher smart contract complexity | Yield-seeking lenders |

| Compound | Proven stability & simplicity | Lower yields than competitors | Conservative borrowers |

| Euler | Permissionless risk markets | Fragmented liquidity pools | Niche asset trading |

Your decision should start with the asset you intend to borrow. If you need to borrow volatile assets like altcoins, prioritize protocols with deep liquidity in those specific pairs to avoid liquidation cascades. If you are lending stablecoins, focus on protocols with the highest risk-adjusted yields, such as Morpho’s peer-to-peer pools. Always verify the protocol’s current TVL and audit status before committing funds, as the DeFi landscape shifts rapidly.

How to choose the right DeFi credit protocol

The landscape for DeFi credit protocols has shifted from speculative experiments to institutional-grade infrastructure. With $54 billion in deposits across 380+ protocols as of April 2026, selecting the right platform requires moving beyond simple APY comparisons. You must evaluate how each protocol calculates creditworthiness, the liquidity depth of its pools, and the regulatory clarity of its jurisdiction.

Follow this decision framework to match your specific risk profile and lending goals with the appropriate protocol.

Your first step is to determine whether you prioritize capital preservation or yield maximization. Conservative lenders should look for protocols with deep liquidity and established track records, such as Aave or Compound, which have survived multiple market cycles. Aggressive lenders might explore newer entrants like Euler or Fluid, which often offer higher yields but carry greater smart contract and liquidity risks.

Not all protocols use the same method to assess borrower reliability. Some rely purely on over-collateralization, while others integrate off-chain data or on-chain history to offer under-collateralized loans. Check if the protocol uses a transparent scoring model or a black-box algorithm. Transparent models reduce the risk of unexpected liquidations and provide clearer paths to building a credit history.

High yields are meaningless if you cannot withdraw your funds when needed. Review the total value locked (TVL) and the average pool depth for your target asset. Protocols with fragmented liquidity may suffer from high slippage or temporary freezes during market stress. Look for protocols that aggregate liquidity across multiple layers, such as Morpho, to ensure consistent access to your capital.

As DeFi becomes more institutional, regulatory compliance is a key differentiator. Protocols operating with clear licenses or operating in jurisdictions with established crypto frameworks offer greater legal certainty. This is particularly important for large deposits or institutional capital. Verify if the protocol has undergone security audits and if it implements any KYC/AML requirements for certain features.

Finally, calculate the total cost of participation, including gas fees, protocol fees, and potential slippage. Use the comparison tools below to weigh these costs against the expected yield. Remember that higher yields often correlate with higher risk or lower liquidity. Choose the protocol that offers the best risk-adjusted return for your specific use case.

| Protocol | Credit Model | Risk Level | Best For |

|---|---|---|---|

| Aave | Over-collateralized | Low | Conservative lenders |

| Morpho | Peer-to-peer | Medium | Yield optimization |

| Euler | Unsecured credit | High | Established credit history |

| Fluid | Hybrid | Medium-High | High-yield seekers |

Watch out for weak credit scoring options

DeFi credit scoring is still experimental. Many protocols claim to offer "instant credit scores" or "on-chain reputation," but these metrics are often opaque, unverified, or derived from narrow data sets. In 2026, with over $54 billion in DeFi lending deposits across 380+ protocols, the landscape is fragmented and misleading claims are common.

Common pitfalls to avoid

Over-reliance on single-source data: Some protocols base creditworthiness solely on one chain or token, ignoring cross-chain activity. This creates a skewed risk profile.

Vague methodology: If a protocol doesn't clearly explain how it calculates scores, treat it with skepticism. Transparency is non-negotiable in credit assessment.

Ignoring off-chain context: On-chain data alone doesn't capture a borrower's full financial picture. Protocols that ignore traditional credit history or real-world assets may misjudge risk.

How to verify a protocol's credit model

- Check if the methodology is publicly documented.

- Look for third-party audits or peer-reviewed research.

- Compare scores across multiple protocols to spot inconsistencies.

- Assess whether the model accounts for your specific use case, such as borrowing against volatile assets or stablecoins.

Defi credit protocols 2026: frequently asked: what to check next

How do DeFi credit scores differ from traditional FICO scores?

Traditional credit scores rely on centralized data from banks and credit bureaus, often excluding those with thin financial files. DeFi credit protocols calculate scores on-chain, analyzing your lending history, collateral health, and repayment behavior across protocols like Aave or Compound. This creates a portable reputation that follows your wallet, allowing you to access better rates without revealing personal identity or relying on a single institution’s gatekeeping.

Are DeFi lending rates fixed or variable?

Most DeFi lending protocols use variable rates that adjust based on real-time supply and demand. When demand for a specific asset (like USDC or ETH) rises, borrowing costs increase automatically. Some newer protocols offer fixed-rate options for specific terms, but variable rates remain the standard. This means your loan payments can fluctuate, requiring you to monitor market conditions closely to avoid unexpected cost spikes during high-demand periods.

Is my collateral safe if I default on a DeFi loan?

If your collateral value drops below the required threshold, the protocol automatically liquidates it to cover the loan. You typically do not get a grace period or the chance to negotiate terms. This automated process protects lenders but puts borrowers at risk of losing assets quickly during volatile market swings. Understanding your liquidation threshold and maintaining a healthy collateralization ratio is essential to avoid forced sales.

Can DeFi credit scores impact my access to real-world services?

Currently, most DeFi credit scores are isolated within the blockchain ecosystem and do not directly affect traditional banking or credit reports. However, the landscape is shifting. Newer "hybrid" protocols are beginning to bridge on-chain reputation with off-chain identity, potentially allowing verified DeFi history to influence traditional lending decisions in the future. For now, your DeFi score is primarily useful for optimizing rates within decentralized finance.

No comments yet. Be the first to share your thoughts!