Why DeFi credit score 2026 matters now

The financial landscape is shifting beneath our feet. Institutional giants like BlackRock and Morgan Stanley estimate the private credit market will exceed $2.3 trillion by 2026, signaling a massive migration of capital away from traditional banking channels. This surge is not just about volume; it is about access. For the first time, on-chain credit scoring is moving from a niche experiment to a critical infrastructure layer for this trillion-dollar opportunity.

Traditional FICO scores have long served as the gatekeeper for credit, but they are increasingly ill-suited for a global, digital-first economy. Legacy KYC (Know Your Customer) processes are slow, expensive, and often exclude billions of unbanked or underbanked individuals who lack a formal credit history. In contrast, DeFi credit scores leverage on-chain data—transaction history, collateralization ratios, and smart contract interactions—to create a more dynamic and inclusive credit profile.

The urgency for this shift is evident in the rapid growth of decentralized finance. DeFi outstanding loans grew 37% in 2025, driven largely by real-world asset (RWA) tokenization and institutional demand for yield. As 2026 unfolds, the conversation has moved beyond speculation to practical application. On-chain scoring offers a transparent, real-time alternative that can unlock liquidity for those traditional systems overlook.

This transition is not merely technological; it is structural. By replacing static, historical credit scores with live, on-chain reputation metrics, DeFi is creating a more efficient capital allocation system. This efficiency is what will determine whether the $2.3 trillion private credit market can truly scale. The DeFi credit score 2026 model is not just an alternative; it is becoming the standard for a borderless financial system.

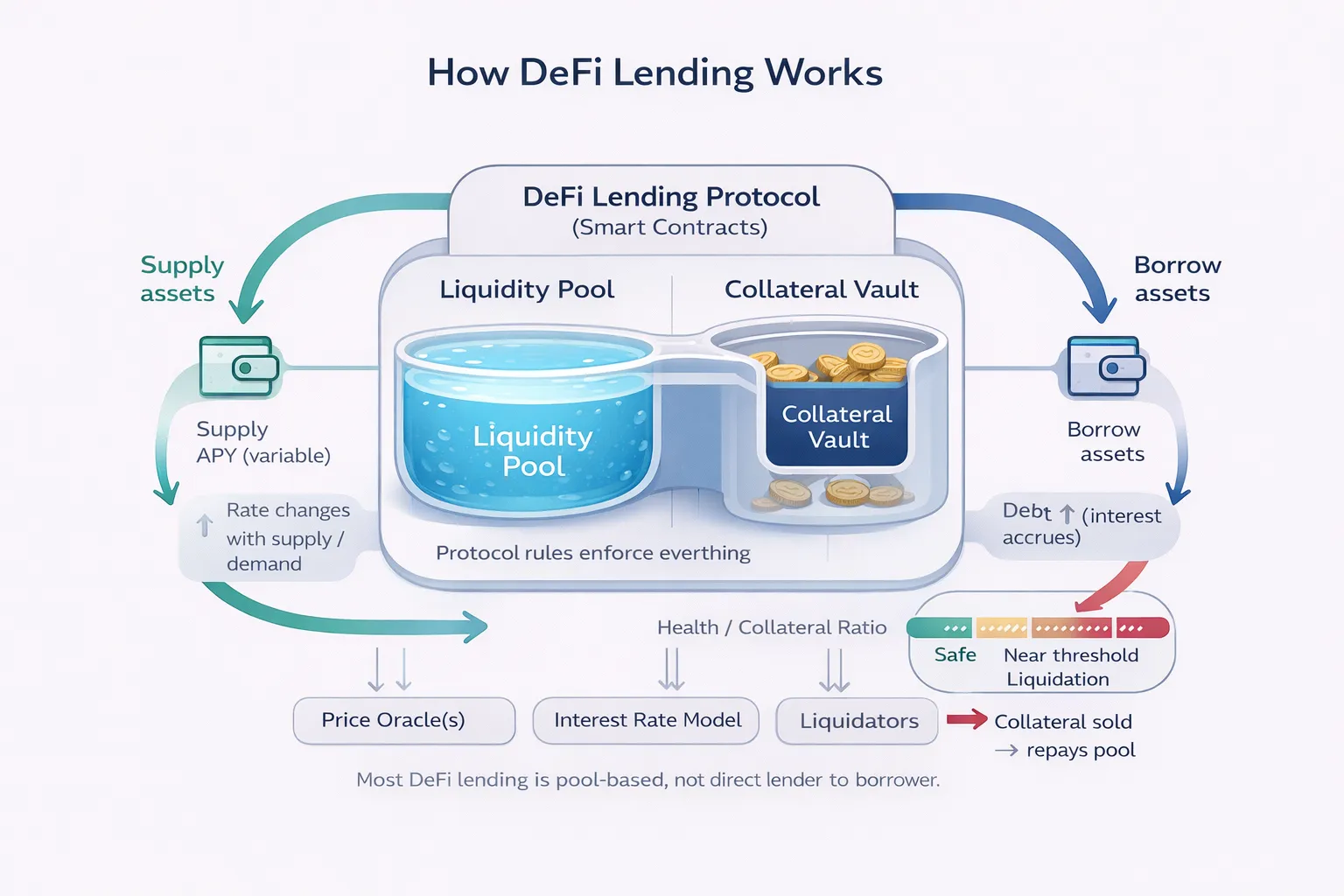

How on-chain credit history works

Traditional credit scores rely on centralized bureaus that pull personal identity data. On-chain credit history operates differently. It analyzes wallet behavior to generate a probabilistic risk grade without requiring personal identity. This approach measures financial discipline through public transaction records rather than private demographic information.

The core mechanism is the On-Chain Credit Risk Score (OCCR). Developed through research such as the paper on arXiv, the OCCR score quantifies credit risk by examining historical on-chain activity. It looks at repayment consistency, debt-to-equity ratios, and transaction frequency. These metrics create a dynamic profile that updates in real time as the wallet interacts with decentralized finance protocols.

Artificial intelligence plays a central role in this process. AI models analyze vast amounts of wallet behavior data to identify patterns that indicate reliability or risk. Instead of a simple binary pass/fail, the system generates a probabilistic grade. This grade reflects the likelihood of default based on past performance in smart contract environments. The analysis remains transparent, as every data point is visible on the blockchain ledger.

This method shifts the focus from who you are to what you do. By stripping away personal identity, on-chain scoring reduces bias and increases accessibility. Lenders can assess risk based on verifiable financial actions, while borrowers maintain their privacy. The result is a more inclusive credit system that rewards consistent financial behavior regardless of geographic location or traditional banking history.

Top DeFi credit score platforms compared

Selecting a DeFi credit score infrastructure provider depends on your specific borrowing needs and privacy preferences. The market has consolidated around four primary protocols that handle on-chain data differently. Each offers distinct advantages for borrowers seeking capital without traditional FICO checks.

ChainAware

ChainAware focuses on institutional-grade data aggregation. It pulls from a wide range of DeFi protocols to create a comprehensive risk profile. This approach suits borrowers who need high loan-to-value ratios and are comfortable with extensive data sharing. Their infrastructure is designed for scalability and accuracy in volatile markets.

Cred Protocol

Cred Protocol emphasizes privacy-preserving score generation. It uses zero-knowledge proofs to verify creditworthiness without exposing raw transaction history. This is ideal for users who prioritize anonymity but still want access to unsecured loans. The platform has gained traction among privacy-focused DeFi participants.

Spectral

Spectral integrates credit scoring directly into its lending market. Borrowers receive a score based on their collateral history and repayment behavior within the ecosystem. This closed-loop system simplifies the borrowing process for users already active in DeFi. It offers competitive rates for those with a strong on-chain track record.

RociFi

RociFi targets real-world asset (RWA) tokenization. It bridges traditional credit data with on-chain lending, allowing borrowers with some off-chain credit history to access DeFi capital. This hybrid model is useful for individuals with established financial footprints outside crypto. It expands the addressable market for both lenders and borrowers.

| Platform | Scoring Method | KYC Required | Target Borrower |

|---|---|---|---|

| ChainAware | Multi-protocol Aggregation | Yes (Institutional) | High-Net-Worth |

| Cred Protocol | Zero-Knowledge Proofs | No | Privacy-Focused |

| Spectral | On-Chain History | No | DeFi Natives |

| RociFi | Hybrid (RWA + On-Chain) | Yes | RWA Investors |

DeFi NPL Rates vs. Traditional Banking

DeFi credit scores are built on real-time on-chain collateralization, a mechanism that fundamentally alters loan performance metrics compared to traditional finance. The most striking validation of this model appears in non-performing loan (NPL) data. According to a 2026 report by the Bank of Canada, Aave V3 reported zero non-performing loans in recent audits, while the average NPL ratio for major U.S. banks stood at 0.59%.

This disparity stems from the structural differences in how risk is managed. In traditional banking, loans are often originated with little to no collateral, relying on credit scores and income verification that can be manipulated or become outdated. When a borrower defaults, the bank must seize assets, a process that is slow, costly, and rarely recovers the full loan value. In contrast, DeFi lending protocols require over-collateralization. If the value of the collateral drops below a certain threshold, the protocol automatically liquidates the assets before the loan can go unpaid.

The result is a system where bad debt is theoretically impossible as long as the liquidation mechanism functions correctly. While this doesn't mean DeFi lending is risk-free—smart contract bugs and oracle failures remain threats—it does mean that credit risk is managed differently. Instead of hoping borrowers will pay, the system ensures that lenders are repaid from the collateral, shifting the risk from creditworthiness to asset volatility.

This structural advantage explains why DeFi platforms can offer competitive rates without the same level of bad debt that plagues traditional banks. It also suggests that as on-chain credit scores mature, they may not need to replicate the FICO model to be effective. Instead, they can leverage the inherent security of collateralized lending to provide a more reliable credit assessment tool.

Best DeFi loans 2026 for borrowers

Choosing the right protocol depends on whether you want to lock up collateral or leverage your on-chain history. The landscape splits into two distinct paths: overcollateralized vaults that require no identity, and undercollateralized loans that reward your DeFi credit score.

Aave V3: The Standard for Overcollateralized Lending

Aave remains the most liquid option for borrowers who want to access cash without KYC. You deposit assets like ETH or USDC into a vault and borrow against them. The interest rates are dynamic, adjusting based on supply and demand.

This model is straightforward but capital-intensive. You must lock more value than you borrow, which limits leverage. However, the deep liquidity means you can exit positions quickly without slippage.

Compound V3: Optimized for Efficiency

Compound focuses on capital efficiency by concentrating liquidity in specific markets. Its V3 architecture uses a single collateral asset per market, simplifying risk management for lenders and borrowers alike.

The platform is known for its stability and transparent governance. If you are borrowing stablecoins against volatile assets, Compound often offers competitive rates due to its streamlined risk model.

Goldfinch: Undercollateralized Credit

Goldfinch allows you to borrow without locking up crypto assets. Instead, it relies on on-chain credit scores and reputation. This is the closest DeFi gets to a traditional unsecured personal loan.

Eligibility depends on your DeFi credit score. If your on-chain history shows consistent repayment behavior, you can access liquidity without tying up your collateral. This is ideal for active traders who need working capital.

Nexo and Celsius: Hybrid Models

Centralized platforms like Nexo offer crypto-backed loans with competitive rates and flexible repayment options. They bridge the gap between DeFi and TradFi by offering fiat withdrawals and customer support.

These platforms require some level of identity verification, but they simplify the borrowing process. If you value ease of use over complete anonymity, a hybrid model might suit your needs.

Securing Your Private Keys

Regardless of the protocol you choose, your private keys are your only identity. If you lose access, you lose your credit history and your collateral. Using a hardware wallet is not optional; it is the foundation of your DeFi credit score.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!