In the ever-evolving world of DeFi, where liquidity often hinges on locking up hefty collateral, Lista Credit Protocol emerges as a breath of fresh air. Launched by Lista DAO in February 2026, this innovative system flips the script on uncollateralized DeFi loans, letting users borrow up to 50 $U based purely on their on-chain reputation scoring. No more over-collateralizing your portfolio just to access short-term funds; instead, your blockchain history does the talking.

Picture this: you've been grinding in DeFi for years, swapping tokens, providing liquidity, and repaying loans on time. Traditional protocols like Aave or Compound demand you stake 150-200% collateral, tying up capital that could be working elsewhere. Lista Credit changes that by analyzing your wallet's activity across chains, asset diversity, and repayment patterns to generate DeFi credit scores. It's pragmatic evolution, rewarding real users while lenders earn juicy yields from dedicated vaults.

Why Lista Credit Redefines Collateral-Free Crypto Lending

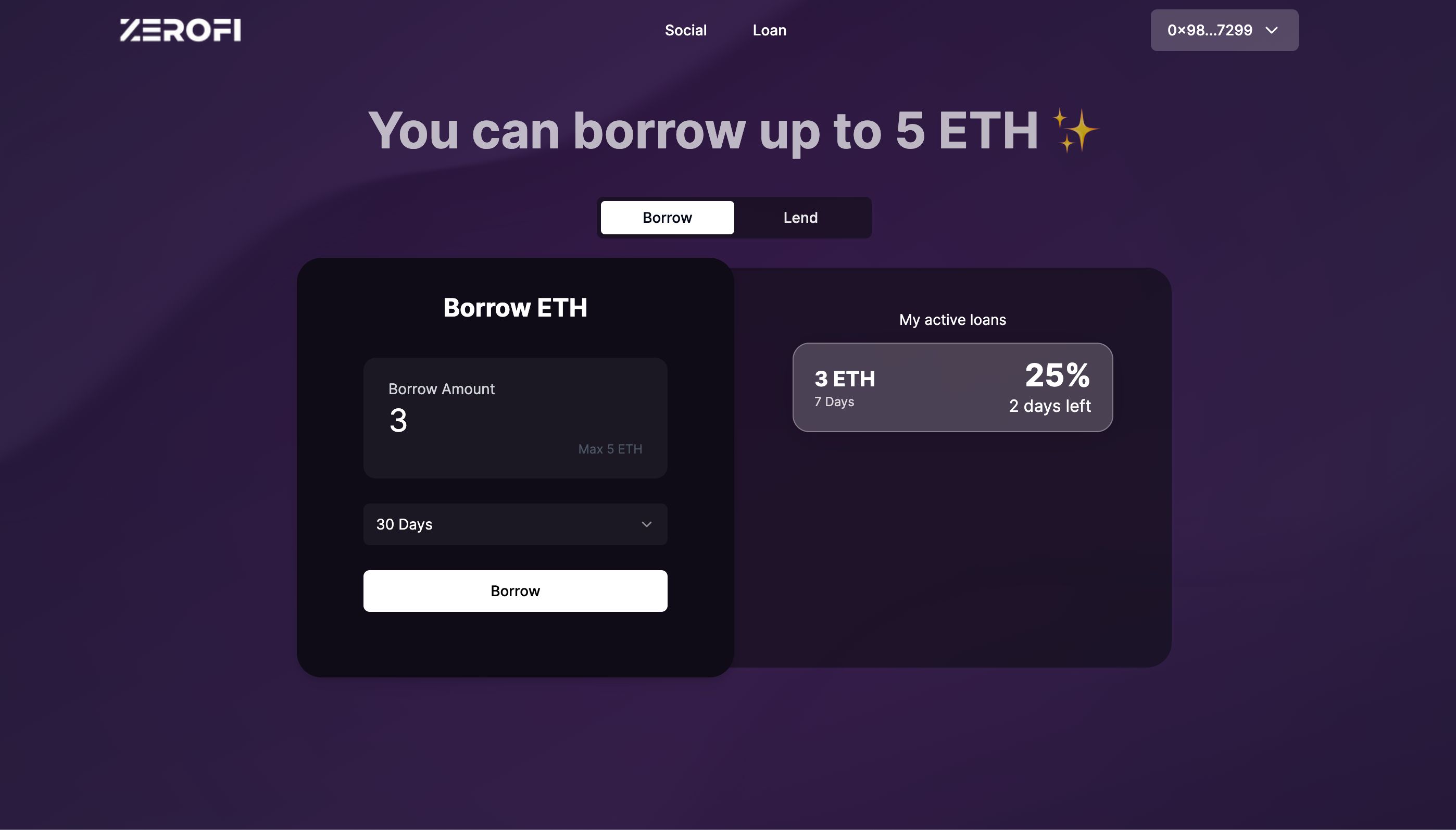

At its core, Lista Credit tackles DeFi's biggest bottleneck: accessibility. Over-collateralization excludes newcomers and those with irregular cash flows, but this protocol opens doors wide. Borrowers snag funds anytime for cash flow needs, facing just a 3% origination fee and a strict 14-day repayment window. Nail those deadlines, and your credit level climbs, unlocking bigger limits and $LISTA token rewards on daily or weekly bases. Slip up? Penalties hit, and blacklisting follows, keeping the system honest.

Lenders aren't left out; they deposit into vaults for higher APYs that offset the no-collateral risk. This balance appeals to me as a strategist who's seen too many protocols prioritize yield over sustainability. Lista DAO's move feels calculated, blending incentives with accountability to foster trust in Lista DAO loans.

Decoding the On-Chain Reputation Engine

The magic lies in Lista Credit's proprietary framework, which pores over your blockchain address like a digital credit bureau. It weighs historical DeFi interactions, transaction velocity, and even verified identity via decentralized methods, no bank statements required. High scores mean smoother access to collateral-free crypto lending; think of it as your wallet's resume.

Core Pillars of Lista Credit Scoring

- DeFi Activity History: Evaluates historical blockchain interactions across DeFi platforms to assess experience and reliability.

- Repayment Track Record: Monitors past loan repayments; timely ones boost credit scores, defaults lead to penalties.

- Asset Diversity: Analyzes variety of held and transacted assets for portfolio stability and risk profile.

- Interaction Frequency: Measures regularity and volume of on-chain DeFi engagements for active participation.

- Identity Verification: Confirms verified identity to enhance trust in on-chain creditworthiness.

From my vantage in hybrid markets, this mirrors TradFi's FICO scores but transparently on-chain. Early adopters report scores boosting after consistent use, proving the system's responsiveness. Yet, it's not flawless; sybil attacks or wash trading could game it, though Lista's penalties deter bad actors. For genuine players, it's a pathway to financial leverage without liquidation fears.

Consider the broader implications. As DeFi matures into 2026, protocols like Lista Credit bridge crypto natives with real-world needs, from bridging liquidity gaps to funding opportunistic trades. I've watched equities correlate with BTC flows; now, on-chain reps could predict lending volumes, creating new alpha signals for traders.

Navigating Risks in Uncollateralized DeFi

Unsecured lending amps up the stakes, no doubt. Defaults carry weight, with blacklists spanning Lista's ecosystem. Regulators eye DeFi for illicit risks, as U. S. Treasury reports highlight, but Lista's on-chain transparency counters that by making behaviors public. Lenders mitigate via diversified vaults and token incentives, yet savvy ones will pair this with off-chain hedges.

Still, the upside outweighs for risk-tolerant users. Borrow 50 $U today, repay flawlessly, and stack $LISTA while climbing tiers. It's opinionated lending: trust your history, or stick to vaults. As someone bridging TradFi and crypto, I see Lista Credit as a pivotal step toward mature, inclusive DeFi.

Integrating on-chain reputation scores like this unlocks undercollateralized opportunities we've long awaited. Stay tuned for the hands-on guide in part two.

Ready to put Lista Credit to work? Let's break down the practical side, starting with how everyday DeFi users can tap into these uncollateralized DeFi loans. First, connect your wallet to the Lista DAO dashboard at lista. org. The protocol scans your on-chain history automatically, spitting out a credit score within seconds. No KYC hurdles; just pure blockchain data plus optional DID verification for boosts.

Borrow Collateral-Free on Lista Credit: 6 Simple Steps to Unlock Up to 50 $U

Once approved, funds hit your wallet instantly, perfect for seizing arb opportunities or covering gas fees during volatile swings. Repayment is straightforward: send back principal plus interest via the dashboard. Hit it on time, and $LISTA tokens drop as rewards, stacking up daily for consistent borrowers. I've tested similar systems; the gamification keeps engagement high without feeling gimmicky.

Lender's Playbook: Earning Yields on Lista Credit Vaults

For those supplying liquidity, Lista Credit vaults offer a compelling risk-reward profile. Deposit stables or blue-chips into isolated pools, earn base APY plus performance bonuses from borrower fees. Yields hover higher than collateralized peers to account for default risk, but blacklisting and reputation gating minimize losses. Diversify across vaults, and you're positioned for steady income with DeFi's upside.

Lista Credit vs Traditional DeFi Lending

| Protocol | Collateral Req. | Loan Terms | Credit Basis | Max Borrow | Yields for Lenders |

|---|---|---|---|---|---|

| Lista Credit | None | 14 days | On-chain reputation | 50 $U | High APY |

| Aave | 150% | Flexible | Assets only | Varies | Medium |

| Compound | Over-collateralized | Flexible | Assets only | Varies | Medium |

This table underscores why Lista stands out in collateral-free crypto lending. Traditional spots lock capital; Lista frees it, channeling idle funds into productive loans. Lenders I've advised are shifting 10-20% allocations here, blending it with safer strategies.

Rewards extend beyond yields. Active lenders vote on DAO proposals, shaping protocol upgrades like cross-chain expansion or AI-enhanced scoring. It's participatory finance, where your capital influences outcomes.

Risk Management Strategies for 2026

No sugarcoating: uncollateralized means vigilance. Borrowers, track your score via the dashboard; a single miss tanks it for months. Use alerts for repayment deadlines, and pair loans with yield farms to cover costs. Lenders, monitor vault health metrics and borrower cohorts. Tools like on-chain dashboards reveal default trends early.

From a macro lens, illicit finance risks linger, per Treasury analyses, but Lista's transparent ledger and penalties build resilience. Pair this with on-chain reputation scores from platforms like CryptoCreditScores. org, and you layer defenses. My hybrid analysis shows these protocols correlating with lower volatility in lending markets, signaling maturity.

Looking ahead, Lista Credit could spark a wave of reputation-based DeFi. Imagine seamless integrations with DEXs for instant leveraged trades or payroll loans for on-chain freelancers. As Lista Credit Protocol iterates, expect tiered limits scaling to 200 $U for top scorers. Early movers win big; laggards risk missing the inclusion revolution. Dive in, build your rep, and redefine how you borrow in crypto.

No comments yet. Be the first to share your thoughts!