Check your on-chain history

Your wallet address is your social security number in DeFi. Every transaction, loan repayment, and stablecoin holding creates a permanent record that protocols use to assess your reliability. Before you can build a DeFi credit score, you need to audit the raw data that defines it. Think of your wallet as a financial resume that never forgets; if it’s blank or messy, lenders have nothing to work with.

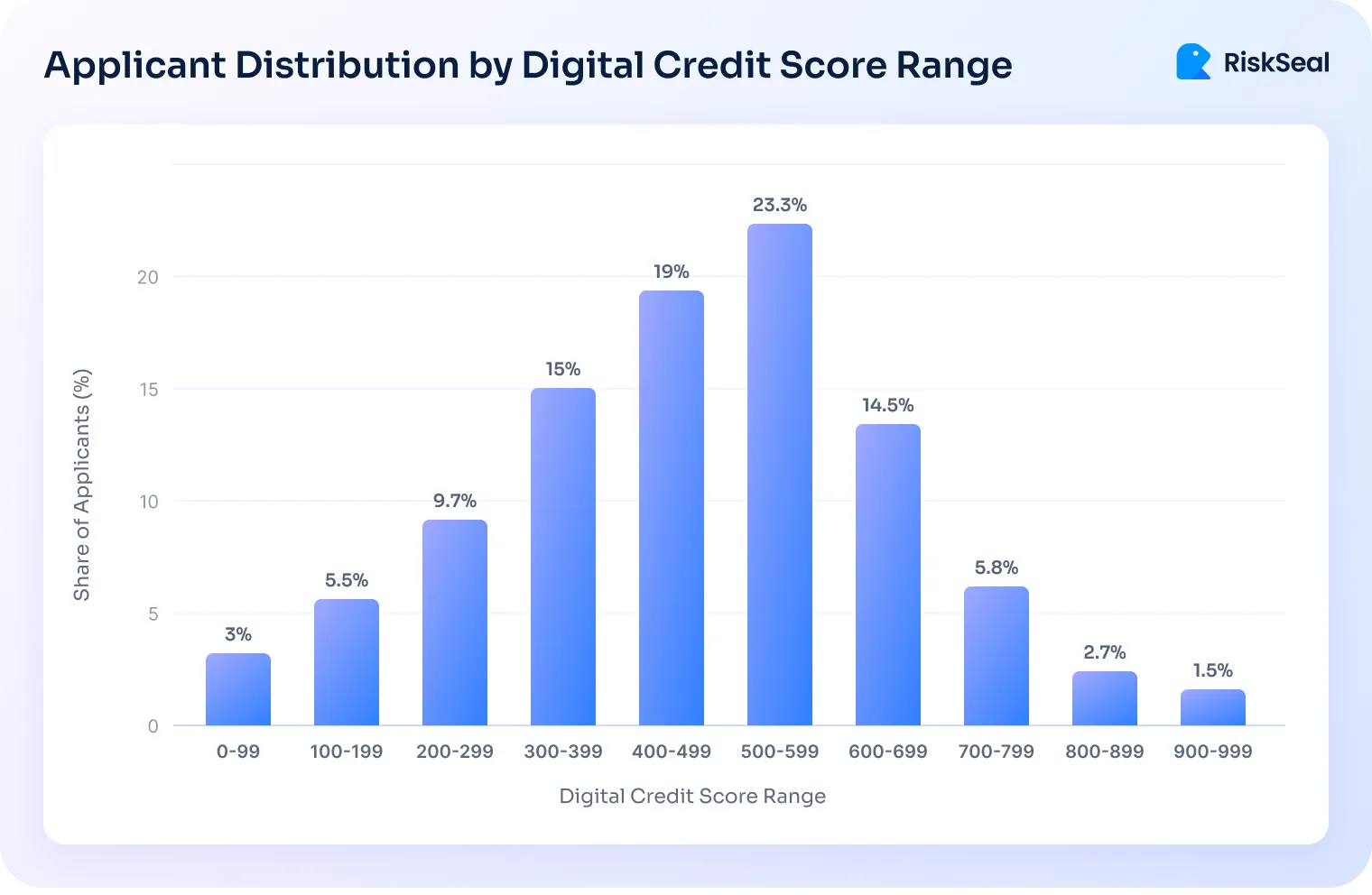

To start, connect your wallet to a reputable on-chain analytics platform like DeFiScore. These tools aggregate your activity across multiple chains, including Ethereum and Arbitrum, to generate a transparent credit report. The platform will display a score ranging from 300 to 850, along with portfolio risk heatmaps that highlight potential vulnerabilities in your current setup. This isn’t just a number; it’s a diagnostic tool showing exactly which behaviors are helping or hurting your standing.

Pay close attention to the details behind the score. Look for patterns such as consistent repayment history, diversified asset holdings, and the absence of suspicious or high-risk interactions. Protocols favor wallets that demonstrate stability over time. If your history shows frequent flash-loan arbitrage or interactions with flagged smart contracts, your score will reflect that risk. Use the free public API or dashboard alerts provided by these platforms to monitor changes in real-time, ensuring you stay ahead of any shifts in your on-chain reputation.

Compare lending protocols for credit reporting

Choosing the right lending protocol is the foundation of a verifiable DeFi credit score. Not all platforms report to external credit bureaus or use robust scoring models. You need a protocol that translates your on-chain activity into a format traditional lenders will actually recognize.

The market has consolidated around a few key players that prioritize data portability and standardization. Below is a comparison of the major DeFi credit score platforms in 2026, focusing on their reporting standards and scoring methodologies.

| Platform | Credit Bureau Reporting | Scoring Model | Data Granularity |

|---|---|---|---|

| ChainAware | Yes (Equifax, Experian) | Proprietary Risk Score | Full transaction history |

| Cred Protocol | Yes (TransUnion) | On-chain Behavior | Wallet activity |

| Spectral | Limited | Collateral-based | Loan-specific |

| Goldfinch | No | Community Vetting | Manual review |

ChainAware and Cred Protocol stand out for their direct integrations with major credit bureaus. This means your on-chain repayment history can directly influence your traditional FICO or VantageScore. Spectral, while robust, focuses more on collateralized lending with limited external reporting. Goldfinch relies on community vetting, which is valuable for privacy but less useful for building a portable credit profile.

When selecting a protocol, prioritize those that offer granular data export. A score based on full transaction history is far more accurate than one based solely on loan repayment. Look for platforms that allow you to verify your identity through KYC-lite processes, as this unlocks higher reporting tiers.

Lend and repay on time

Building a DeFi credit score is less about how much you borrow and more about how you pay it back. On-chain protocols do not rely on traditional bureau reports; they track your wallet’s history of fulfilling debt obligations. A clean repayment record acts as your financial fingerprint, signaling to lenders that you are a low-risk borrower ready for better terms.

Take out a loan

Start by borrowing a manageable amount on a reputable lending protocol such as Aave or Compound. The goal here is not to maximize leverage but to establish a clear debt record. When you take out the loan, the protocol locks your collateral and issues the debt position to your wallet address. This initial action creates the "credit line" that future scoring algorithms will monitor. Keep the loan size small relative to your collateral to avoid unnecessary liquidation risks while you are still building your history.

Repay on schedule

Consistency is the primary driver of your score. Set up automated reminders or use protocol dashboards to track your repayment dates. When you repay the loan principal and interest before the due date, the transaction is recorded on the blockchain. These successful repayments are aggregated by scoring models, such as the On-Chain Credit Risk Score (OCCR), to calculate a positive probability of future repayment. Each on-time payment increments your score, demonstrating reliability to the network.

Avoid defaults and liquidations

A single default or liquidation can severely damage your DeFi credit score. Unlike traditional credit, where a late payment might sit quietly on a report for years, on-chain defaults are immutable. If your collateral value drops below the required threshold and you fail to add more funds, the protocol liquidates your assets. This event is permanently visible on-chain and signals high risk to any future lender. To protect your score, maintain a healthy collateralization ratio and monitor market volatility closely.

Monitor your on-chain history

Regularly review your wallet’s transaction history to ensure all repayments are correctly logged. Some third-party analytics platforms now offer DeFi credit score dashboards that aggregate your lending activity. By keeping your profile clean and your repayments timely, you create a robust on-chain identity that can unlock higher borrowing limits and lower interest rates in the future.

Avoid common scoring mistakes

Your on-chain history is a permanent record. Unlike traditional credit reports, you cannot dispute a bad transaction or ask a lender to forget a default. The protocols that build your DeFi credit score are unforgiving: they only see the raw data of your past activity. One misstep can permanently lower your borrowing power or increase the cost of future loans.

Over-leveraging and liquidation risk

The fastest way to tank your score is to borrow against collateral you cannot afford to lose. High leverage ratios amplify volatility. When the market dips, your position may be liquidated, triggering a default record on your profile. Galaxy Research notes that crypto-collateralized lending volumes dropped significantly in early 2026 as exploits and market shocks exposed these risks [[src-serp-1]].

Keep your loan-to-value (LTV) ratio conservative. A healthy LTV leaves room for price swings without triggering automatic liquidations. This stability signals to scoring algorithms that you are a low-risk borrower, protecting your score from sudden drops.

Using unverified protocols

Not all DeFi platforms contribute to your credit score. Many protocols operate in isolation, and their lending activity remains invisible to major credit scoring models. If you lend or borrow on a platform that does not report to a recognized oracle or scoring provider, that activity will not help you build a reputation.

Stick to protocols that integrate with established credit reporting systems. Verify that the platform you are using is listed as a data source for the scoring model you are trying to improve. Activity on unverified chains or obscure forks often counts for nothing in the broader DeFi credit ecosystem.

Ignoring stablecoin volatility

Using volatile assets as primary collateral or repayment sources introduces unnecessary risk. Even if you do not get liquidated, frequent rebalancing and transaction fees can clutter your history with noise, making it harder for algorithms to assess your true repayment reliability. Choose stablecoins for your primary lending and borrowing activities to demonstrate consistent, predictable cash flow.

Verify your score with a provider

Before applying for any DeFi loan, you need an official score from a recognized provider. This step turns your on-chain activity into a verifiable credential that lenders actually accept.

- Choose a reputable provider. Look for platforms that offer a public API and transparent scoring models. DeFi Scoring is one option, offering scores between 300 and 850 across major chains like Ethereum and Arbitrum (deificscoring.com).

- Connect your wallet. Link the wallet you intend to use for borrowing. Ensure it holds the transaction history you want to highlight.

- Review the breakdown. Check which on-chain behaviors contributed to your score. Lenders often look for consistent repayment history and low portfolio risk.

Once verified, you can share your score or API token directly with lending protocols. This reduces friction and proves your creditworthiness without exposing unnecessary private data.

-

Score is issued by a recognized provider

-

Wallet connected matches borrowing intent

-

On-chain history covers the required period

Frequently asked: what to check next

Work through How DeFi Lending Impacts Your Credit Score

No comments yet. Be the first to share your thoughts!