DeFi credit scores defined

Use this section to make the DeFi Credit Score decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

On-chain data as credit history

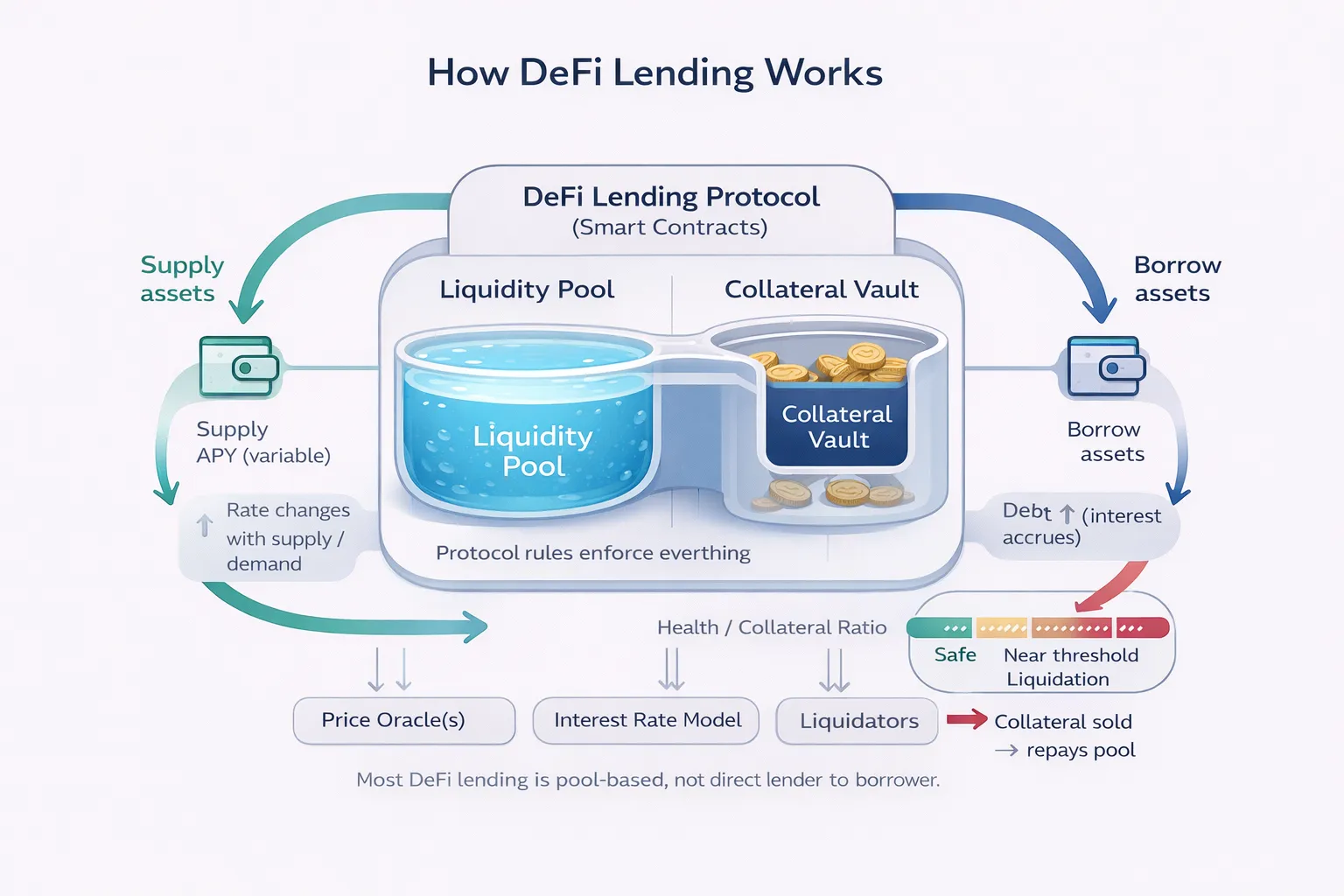

Traditional credit scoring relies on centralized financial records, but decentralized finance (DeFi) builds creditworthiness from public blockchain activity. Every transaction, loan repayment, and asset transfer is immutable and visible, creating a digital footprint that algorithms can analyze to predict future behavior. This on-chain history serves as the primary input for credit models, replacing FICO scores with verifiable, real-time data.

The mechanics of this assessment are formalized in frameworks like the On-Chain Credit Risk Score (OCCR). As detailed in academic research, the OCCR score is a probabilistic measure designed to quantify the likelihood of default based on historical on-chain behavior. It aggregates three core dimensions: repayment history, asset diversity, and wallet age. Repayment history is the strongest predictor; a wallet that consistently repays loans on time or maintains healthy collateral ratios demonstrates reliability. Asset diversity measures the stability of a user’s portfolio, while wallet age provides context on experience and longevity in the ecosystem.

Lending platforms use these aggregated metrics to determine under-collateralized loan terms. A high on-chain credit score can reduce the collateral required for a loan, lowering the cost of capital for trustworthy borrowers. Conversely, erratic behavior or sudden liquidations in past transactions can trigger higher interest rates or loan denials. This system shifts the risk assessment from static collateral to dynamic behavioral analysis, allowing DeFi to offer credit products that mirror traditional banking without the central gatekeepers.

DeFi credit score platforms compared

The infrastructure for on-chain credit scoring is fragmented, with each protocol prioritizing different data sources and privacy trade-offs. For institutions assessing borrower risk, the choice of platform determines which historical behaviors are visible and how much personal identity is exposed.

The following table outlines the primary differences between leading DeFi credit score providers, including Credora, zkCredit, and ChainAware. These platforms vary in their supported blockchains, the granularity of their data aggregation, and their approach to zero-knowledge proofs.

| Platform | Primary Data Sources | Privacy Model | Supported Chains |

|---|---|---|---|

| Credora | Ethereum, Solana, Base transaction history | Public score with optional PII masking | Multi-chain |

| zkCredit | On-chain activity, off-chain identity verification | Zero-knowledge proofs (ZKPs) | Ethereum, L2s |

| ChainAware | Cross-chain wallet behavior, NFT holdings | Federated learning with encrypted data | Ethereum, Polygon, Arbitrum |

Credora focuses on broad transaction history aggregation, making it suitable for borrowers with active multi-chain portfolios. Its model relies on transparent scoring algorithms, which simplifies integration for lending protocols but offers less privacy than zero-knowledge alternatives.

zkCredit utilizes zero-knowledge proofs to verify creditworthiness without revealing underlying transaction details. This approach is critical for high-net-worth individuals or institutions requiring strict data confidentiality. However, the complexity of ZK-proof generation can introduce latency during the underwriting process.

ChainAware emphasizes cross-chain consistency, aggregating data from Ethereum, Polygon, and Arbitrum to create a unified risk profile. Its federated learning model allows for continuous improvement of risk assessments without centralizing sensitive user data, aligning with current regulatory expectations for data minimization.

Regulatory Risks and Compliance

The intersection of on-chain history and traditional financial regulation creates a complex liability landscape for DeFi protocols. Unlike centralized lenders, decentralized finance operates across jurisdictions, yet it remains subject to the same stringent rules regarding data privacy and consumer protection. The primary legal ambiguity centers on whether an algorithmic credit score constitutes a regulated "credit report" or a "security," a distinction that determines compliance obligations for protocol developers.

Data privacy laws, including the General Data Protection Regulation (GDPR) in Europe and the California Consumer Privacy Act (CCPA) in the United States, pose significant hurdles for immutable on-chain data. Credit scoring relies heavily on analyzing transaction histories to assess risk, but the "right to be forgotten" under GDPR conflicts with the permanent nature of blockchain ledgers. Protocols must navigate this tension by ensuring that personal identifiers are kept off-chain while only cryptographic proofs of creditworthiness are stored on-chain.

Academic literature also highlights concerns regarding "predatory lending" mechanisms inherent in DeFi. Without the underwriting discretion of traditional banks, algorithmic scoring can lead to aggressive liquidation practices that disproportionately affect borrowers during market volatility. Research from the Global Association of Risk Professionals (GARP) indicates that while credit scores can minimize counterparty risk, they must be designed with safeguards to prevent systemic instability and unfair lending practices.

The Crypto-Native Credit Score framework, as discussed in academic journals, aims to bridge the gap in risk assessment while adhering to regulatory standards. By rendering DeFi lending more robust and inclusive, these systems attempt to align on-chain behavior with off-chain legal expectations. However, the lack of a unified global regulatory framework means that protocols face varying compliance burdens depending on their user base, making legal adherence a dynamic and high-stakes challenge.

| Factor | Compliance Impact |

|---|---|

| Immutable Data | Conflicts with GDPR right to erasure |

| Algorithmic Scoring | May be classified as a credit report |

| Cross-Border Access | Subject to multiple jurisdictional laws |

No comments yet. Be the first to share your thoughts!