DeFi lending reshapes credit assessment

The traditional credit score, anchored in FICO and historical banking data, is losing its monopoly on risk assessment. In 2026, DeFi lending has emerged as the primary driver of a new paradigm: the crypto credit score. Unlike conventional loans that rely on income verification and credit history, DeFi protocols utilize on-chain reputation and collateralization ratios to determine borrowing power. This shift removes traditional barriers such as lengthy approval processes and rigid credit checks, replacing them with transparent, algorithmic risk models.

This transition does not merely change how loans are approved; it fundamentally alters the definition of creditworthiness. A borrower’s ability to repay is no longer inferred from past behavior in a centralized bank but is verified through real-time on-chain activity. As noted in legal analyses from Cardozo Law, crypto-native credit scoring aims to bridge the gap in risk assessment, rendering DeFi lending more robust and inclusive for those excluded from traditional systems. However, this inclusivity comes with high-stakes implications, as the lack of regulatory oversight in many jurisdictions means that on-chain reputation is often the only recourse for lenders in the event of default.

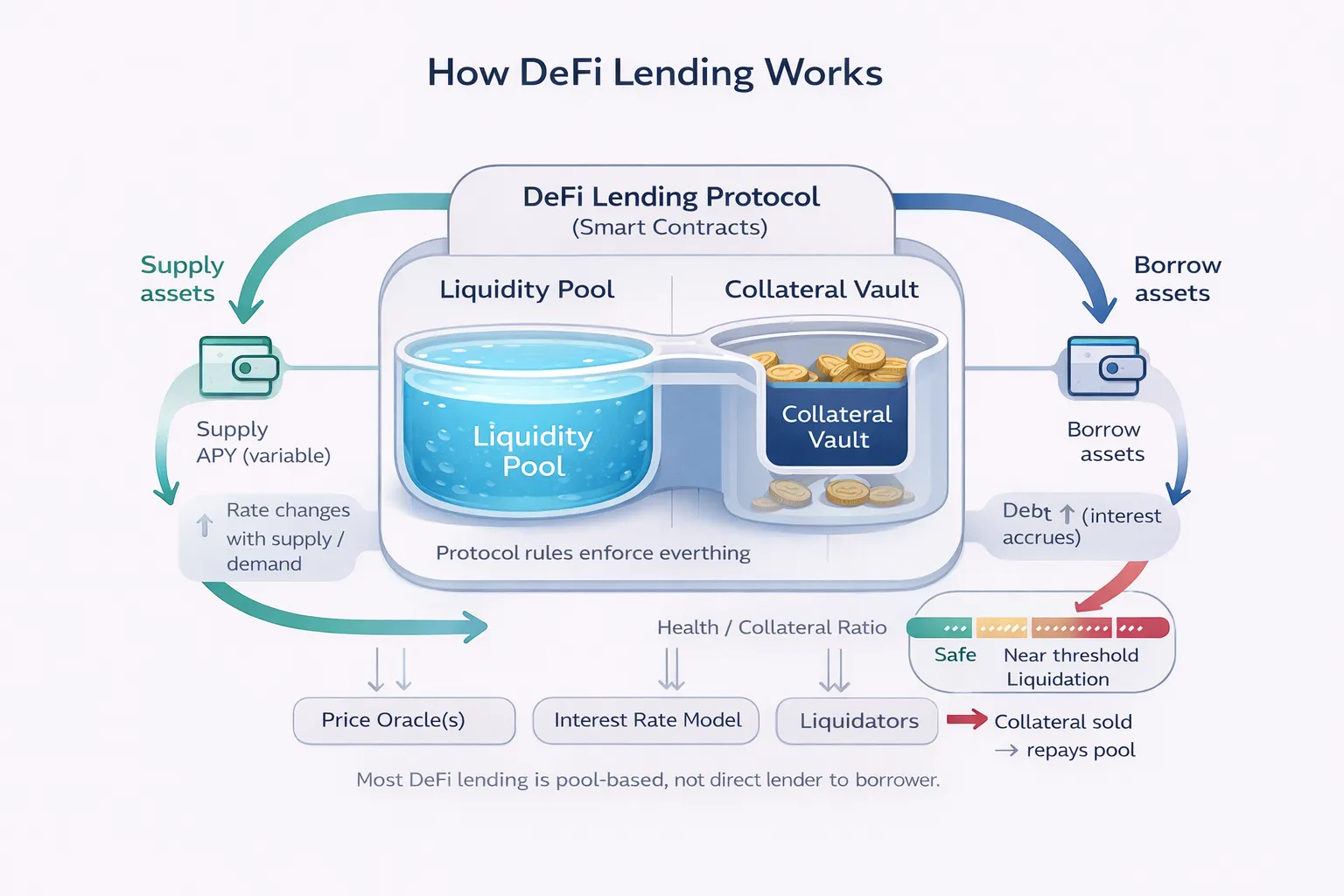

The market for crypto-backed loans has expanded rapidly, with borrowing against Bitcoin becoming a standard liquidity tool. These loans are collateral-based rather than credit-based, meaning the asset itself serves as the primary guarantee. This structure decouples borrowing capacity from traditional credit scores, allowing users with thin or no credit files to access capital. Yet, the volatility of these assets introduces unique risks that traditional credit models were designed to mitigate through conservative underwriting. The interplay between asset price and loan-to-value ratios creates a dynamic where credit health is constantly recalculated by smart contracts.

To understand the current state of this market, it is necessary to look at the underlying asset performance that drives these lending protocols. The value of the collateral, primarily Bitcoin, directly influences the stability of the lending ecosystem.

The shift toward on-chain reputation is not just a technological upgrade; it is a regulatory challenge. As digital assets become more integrated into the broader financial system, the question of how on-chain data translates to legal creditworthiness remains unresolved. The PwC Global Crypto Regulation Report 2026 highlights that while stablecoins and tokenization are key areas of focus, the supervisory frameworks for crypto-native credit scoring are still in their infancy. This regulatory uncertainty adds a layer of complexity for users who may find their on-chain reputation valuable in DeFi but unrecognized by traditional financial institutions.

On-chain history replaces FICO

The traditional FICO model relies on a narrow set of financial behaviors: payment history, amounts owed, length of credit history, new credit, and credit mix. DeFi lending operates on a different axis entirely. In 2026, your "credit score" is not a three-digit number pulled from a centralized bureau, but a dynamic, on-chain reputation derived from your wallet's transaction history, repayment behavior, and asset holdings.

This shift is not merely cosmetic; it is structural. DeFi protocols do not report to Equifax or TransUnion. Instead, they aggregate data directly from the blockchain. Every swap, liquidity provision event, and loan repayment is permanently recorded. This creates a comprehensive, immutable ledger of your financial activity. For borrowers, this means that your ability to secure loans is determined by your on-chain solvency rather than your off-chain creditworthiness.

The implications for legal compliance and risk management are significant. Because this data is public, it can be analyzed by third-party scoring algorithms to generate a "crypto-native" credit score. These scores evaluate factors such as collateralization ratios, transaction frequency, and wallet age. A wallet with a long history of consistent repayments and stable asset holdings will command better lending terms than a new wallet with high volatility.

This system is more transparent but also more exposed. Your entire financial history is visible to anyone who knows your address. While this reduces information asymmetry for lenders, it increases the risk of doxxing and targeted attacks. Understanding this on-chain reputation is critical for anyone engaging in high-stakes DeFi lending.

Collateral Models and Risk Metrics

DeFi lending protocols operate on a fundamentally different risk architecture than traditional finance. Instead of relying on personal credit history, these systems use over-collateralization to mitigate default risk. Borrowers must lock up digital assets worth more than the loan amount, creating a buffer that protects lenders if the collateral’s value drops. This mechanism removes traditional barriers such as credit scores, allowing anyone with sufficient crypto holdings to access liquidity regardless of their off-chain financial history.

The primary metric governing this relationship is the Loan-to-Value (LTV) ratio. An LTV of 50% means a borrower can borrow $50 for every $100 of collateral deposited. If the value of the collateral falls below a specified threshold, the protocol automatically liquidates the assets to repay the loan. This automated enforcement is critical in high-volatility markets, where rapid price swings can erode collateral value in minutes. Unlike CeFi loans, which may offer grace periods or manual review processes, DeFi liquidations are instantaneous and algorithmic.

| Feature | CeFi Lending | DeFi Lending |

|---|---|---|

| Credit Check | Required (FICO/Income) | None (On-chain only) |

| Collateral | Often Unsecured | Over-collateralized |

| LTV Ratio | Typically 20-30% | Typically 50-75% |

| Liquidation | Manual/Legal Process | Automated/Instant |

| Transparency | Private/Black Box | Public/On-chain |

While DeFi removes the need for a credit score, it introduces new risks tied to smart contract code and oracle reliability. A failure in the price feed or the liquidation engine can lead to significant losses for borrowers or lenders. Therefore, understanding the specific collateral models and risk metrics of each protocol is essential for managing exposure in the DeFi lending landscape.

| Feature | CeFi Lending | DeFi Lending |

|---|---|---|

| Credit Check | Required (FICO/Income) | None (On-chain only) |

| Collateral | Often Unsecured | Over-collateralized |

| LTV Ratio | Typically 20-30% | Typically 50-75% |

| Liquidation | Manual/Legal Process | Automated/Instant |

| Transparency | Private/Black Box | Public/On-chain |

2026 Regulatory Shifts

The regulatory landscape for digital assets is undergoing a fundamental restructuring in 2026, moving from experimental frameworks to standardized compliance. PwC’s 2026 Global Crypto Regulation Report highlights that the focus has shifted decisively toward stablecoin issuance models, reserve requirements, and supervisory frameworks across more than 50 jurisdictions. This standardization is not merely bureaucratic; it is the primary mechanism integrating DeFi lending into traditional credit ecosystems.

A critical development in this shift is the integration of traditional credit bureaus into blockchain protocols. As reported by TransUnion, credit agencies are now delivering traditional off-chain credit scores to individuals applying for loans on blockchain-based protocols. This allows lenders to assess risk using familiar metrics without compromising the privacy or security of on-chain data. The result is a hybrid credit scoring model where DeFi lending activity directly influences a user’s traditional creditworthiness.

This convergence creates a high-stakes environment where regulatory compliance becomes a prerequisite for market access. Grayscale’s 2026 Digital Asset Outlook notes that the "dawn of the institutional era" is defined by this interoperability between legacy finance and decentralized protocols. For lenders, this means that failure to adhere to emerging regulatory standards could result in exclusion from the broader credit market, while early adopters benefit from expanded liquidity and trust.

Building your on-chain reputation

Your crypto credit score is not a static number; it is a dynamic record of how you manage smart contract liabilities. In 2026, lenders rely on this on-chain history to assess risk, making responsible borrowing habits essential for accessing capital. Building this reputation requires treating DeFi protocols like regulated financial institutions: consistency and transparency are paramount.

Keep your Loan-to-Value (LTV) ratio well below the liquidation threshold. While protocols may allow borrowing up to 80% of your collateral, maintaining an LTV under 50% demonstrates financial stability. This buffer protects you from market volatility and signals to lenders that you prioritize risk management over leverage.

Repayment history is the strongest predictor of future creditworthiness. Set up automated repayments or calendar reminders to ensure your principal and interest are settled on time. Even a single missed payment can severely damage your on-chain reputation, making future borrowing more expensive or impossible.

Engage with multiple reputable protocols rather than concentrating all your activity on a single platform. A diverse history of successful interactions across different DeFi ecosystems shows lenders that you are experienced and adaptable. This diversification also reduces the risk of a single protocol failure impacting your entire credit profile.

Lenders may blacklist addresses associated with known bad actors or high-risk activities. Avoid interacting with protocols flagged for security breaches or those involved in illicit activities. A clean transaction history ensures that your credit score reflects only your legitimate financial behavior, not the actions of others.

The concept of a "crypto-native credit score" aims to bridge the gap in risk assessment, rendering DeFi lending more robust and inclusive. As noted by legal experts at Cardozo Law, these scores are evolving beyond simple wallet reputation to include complex behavioral data. Your on-chain identity is becoming your financial passport, so treat it with the same care as your traditional credit report.

Frequently asked: what to check next

Does DeFi lending affect my traditional credit score?

Generally, no. DeFi lending protocols are collateral-based rather than credit-based. This structure removes traditional barriers such as FICO scores and lengthy approval processes, meaning your on-chain borrowing activity typically does not report to major credit bureaus. However, this also means you miss the opportunity to build traditional credit history through on-chain activity. For a broader view of how these systems are evolving, the 2026 Crypto Market Outlook from Coinbase highlights the regulatory progress shaping these boundaries.

What regulatory changes should I expect in 2026?

The PwC Global Crypto Regulation Report 2026 indicates a shift toward stricter oversight of stablecoins, including reserve and redemption requirements. As digital assets face more scrutiny, the line between traditional finance and DeFi may blur, potentially leading to new reporting requirements that could eventually impact how on-chain activity is viewed by traditional credit agencies.

How volatile is Bitcoin, and how does it impact loans?

Bitcoin’s price volatility is the primary risk in collateralized lending. If the value of your Bitcoin collateral drops significantly, you may face liquidation. The current market trajectory can be tracked via the Bitcoin price widget or technical charts to gauge short-term trends. Understanding these fluctuations is essential for managing loan-to-value ratios and avoiding forced sales during market dips.

What are the biggest developments for digital assets in 2026?

Beyond regulation, experts point to digital securities, tokenisation, and interoperability as key areas of development. Ashurst’s 2026 outlook suggests that while regulation is pervasive, the integration of digital assets into traditional cash legs remains a significant challenge for widespread adoption.

No comments yet. Be the first to share your thoughts!