What defines a crypto credit score in 2026

The term "crypto credit score" describes two entirely separate systems that often confuse borrowers. The first is the traditional credit bureau model, which has historically ignored cryptocurrency activity. The second is the emerging on-chain scoring model, which attempts to translate blockchain transaction history into a risk metric for decentralized finance (DeFi) lending.

Traditional Bureau Reporting

Purchasing, trading, or holding cryptocurrency does not generate a tradeline on your Equifax, Experian, or TransUnion report. As noted by credit analysis firms, buying crypto will generally not show on your credit history because most exchanges are not required to report payment data to the major bureaus. This silence creates a "credit invisibility" gap for many digital asset holders.

However, this gap can be bridged through specific lending products. Certain centralized crypto lenders and secured loan providers now report collateralized loan activity to credit bureaus. If you take out a loan backed by crypto assets and the lender reports to the bureaus, your repayment history can build or damage your traditional score. The risk here is direct: failure to repay can lead to liquidation of your collateral and a significant drop in your creditworthiness.

On-Chain Scoring Models

On-chain scoring operates independently of the traditional financial system. It analyzes public blockchain data—such as wallet age, transaction frequency, and collateralization ratios—to assign a risk score. This system aims to bridge the gap in risk assessment, rendering DeFi lending more robust and inclusive for users without traditional credit histories.

These models are primarily used within decentralized finance protocols. Lenders use on-chain scores to determine loan-to-value (LTV) ratios and interest rates without a credit check. While this allows access to capital for unbanked users, it introduces new risks. On-chain scoring does not protect your traditional credit score, but poor performance in DeFi can lead to immediate, automated liquidation of your digital assets, effectively cutting off your access to capital in the crypto ecosystem.

How collateral loans build on-chain history

Crypto Credit Score works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative.

After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

How DeFi Lending Intersects with Traditional Credit

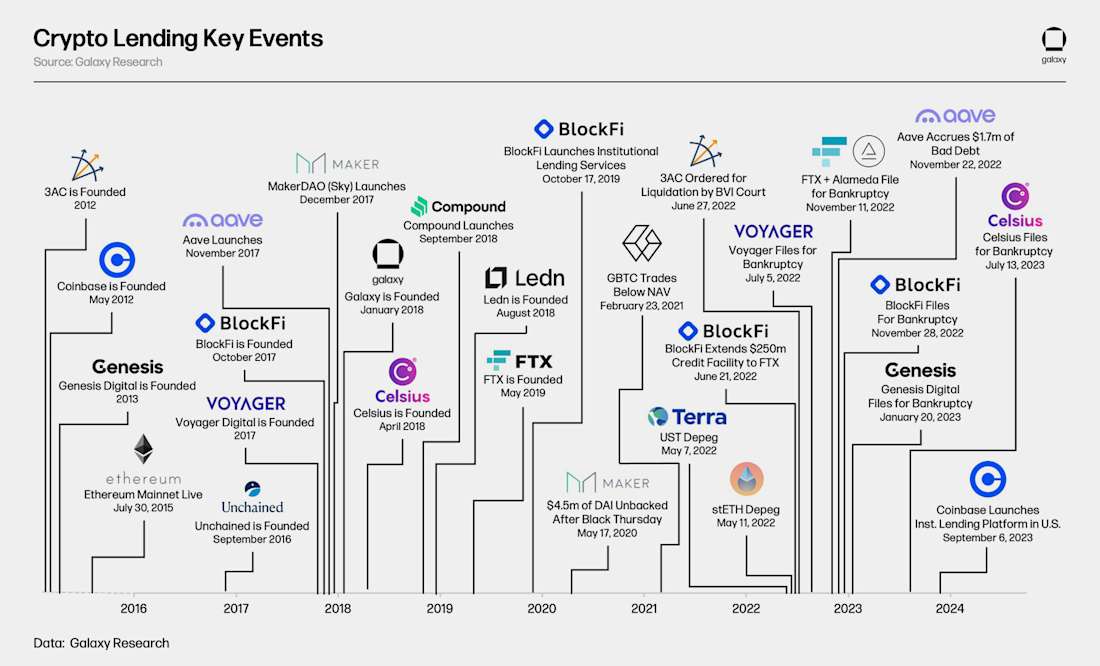

The relationship between decentralized finance (DeFi) and traditional credit scores is often misunderstood. Most DeFi lending protocols operate on a permissionless, non-custodial basis. In this environment, borrowers provide crypto collateral to secure loans without identity verification (KYC). Because these transactions occur on public blockchains without linking to a legal identity, they do not report to FICO or VantageScore. Consequently, responsible repayment on platforms like Aave or Compound does not build a tradeline in the traditional banking system.

A distinct category of platforms bridges this gap. Centralized finance (CeFi) entities and regulated lenders often offer "crypto-backed loans" that require strict KYC/AML compliance. These platforms act as intermediaries, reporting loan performance to major credit bureaus. For these specific products, on-chain activity can influence traditional credit metrics, but the risk profile differs significantly from unsecured personal loans.

The financial stakes in bridging these two worlds are high. While DeFi loans carry the risk of smart contract failure, CeFi crypto loans carry the risk of credit damage. If the value of the underlying crypto collateral drops, these platforms may trigger a margin call or liquidation. Failure to cover the shortfall can lead to default, which is then reported to credit bureaus, causing immediate and lasting damage to the borrower's credit score.

| Feature | Pure DeFi Lending | CeFi / Regulated Crypto Lending |

|---|---|---|

| Identity Verification | None (Anonymous) | Required (KYC/AML) |

| Credit Reporting | No | Yes (FICO/VantageScore) |

| Collateral Type | Crypto Assets | Crypto Assets |

| Primary Risk | Smart Contract Exploit | Credit Score Damage / Liquidation |

For borrowers seeking to build credit, only the regulated, KYC-compliant options matter. Pure DeFi remains a tool for capital efficiency, not credit building. Users must carefully distinguish between these models to avoid unintended consequences for their financial health.

The Hidden Costs of Crypto-Backed Borrowing

Borrowing against crypto assets introduces a distinct set of risks that diverge sharply from traditional secured lending. While these loans bypass credit checks, they expose borrowers to the extreme volatility of digital assets and the opacity of platform reporting mechanisms. The primary danger lies in the mechanics of liquidation and the potential for on-chain defaults to damage your established credit profile.

Liquidation Risk and Volatility

In crypto-backed lending, your collateral is subject to real-time market fluctuations. A sharp decline in asset value can trigger an automatic liquidation, forcing the sale of your holdings to cover the loan. Unlike traditional mortgages, where you might have time to refinance or sell manually, crypto liquidations are often instantaneous and irreversible. This risk is amplified by the inherent volatility of cryptocurrencies, where significant price swings can occur within minutes.

To understand the current market volatility context, consider the live price movement of Bitcoin:

Credit Reporting and Default Consequences

A growing number of crypto lending platforms are beginning to report loan performance to major credit bureaus. This shift means that missed payments or defaults on crypto-backed loans can now negatively impact your traditional credit score. The PwC Global Crypto Regulation Report 2026 highlights the increasing regulatory scrutiny on how digital asset lending intersects with traditional financial systems, including credit reporting obligations. Borrowers must carefully review platform terms to understand if their activity is being reported and how defaults are handled.

The legal framework surrounding these loans is still evolving. As noted in academic discussions on crypto-native credit scoring, the goal is often to bridge the gap in risk assessment, but this comes with significant liability for the borrower. If a platform fails to report accurately or if a liquidation event is mishandled, the financial and credit consequences can be severe. Borrowers should treat crypto-backed loans with the same caution as any high-stakes financial obligation, understanding that the "non-recourse" nature of some loans does not always protect your broader credit history.

Regulatory shifts and the 2026 landscape

The regulatory environment for crypto credit is undergoing a fundamental restructuring. The PwC Global Crypto Regulation Report 2026 highlights a decisive pivot toward standardized oversight, particularly for stablecoins and lending protocols. This shift moves the industry away from opaque, self-regulated risk models toward transparent, auditable frameworks that align with traditional financial compliance standards PwC 2026 Report.

For borrowers and lenders, this standardization carries significant stakes. Regulatory mandates now require continuous monitoring of on-chain behavior, replacing periodic audits with real-time risk assessment. As noted by Agio Ratings, institutions are increasingly relying on model-driven monitoring that tracks behavioral signals between formal audit dates to detect early signs of distress. This continuous oversight reduces the likelihood of sudden, unannounced liquidations that previously characterized the unregulated sector.

The convergence of on-chain data and traditional credit scoring creates a more predictable, albeit stricter, lending environment. Lenders can now price risk more accurately based on verified transaction history rather than speculative reputation. However, this transparency also means that credit damage is more immediate and severe. A single missed payment or liquidity shortfall is recorded on-chain and reported to regulatory bodies, potentially affecting a user’s ability to access capital in both crypto and traditional markets. The era of hidden leverage is ending, replaced by a landscape where financial health is continuously verified and publicly accountable.

Frequently asked: what to check next

What is the 2026 crypto report?

The PwC Global Crypto Regulation Report 2026 explores the rapidly evolving regulatory landscape for digital assets, with a particular focus this year on stablecoins – their issuance models, reserve and redemption requirements, and supervisory frameworks – alongside key policy shifts and emerging trends in over 50 jurisdictions.

Can buying or trading crypto affect my credit score?

Buying crypto will generally not show on your credit history. Traditional credit bureaus do not track spot transactions, so your score remains unaffected by direct purchases or trading.

Do crypto loans impact traditional credit scores?

Only if the lender reports to credit bureaus. Many DeFi protocols do not report to traditional agencies, but regulated crypto-lending products may. Defaults on these specific products can damage your credit, while on-chain liquidations typically do not.

How do crypto-native credit scores work?

Crypto-native credit scoring aims to bridge the gap in risk assessment by using on-chain data. It renders DeFi lending more robust and inclusive by evaluating wallet history and collateral behavior instead of traditional credit history.

No comments yet. Be the first to share your thoughts!