The 2026 DeFi Credit Score Landscape

By 2026, the architecture of on-chain credit has diverged sharply from traditional FICO models. The industry has moved away from identity-based scoring toward probabilistic risk assessment, where creditworthiness is derived from verifiable transaction history rather than personal attributes. This shift is not merely cosmetic; it fundamentally alters how risk is priced and who gains access to capital.

As of March 2026, the total value locked (TVL) across all DeFi protocols stands at approximately $98 billion, according to a Congressional Research Service report. This capital deployment reflects a maturing market that prioritizes algorithmic transparency over institutional discretion. The growth of outstanding loans by 37% in 2025 signals a sustained demand for decentralized lending, driven largely by scalable models that integrate AI-driven credit scoring to mitigate default risks.

Unlike traditional credit bureaus, which rely on static snapshots of debt and payment history, DeFi credit scores are dynamic. They update in real-time as on-chain activity occurs. This immediacy allows for more granular risk pricing but introduces new regulatory complexities. The absence of a centralized authority means that disputes over credit metrics are resolved through code and consensus, not customer service representatives.

The landscape is further complicated by the emergence of tranched credit markets, which segment risk by seniority. This structure allows investors to choose their exposure level, but it also requires borrowers to understand how their on-chain behavior impacts their position within the risk hierarchy. The result is a credit environment that is both more inclusive and more volatile than its off-chain counterpart.

How on-chain credit history is generated and reported

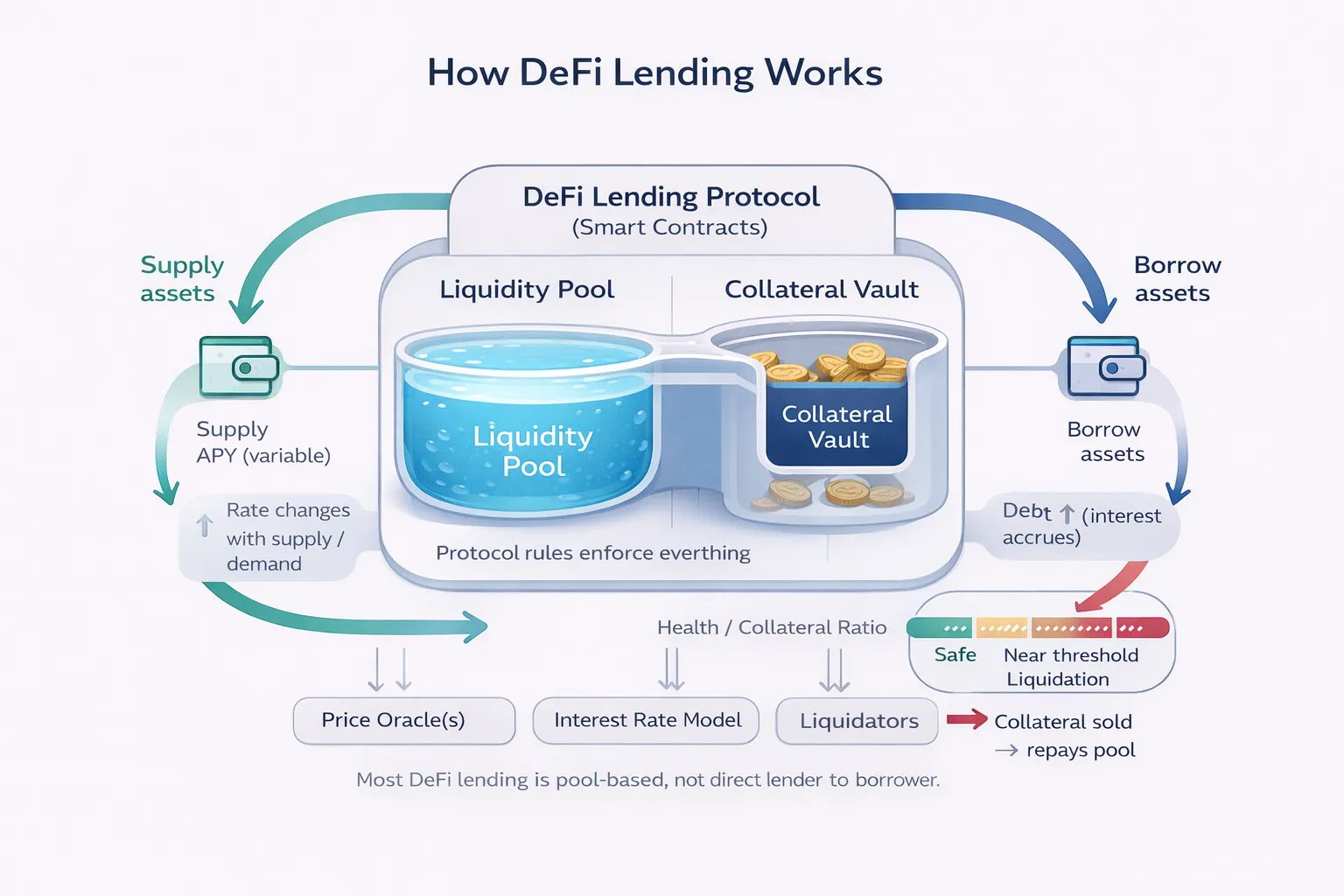

On-chain credit history is not a static record maintained by a central bureau; it is a dynamic output of decentralized lending protocols. When a user interacts with a DeFi lending protocol, every action—depositing collateral, borrowing assets, or repaying debt—is immutably recorded on the blockchain. These events constitute the raw data points for credit assessment. Unlike traditional credit reports, which aggregate data from disparate lenders, on-chain history is native to the protocol itself, offering a transparent and complete ledger of financial behavior.

The technical infrastructure enabling this reporting relies on smart contracts that log transaction hashes and account balances. Recent academic research, such as the introduction of the On-Chain Credit Risk Score (OCCR Score), demonstrates how these raw logs are transformed into probabilistic measures of credit risk. The OCCR Score quantifies the likelihood of default by analyzing variables like loan-to-value ratios, repayment frequency, and historical volatility, all derived directly from on-chain activity [src-serp-6]. This mechanism shifts credit assessment from subjective human evaluation to algorithmic verification.

Reporting this data to third-party credit scoring services requires a bridge between the blockchain and off-chain systems. Protocols must expose their data through standardized interfaces or oracles, allowing credit bureaus to ingest and normalize the information. This process ensures that the credit score reflects the user's actual on-chain behavior rather than speculative metrics. The integrity of this system depends on the accuracy of the data feed; any discrepancy in the reported transaction history can lead to incorrect risk assessments, with significant financial consequences for the borrower.

How DeFi Lending Impacts Your Credit Score

On-chain lending activities directly shape your DeFi credit score through the accumulation of verifiable financial history. Unlike traditional credit bureaus that rely on centralized reporting, DeFi protocols record every interaction on the blockchain. This transparency allows scoring algorithms to assess your reliability based on actual collateralization ratios and repayment behavior. However, the high-stakes nature of smart contract interactions means that a single default can permanently alter your risk profile.

The impact of borrowing extends beyond simple loan history. Protocols analyze the stability of your collateral assets and the frequency of your liquidity provision. Consistent over-collateralization signals financial discipline, while frequent margin calls or liquidations raise red flags. As the industry matures, these on-chain behaviors are becoming the primary metrics for determining creditworthiness in decentralized finance.

To understand how different platforms evaluate these risks, it is essential to compare their scoring methodologies. The table below outlines the key differences between major DeFi credit scoring providers as of 2026.

| Protocol | Scoring Methodology | Output Type | Primary Risk Focus |

|---|---|---|---|

| ChainAware | Behavioral + Collateral | Composite Score | Default Probability |

| Cred | On-Chain History | Credit Tier | Liquidity Stability |

| Spectral | Real-World Assets | Risk Rating | Asset Quality |

Build a verifiable credit history through responsible borrowing

Establishing a positive DeFi credit score in 2026 requires treating on-chain activity as a formal credit relationship. Lenders evaluate borrowers based on verifiable repayment behavior, not speculative volume. To build a score that holds weight in regulated lending environments, you must prioritize protocol selection and consistent repayment over aggressive leverage.

Select audited protocols with transparent data feeds

Your credit history is only as reliable as the data source. In 2026, lenders increasingly rely on audited oracles and compliant lending protocols that report to recognized credit bureaus or decentralized identity standards. Avoid unverified, high-yield pools that obscure their risk models. Use only protocols with clear, auditable smart contract histories and public documentation of their data reporting mechanisms.

Repay loans early to demonstrate reliability

Consistent, on-time repayment is the strongest signal of creditworthiness. Unlike traditional credit, DeFi loans are often over-collateralized, but timely repayment still matters for score calculation. Set up automated repayment schedules or calendar reminders to avoid missed payments. Even small, regular repayments build a positive track record faster than occasional large ones.

Keep debt-to-income ratios low

Your credit score reflects your ability to manage debt relative to your income or total assets. In DeFi, this translates to the ratio of borrowed assets to your total portfolio value. Maintain a conservative loan-to-value (LTV) ratio, ideally below 50%, to show lenders you are not overextended. High LTV ratios signal risk and can negatively impact your score, even if you repay on time.

Monitor your credit report regularly

Just as you would review a traditional credit report, check your on-chain credit history regularly. Some protocols now offer built-in score dashboards or integrate with third-party credit tracking services. Dispute any inaccuracies immediately. Early detection of errors prevents them from compounding into long-term score damage.

TechnicalChart symbol="NASDAQ:BTC" chartStyle="candle" interval="1D" indicators='["volume","rsi"]' />

No comments yet. Be the first to share your thoughts!