What is a DeFi credit score

A DeFi credit score is a risk assessment metric derived exclusively from on-chain data and smart contract history. Unlike traditional FICO scores, which rely on centralized banking records and consumer credit reports, DeFi scores evaluate a wallet’s financial behavior through transparent, immutable ledger entries. This distinction is fundamental for compliance and risk management in decentralized finance.

These scores are generated by analyzing historical interactions with lending protocols, including repayment consistency, collateralization ratios, and transaction frequency. The methodology mirrors traditional credit underwriting but substitutes bank statements with blockchain activity. As noted in legal analyses of crypto-native credit systems, this approach aims to bridge the gap in risk assessment, rendering DeFi lending more robust and inclusive for users without traditional credit histories.

The reliance on smart contract history means that a DeFi credit score is inherently tied to the specific protocols a user engages with. A positive history of repaying loans on Aave or Compound, for example, contributes to a higher score within those ecosystems. This data is not shared with Equifax or TransUnion; it remains siloed within the blockchain environment unless explicitly bridged to a decentralized identity solution.

Understanding this mechanism is critical for high-stakes financial decisions. Because DeFi scores are based on real-time, verifiable data, they offer a more immediate reflection of current financial health than traditional scores, which may lag behind recent economic changes. However, this transparency also means that every transaction impacts your score, requiring careful management of on-chain liabilities.

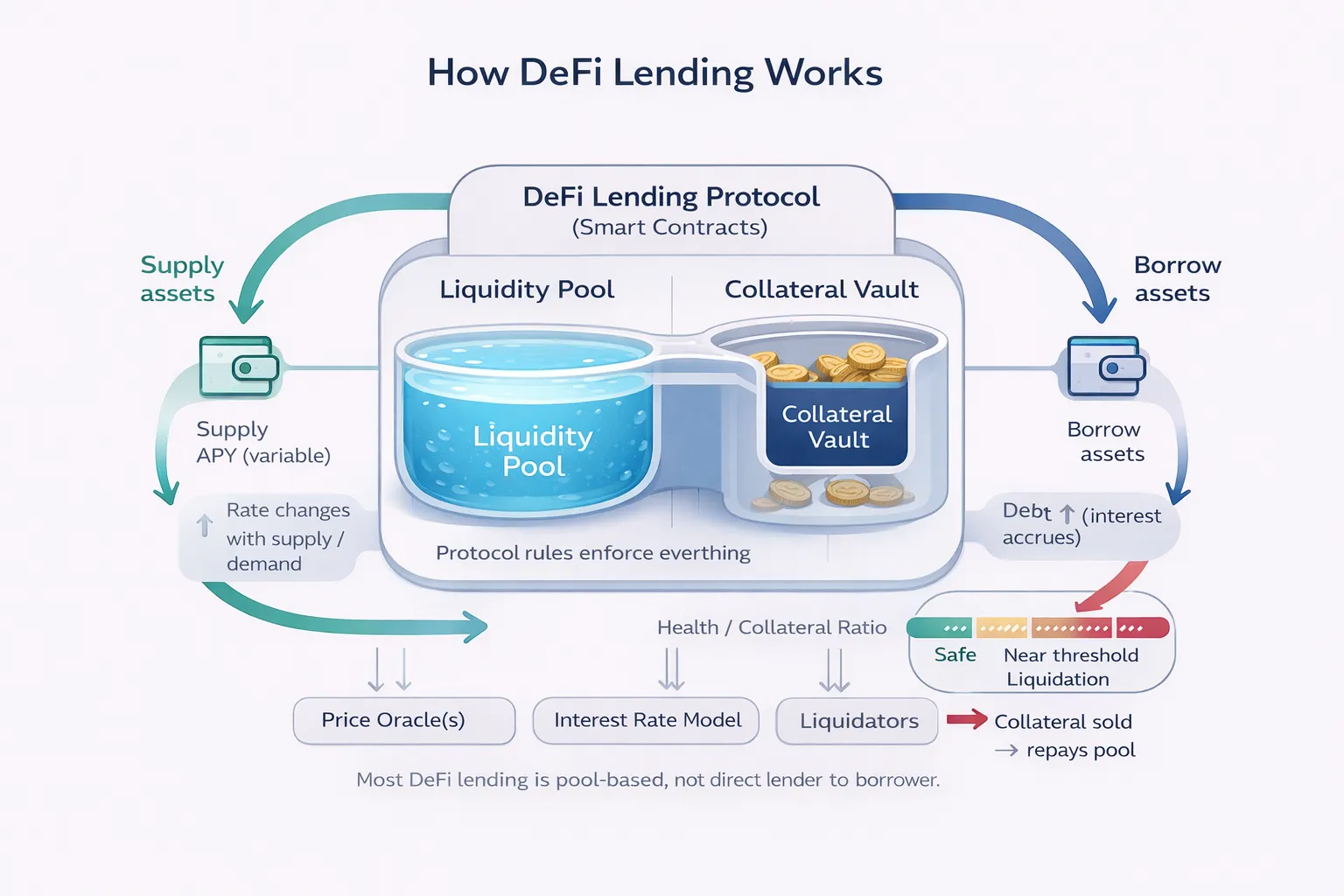

How on-chain credit reporting works

On-chain credit reporting operates by translating public blockchain activity into a quantifiable risk metric. Unlike traditional credit bureaus that rely on identity verification (KYC) and off-balance-sheet liabilities, DeFi protocols assess solvency through transparent, immutable ledger data. This mechanism allows for the generation of credit scores without exposing personal identity, a feature that distinguishes decentralized finance from conventional banking infrastructure.

The technical foundation for this assessment is often anchored in probabilistic models such as the On-Chain Credit Risk Score (OCCR). As detailed in recent academic research, the OCCR score quantifies credit risk by analyzing a wallet’s historical interaction with lending protocols, including repayment consistency, collateralization ratios, and transaction velocity. These metrics are processed through algorithms that weigh behavioral patterns against known failure modes, producing a dynamic score that updates in real-time as on-chain activity changes.

Risk assessment in this environment is driven by volatility and protocol-specific parameters. Lenders do not merely look at the current value of collateral but model the probability of liquidation events under various market stress scenarios. This requires sophisticated data aggregation that links disparate blockchain networks to create a unified view of a user’s financial footprint. The resulting score serves as a gatekeeper for access to higher leverage or lower interest rates, effectively replacing the human underwriter with code.

To contextualize the volatility that drives these risk models, it is necessary to observe the asset classes typically used as collateral. The price action of major assets like Bitcoin directly influences the health of the lending protocols that accept them as security.

The integration of these probabilistic scores into smart contracts ensures that lending terms are enforced automatically. If a user’s on-chain behavior indicates a decline in their OCCR score—such as withdrawing collateral or failing to repay a micro-loan—the protocol can adjust their borrowing limits or interest rates without manual intervention. This creates a self-regulating financial ecosystem where creditworthiness is defined by code and transaction history rather than institutional reputation.

DeFi Lending Without KYC and Credit Impact

The foundational architecture of decentralized finance (DeFi) is built on pseudonymity. Traditional lending requires Know Your Customer (KYC) verification, where borrowers submit government-issued identification and financial documents to establish a credit history. In contrast, most non-KYC DeFi protocols operate on a permissionless basis. Users interact with smart contracts using only a digital wallet address, eliminating the need for identity verification or traditional credit checks.

This structural difference means that standard DeFi lending activity does not report to major credit bureaus such as Equifax, Experian, or TransUnion. A borrower who defaults on an overcollateralized loan in a non-KYC protocol will not see their FICO score drop, nor will they appear on a national credit registry. The risk is contained within the blockchain ecosystem through smart contract enforcement rather than legal recourse or credit reporting.

However, the landscape is evolving. Emerging platforms are developing "on-chain credit scores" that attempt to bridge this gap. These systems analyze on-chain activity—such as repayment history, asset holdings, and transaction frequency—to generate a creditworthiness metric. While these scores do not yet directly influence traditional credit reports, they enable under-collateralized lending within the DeFi ecosystem itself. For example, protocols leveraging EigenLayer AVS (Actively Validated Services) are testing systems like zScore to create portable, on-chain credit identities.

This shift represents a parallel credit system. While it does not currently impact your traditional credit history, it establishes a reputation layer within DeFi. As regulatory frameworks mature, the distinction between on-chain reputation and traditional credit may blur, but for now, non-KYC lending remains isolated from conventional credit reporting mechanisms.

Comparing DeFi credit score platforms

The on-chain credit scoring landscape is fragmented, with protocols diverging significantly in their data transparency, identity verification (KYC) requirements, and supported blockchain networks. For institutional and high-stakes participants, understanding these structural differences is essential for regulatory compliance and risk assessment.

The following comparison outlines the primary distinctions between leading on-chain credit score providers. This analysis focuses on established mechanisms for data aggregation and scoring methodology as they exist in the current regulatory environment.

| Provider | Primary Data Source | KYC Required | Supported Chains |

|---|---|---|---|

| ChainAware | Multi-chain wallet activity | No | Ethereum, Polygon, Arbitrum |

| Cred | On-chain lending history | Optional | Ethereum, Optimism |

| BanklessDAO Score | Community governance participation | No | Ethereum |

| Goldfinch Credit Score | Real-world asset (RWA) backing | Yes | Ethereum |

Providers like ChainAware and Cred rely heavily on anonymized on-chain transaction history, allowing users to build a credit profile without identity verification. This approach prioritizes privacy but may limit the depth of the credit score in jurisdictions requiring strict know-your-customer (KYC) compliance. Conversely, platforms such as Goldfinch require KYC to back their credit scores with real-world assets, offering a more traditional risk model suitable for institutional capital.

Data transparency remains a critical variable. Platforms that publish their scoring algorithms and data sources allow for greater auditability, which is a prerequisite for many legal and regulatory frameworks. Users should verify that the data sources used by any given platform are immutable and verifiable on-chain to ensure the integrity of the credit score.

Regulatory and Financial Vulnerabilities

Decentralized credit scoring introduces distinct regulatory and financial risks that differ fundamentally from traditional banking models. The primary concern lies in the opacity of the algorithms governing these systems. Unlike regulated credit bureaus, which are subject to the Fair Credit Reporting Act (FCRA) and require transparency in scoring methodologies, decentralized finance (DeFi) protocols often operate as "black boxes." This lack of explainability means borrowers cannot easily understand why their creditworthiness was assessed a certain way, nor can they effectively dispute inaccurate on-chain data.

The automation of credit decisions via smart contracts removes human oversight, potentially amplifying systemic biases embedded in the training data. If historical lending data contains discriminatory patterns, the algorithm will replicate and scale these biases without the remedial mechanisms available in conventional finance. This creates a high-stakes environment where financial exclusion can occur without recourse, as the code executes precisely as written, regardless of equitable considerations.

Additionally, the financial risks include the potential for predatory lending practices facilitated by these opaque models. Without the protective guardrails of traditional consumer credit laws, users may face exorbitant interest rates or sudden liquidation events driven by volatile collateral values. The absence of a central authority to mediate disputes or provide consumer protection leaves borrowers vulnerable to exploitation. As noted in academic analyses, this "black box 3.0" model shifts the burden of risk entirely onto the individual, with minimal regulatory safety nets.

To monitor the broader market context and volatility that influences these lending protocols, investors and users should track relevant asset performance.

Regulatory and Compliance Considerations

How is DeFi credit scoring regulated?

Currently, DeFi credit scoring operates in a regulatory gray area. Unlike traditional credit bureaus, which are regulated under the Fair Credit Reporting Act (FCRA) in the United States, on-chain credit providers are not subject to the same oversight. This means there are no federal requirements for transparency in scoring algorithms or mechanisms for disputing inaccurate data. Users must conduct due diligence to ensure the provider’s data sources are reliable and that the scoring methodology does not violate local financial regulations.

Does DeFi activity affect my traditional credit score?

Standard DeFi lending activity does not report to traditional credit bureaus such as Equifax, Experian, or TransUnion. Because DeFi operates without traditional intermediaries like banks, on-chain lending and borrowing activities remain invisible to standard credit reporting systems. Consequently, positive repayment behavior in DeFi protocols will not directly improve a traditional credit score, nor will defaults typically result in a credit bureau penalty. However, emerging platforms that bridge on-chain reputation with traditional identity verification may begin to report data in the future.

Is DeFi legal in the US?

Decentralized finance is not illegal in the United States. There are no federal restrictions or guidelines prohibiting individuals from using DeFi protocols or holding cryptocurrency wallets. However, the regulatory landscape is complex, and while access is open, participants are expected to conduct due diligence. Regulatory bodies caution that the technology may not be suitable for all investors due to inherent risks, and users must understand the legal implications of their interactions with smart contracts.

No comments yet. Be the first to share your thoughts!