The 2026 shift from collateral to identity

The crypto lending market is undergoing a structural transformation, moving away from the rigid, overcollateralized models that defined the previous decade. In 2026, the crypto credit score 2026 framework is replacing blanket collateral requirements with dynamic, on-chain reputation systems. This shift allows lenders to assess borrower risk based on historical behavior rather than just the immediate value of locked assets, unlocking significant capital efficiency for active participants.

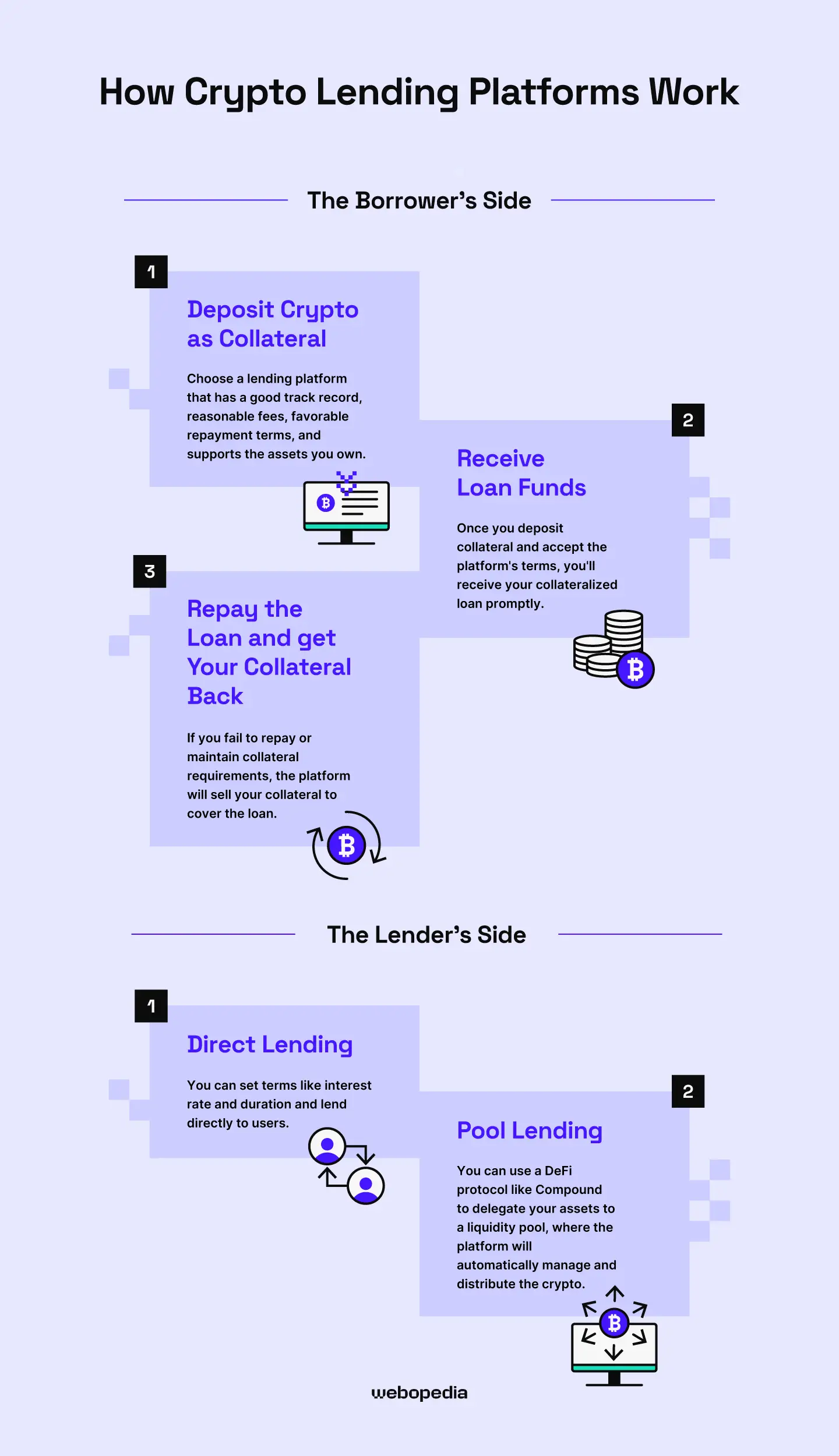

Historically, decentralized finance (DeFi) relied on a simple safety mechanism: borrowers must lock up more value than they borrow. While this minimized lender risk, it trapped capital and excluded users without large upfront holdings. The new paradigm uses on-chain data—transaction history, repayment consistency, and wallet activity—to generate a credit profile. This mirrors traditional credit scoring but operates transparently on the blockchain, allowing for unsecured or undercollateralized loans based on verified identity and trust.

This transition is not merely technological but regulatory. A 2026 report by PwC highlights that regulators are increasingly focusing on stablecoin issuance and supervisory frameworks that require robust risk assessment models. As compliance becomes mandatory, the ability to prove creditworthiness through on-chain history becomes a critical component of market participation. Lenders can now differentiate between high-risk speculators and reliable borrowers, reducing systemic risk while expanding access to credit.

The result is a more mature financial ecosystem where capital is allocated based on merit rather than mere liquidity. For borrowers, this means lower costs and greater flexibility. For lenders, it offers higher yields through diversified, risk-adjusted portfolios. As the industry matures, the on-chain credit metric will likely become the standard for evaluating trust in decentralized markets, bridging the gap between traditional finance rigor and crypto-native innovation.

How the on-chain credit model works

The on-chain credit score is not a FICO equivalent. It is a probabilistic risk model that aggregates wallet activity, repayment history, and social graph data to estimate default likelihood without exposing private keys. Traditional credit bureaus rely on centralized identity verification; on-chain scoring relies on behavioral patterns visible in public ledger transactions.

Scoring engines begin by mapping wallet addresses to a unified identity graph. This process links multiple addresses to a single entity, allowing the model to see the full scope of a user’s financial footprint rather than isolated transactions. The engine then analyzes historical behavior, prioritizing consistent repayment of on-chain loans and stablecoin holdings over speculative trading volume.

To protect privacy, these models use zero-knowledge proofs or similar cryptographic methods. This allows users to prove they meet certain criteria—such as having a debt-to-income ratio below a specific threshold—without revealing the underlying transaction details or private keys. The result is a verifiable score that lenders can trust without accessing sensitive personal data.

The aggregation process also incorporates social graph data. By analyzing the connections between wallets, the model can infer trust levels based on the behavior of associated accounts. If a wallet frequently interacts with high-reputation addresses, it may receive a slight risk adjustment. However, this is secondary to direct repayment history and asset stability.

Regulatory frameworks are beginning to catch up with these technical realities. The same 2026 PwC analysis highlights the need for clear supervisory standards for digital asset lending, emphasizing the importance of transparent risk models. As these standards evolve, the integration of on-chain credit history into traditional financial products will likely become more seamless.

Top platforms for credit-based borrowing

The landscape for borrowing against digital assets has shifted from simple collateralized loans to sophisticated credit lines that rely on on-chain history. In 2026, the most competitive platforms do not just look at your wallet balance; they evaluate your transactional behavior to assign a credit score that determines your borrowing power. This shift allows users to access liquidity without selling their holdings, provided they maintain a clean history of repayments and activity.

The following comparison outlines the leading platforms enabling this credit-based borrowing. These platforms differ in how they calculate risk, the stability of their interest rates, and the maximum Loan-to-Value (LTV) ratios they offer. Understanding these mechanics is essential for selecting a platform that aligns with your financial strategy.

| Platform | Max LTV | Rate Type | Credit Basis |

|---|---|---|---|

| Nexo | 90% | Fixed | On-chain history & KYC |

| Ledger Loans | 75% | Variable | On-chain history only |

| BorrowX | 80% | Variable | DeFi protocol score |

| DeFi Saver | 70% | Variable | Smart contract history |

Risks and regulatory considerations

Building an on-chain credit score model introduces risks that extend far beyond traditional lending. While on-chain history provides a transparent ledger of repayment behavior, the underlying infrastructure remains fragile. Smart contract vulnerabilities, regulatory ambiguity, and the inherent volatility of digital assets create a high-stakes environment where a single exploit or policy shift can invalidate years of positive credit history.

Smart contract and liquidity risk

Unlike traditional banks, DeFi credit protocols operate on immutable code. If a smart contract contains a vulnerability, funds can be drained instantly, leaving borrowers liable for debts that no longer exist in the protocol. This "code is law" reality means that creditworthiness is only as secure as the protocol’s audit trail. Additionally, liquidity crunches during market downturns can trigger forced liquidations, eroding the very on-chain history that lenders rely on to assess risk.

Regulatory uncertainty

The legal landscape for digital assets is shifting rapidly. The 2026 PwC report highlights that regulators are increasingly focusing on stablecoin issuance models, reserve requirements, and supervisory frameworks. While this may bring clarity, it also introduces the risk of retroactive compliance costs or operational restrictions. Lenders must navigate a patchwork of jurisdictions, where a protocol deemed compliant in one region may face severe penalties in another. This uncertainty can lead to sudden protocol shutdowns or changes in terms, disrupting the continuity of credit history.

Over-leverage and volatility

The core mechanism of crypto credit often involves borrowing against volatile assets. A sharp decline in the value of the collateral can trigger margin calls, forcing borrowers to repay debt quickly or face liquidation. This dynamic can exacerbate market downturns, creating a feedback loop that destabilizes both individual positions and the broader ecosystem. Borrowers must maintain a conservative loan-to-value ratio to withstand volatility, but this requirement can limit the utility of credit for everyday financial needs.

Build your on-chain reputation

Your on-chain history is now the primary determinant of your borrowing power. In the 2026 landscape, lenders rely on transparent ledger data rather than traditional bureau reports. To improve your standing, you must treat your wallet address as a financial identity that requires consistent, verifiable activity.

Timely repayment is the strongest signal of reliability. Lenders track your transaction history to calculate your payment consistency. Even a single missed payment on a DeFi protocol can significantly lower your score, making it harder to access uncollateralized loans.

Lenders prefer wallets that show sustained, organic usage over time. Regular interactions with multiple reputable protocols demonstrate stability. Avoid sudden, high-volume transfers that resemble wash trading or suspicious activity, as these can trigger risk flags.

Many platforms now require Know Your Customer (KYC) verification to unlock higher credit limits. Linking your verified identity to your wallet address allows lenders to cross-reference your on-chain behavior with real-world obligations. This step is essential for accessing the best rates under current regulations.

Keep your outstanding debt levels manageable relative to your total assets. High leverage increases your risk profile, potentially leading to lower credit scores or higher interest rates. Regularly monitor your exposure across different lending platforms to ensure you remain within safe borrowing limits.

| Action | Impact on Score |

|---|---|

| On-time repayment | High positive |

| Missed payment | Severe negative |

| KYC verification | Moderate positive |

| High leverage | Negative |

How the 2026 credit score meets regulation

The regulatory environment for on-chain lending has shifted from ambiguity to structured oversight. According to the 2026 PwC report, authorities are no longer treating digital assets as peripheral experiments. Instead, they are establishing clear frameworks for stablecoin issuance, reserve requirements, and redemption mechanisms. This shift directly impacts how the crypto credit score 2026 is validated, as lenders now require proof that underlying collateral adheres to these new supervisory standards.

The report highlights that creditworthiness is no longer just about on-chain transaction history; it is also about legal compliance. Lenders are integrating regulatory checks into their scoring algorithms to mitigate counterparty risk. This means that a high on-chain score must now be paired with verified reserve audits to secure favorable loan terms. The mechanics of credit scoring are becoming inextricably linked with legal adherence, ensuring that the digital assets backing loans are both solvent and compliant.

"The 2026 report explores the rapidly evolving regulatory landscape for digital assets, with a particular focus this year on stablecoins – their issuance models, reserve and redemption requirements, and supervisory frameworks."

This regulatory clarity provides a foundation for institutional adoption. By standardizing how credit scores are derived from on-chain data within a legal framework, the market is moving toward more stable and transparent lending practices. Borrowers who understand these regulatory nuances can better position themselves to access capital, as lenders prioritize assets that meet these rigorous compliance benchmarks.

No comments yet. Be the first to share your thoughts!