Crypto credit score 2026 limits to account for

Your crypto staking rewards no longer automatically build credit. The 2026 regulatory landscape, shaped by the PwC Global Crypto Regulation Report, has tightened how digital assets are treated by traditional credit bureaus. Staking income is now viewed as volatile capital, not stable cash flow, meaning it rarely qualifies for standard credit score calculations.

This shift forces a clearer distinction between on-chain reputation and traditional creditworthiness. While "crypto-native" scoring models aim to bridge this gap by analyzing DeFi lending history, these scores currently lack broad acceptance with major lenders. You cannot yet use a DeFi repayment history to secure a conventional mortgage or auto loan.

The practical impact is that your staking yields do not lower your debt-to-income ratio. Instead, they remain separate assets. To improve your credit score in 2026, you must report staking payouts as income on traditional forms, but expect lenders to discount their stability. The constraint is structural: credit scores measure reliability in fiat systems, and crypto assets are still considered high-risk counterparty exposure by most institutions.

Crypto credit score 2026 choices that change the plan

The 2026 regulatory landscape has shifted how creditworthiness is measured for digital asset holders. Traditional credit scoring models rarely capture on-chain behavior, creating a gap that crypto-native solutions and institutional rating agencies are now attempting to fill. Understanding the tradeoffs between these new metrics and traditional credit reports is essential for anyone using crypto as a financial tool.

Collateral vs. Credit-Based Lending

The most significant tradeoff in 2026 is the distinction between collateral-backed loans and credit-based borrowing. Crypto-backed loans, often secured by Bitcoin or Ethereum, remove traditional credit score barriers. This allows users to access liquidity without a credit check, but it introduces liquidation risk if the collateral value drops. In contrast, credit-based crypto lending relies on your traditional credit score and income verification, offering lower interest rates for those with strong credit but excluding those with thin or poor credit files.

On-Chain Data and Institutional Ratings

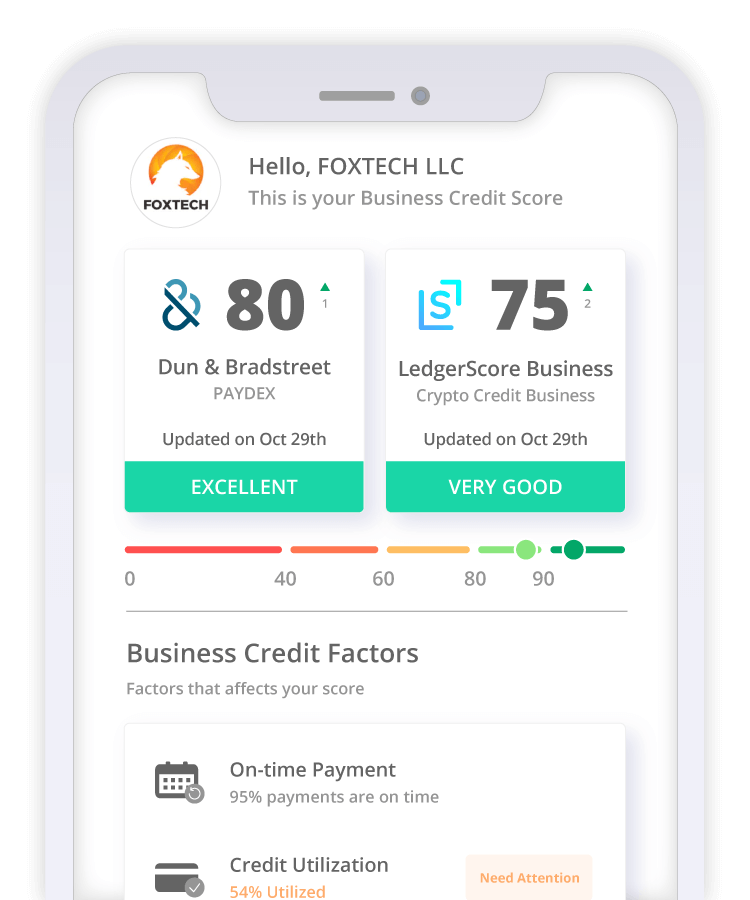

New rating agencies, such as Gio Ratings, are developing crypto credit ratings based on on-chain data. These scores assess counterparty risk for exchanges and custodians, providing a layer of transparency that traditional credit bureaus lack. However, these ratings are primarily designed for institutional investors evaluating platform safety, not for individual consumers seeking to build a personal credit score. For individuals, on-chain activity remains largely invisible to traditional lenders unless explicitly shared through specialized "crypto-native" credit scoring platforms.

Market Growth and Regulatory Clarity

The crypto credit card market is expanding rapidly, with estimates suggesting the sector will grow from $3.81 billion in 2026 to $10.71 billion by 2035. This growth is driven by clearer regulatory frameworks, such as the PwC Global Crypto Regulation Report 2026, which focuses on stablecoin reserves and supervisory standards. As regulations tighten, crypto rewards from staking and lending are becoming more reportable, potentially impacting your taxable income and, indirectly, your ability to qualify for traditional loans if income verification becomes stricter.

| Factor | Traditional Credit | Crypto-Native | Credit Impact |

|---|---|---|---|

| Basis | Income & Payment History | On-Chain Activity & Collateral | Low to High |

| Accessibility | Requires SSN & Credit History | Open to Unbanked Users | None |

| Risk | Default Risk | Liquidation Risk | Variable |

| Reporting | Auto-Reported to Bureaus | Manual or Specialized Platforms | Low |

How to choose a staking tool that protects your credit

Your staking strategy should balance yield with risk management. Under 2026 regulatory standards, credit impact depends on how you structure positions. Choose tools that offer transparency, low liquidation risk, and clear reporting.

Verify the platform’s licensing. Regulators now require clear disclosure of reserve backing and custody practices. Non-compliant platforms pose higher counterparty risk, which can negatively affect your credit profile if assets are lost.

Look for platforms with conservative loan-to-value (LTV) ratios. High LTVs increase the chance of forced liquidation during market volatility, which can trigger debt collection or credit reporting issues. Lower LTVs provide a safer buffer.

Ensure the platform provides clear records of rewards and fees. Transparent reporting helps you track income for tax purposes and demonstrates financial responsibility to potential lenders who may review your crypto activity.

Calculate net yield after fees. High fees can erode returns, making the risk of staking less worthwhile. Use comparison tools to find platforms that offer competitive rates without hidden charges.

Spot Misleading Claims and Weak Options

The 2026 crypto report from PwC highlights how stablecoin reserve requirements and supervisory frameworks are reshaping risk assessment. This regulatory shift exposes common mistakes in how staking rewards are reported to credit bureaus. Many platforms still treat staking yields as standard interest, which can distort your credit utilization ratio and lead to inaccurate scoring.

Watch out for weak options that promise "crypto-native" credit scores without transparent data sources. Some services use on-chain activity to infer creditworthiness, but these models often lack the stability of traditional bureau data. If a platform claims to boost your score through staking alone, verify their methodology against official regulatory standards.

Misleading claims often ignore the volatility of underlying assets. A high staking reward does not equate to lower credit risk if the asset price crashes. Always check if the provider uses real-time risk adjustments or static historical averages. The latter can leave you exposed to sudden score drops when market conditions change.

Crypto credit score 2026: what to check next

The regulatory landscape for digital assets is shifting rapidly, particularly regarding how staking rewards are treated under new compliance frameworks. Understanding these nuances is essential for managing your financial health in 2026.

No comments yet. Be the first to share your thoughts!