Defi credit scoring limits to account for

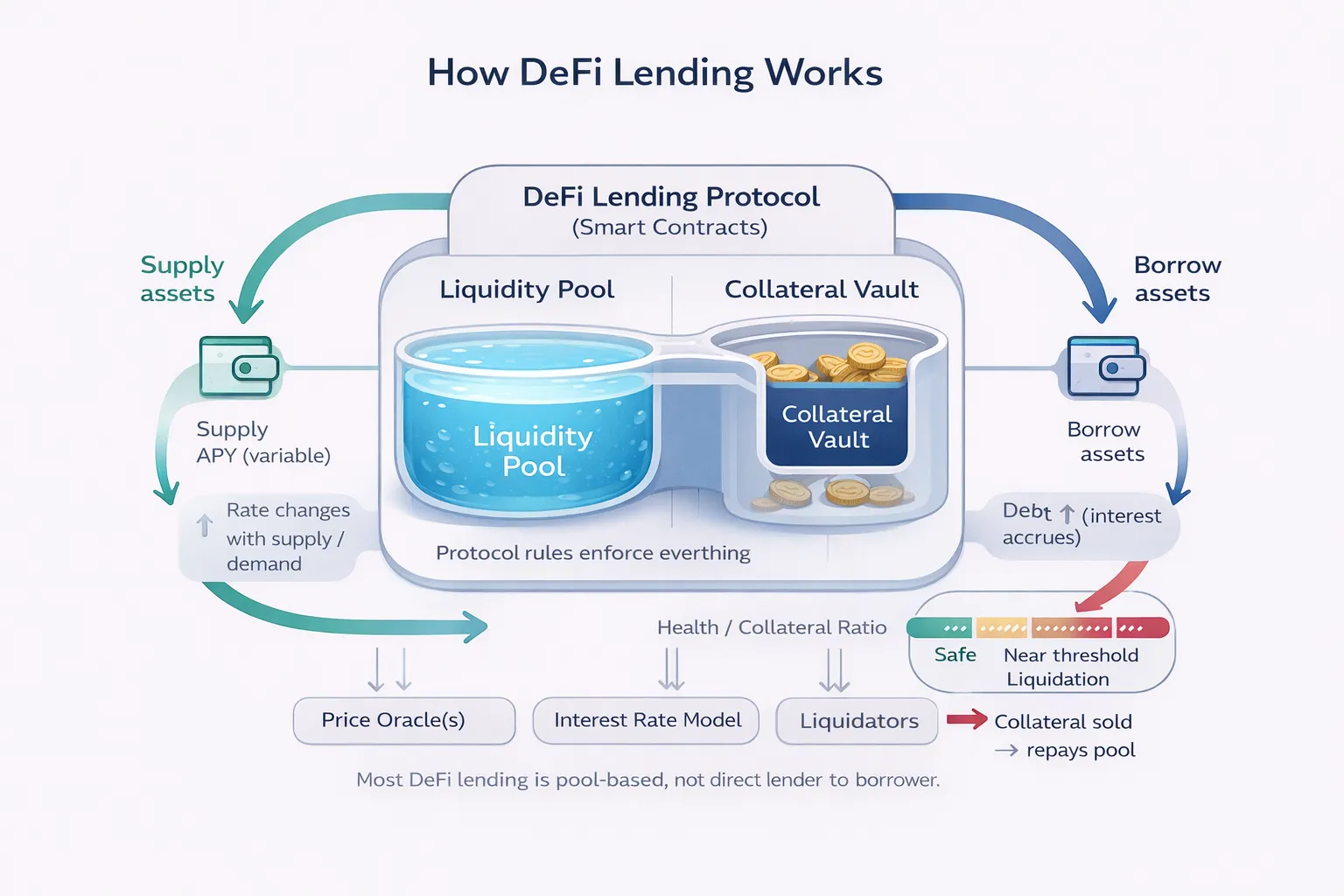

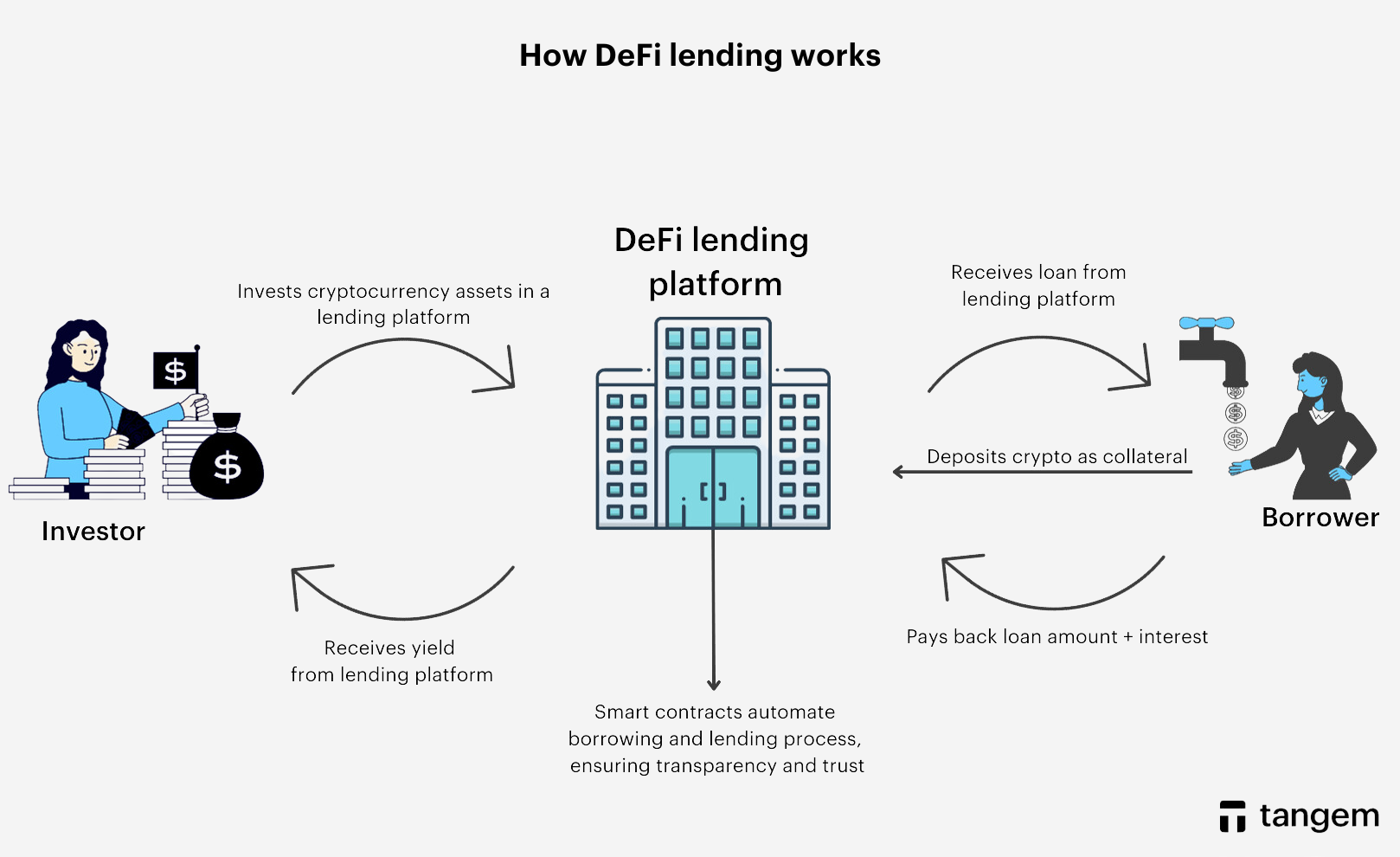

DeFi lending operates on collateral rather than identity. Traditional credit bureaus do not report on-chain activity, so your DeFi borrowing history does not automatically influence your FICO score. This creates a fundamental constraint: you can build a reputation for repayment on-chain without gaining access to centralized credit products.

A "DeFi credit" refers to the on-chain reputation built through consistent lending and borrowing behavior. Platforms like Kava are experimenting with AI-powered models to translate this on-chain data into a credit score. However, these scores remain siloed within specific ecosystems and are not yet recognized by major traditional lenders.

The primary tradeoff is accessibility versus privacy. You retain full control over your data, but you lose the automatic credit-building benefits of traditional finance. If you rely on your credit score for mortgages or auto loans, DeFi activity will likely remain invisible to those underwriters.

| Feature | Traditional Lending | DeFi Lending |

|---|---|---|

| Credit Check | Hard pull on bureau report | On-chain wallet analysis |

| Reporting | Reports to Equifax, Experian | No standard bureau reporting |

| Collateral | Unsecured or secured by income | Over-collateralized (crypto assets) |

| Privacy | Low (identity verification required) | High (pseudonymous) |

For most users, DeFi is a parallel financial track. It offers liquidity without identity checks, but it does not currently serve as a bridge to improve your traditional credit standing. Until standardized reporting protocols are adopted by major credit bureaus, these two worlds will remain separate.

Defi credit scoring choices that change the plan

DeFi lending relies on algorithmic models that assess creditworthiness without traditional bureau checks. These models analyze on-chain behavior, collateral health, and transaction history to generate a score. While this expands access to capital, it introduces distinct risks compared to conventional credit reporting.

When evaluating DeFi credit scoring, you must weigh transparency against volatility. Traditional scores are stable but opaque; DeFi scores are transparent but highly sensitive to market swings. Understanding these mechanics helps you determine if a platform aligns with your long-term financial goals.

The table below compares key factors across different DeFi credit scoring approaches. This comparison highlights how collateral type, data sources, and reporting mechanisms differ in impact on your financial profile.

| Factor | On-Chain Only | Hybrid Model | Traditional Bridge |

|---|---|---|---|

| Data Source | Wallet history, tx volume | On-chain + KYC data | Credit bureau reports |

| Volatility Impact | High (collateral dependent) | Moderate | Low (stable metric) |

| Privacy Level | Public (pseudonymous) | Private (verified identity) | Restricted (bureau access) |

| Reporting to Bureaus | None | Selective/Partner-based | Standard full reporting |

| Default Risk | Liquidation risk | Underwriting risk | Payment history risk |

The choice between these models depends on your priority. If privacy and speed are paramount, on-chain models offer immediate access. However, they do not build traditional credit history. Hybrid models offer a middle ground, potentially reporting positive payment history to bureaus while maintaining some blockchain transparency.

Always verify if a platform reports to major credit bureaus before borrowing. Without this reporting, your responsible DeFi usage will not improve your traditional credit score. Conversely, failure to maintain collateral ratios can trigger liquidations, which may indirectly affect your financial standing through debt collection or legal action.

How to Decide if DeFi Lending Fits Your Credit Profile

DeFi lending impacts your credit score differently depending on whether the protocol reports to bureaus and how you structure your collateral. The 2026 reporting standards prioritize transparency, but they don't automatically translate to a higher FICO score for every borrower.

Use this framework to determine if the tradeoff between lower fees and credit invisibility is worth it for your current financial goals.

Most DeFi platforms operate in a regulatory gray area and do not report positive payment history to Equifax, Experian, or TransUnion. Before borrowing, verify if the protocol integrates with a third-party reporting service like Plaid or Chainalysis. If the platform doesn't explicitly state it reports to bureaus, assume the activity will not help your score.

Traditional loans report late payments as negative marks. DeFi loans are overcollateralized; if your crypto drops in value, the protocol liquidates your assets rather than reporting a delinquency. This protects your credit score from sudden drops but carries the risk of losing your principal. Calculate your liquidation threshold carefully.

Traditional lenders charge origination fees and interest based on your credit tier. DeFi protocols charge network gas fees and a percentage of the borrowed amount. For short-term borrowing under 30 days, DeFi is often cheaper. For long-term leverage, the compounding interest on DeFi loans can exceed traditional personal loan rates if you don't monitor APY changes.

New 2026 standards require clearer disclosure of how AI-driven credit scoring models interpret on-chain data. If you plan to apply for a mortgage within two years, be cautious. Some lenders view recent DeFi activity as "thin file" risk, which can complicate underwriting even if your on-chain history is flawless.

Spotting misleading claims and weak options

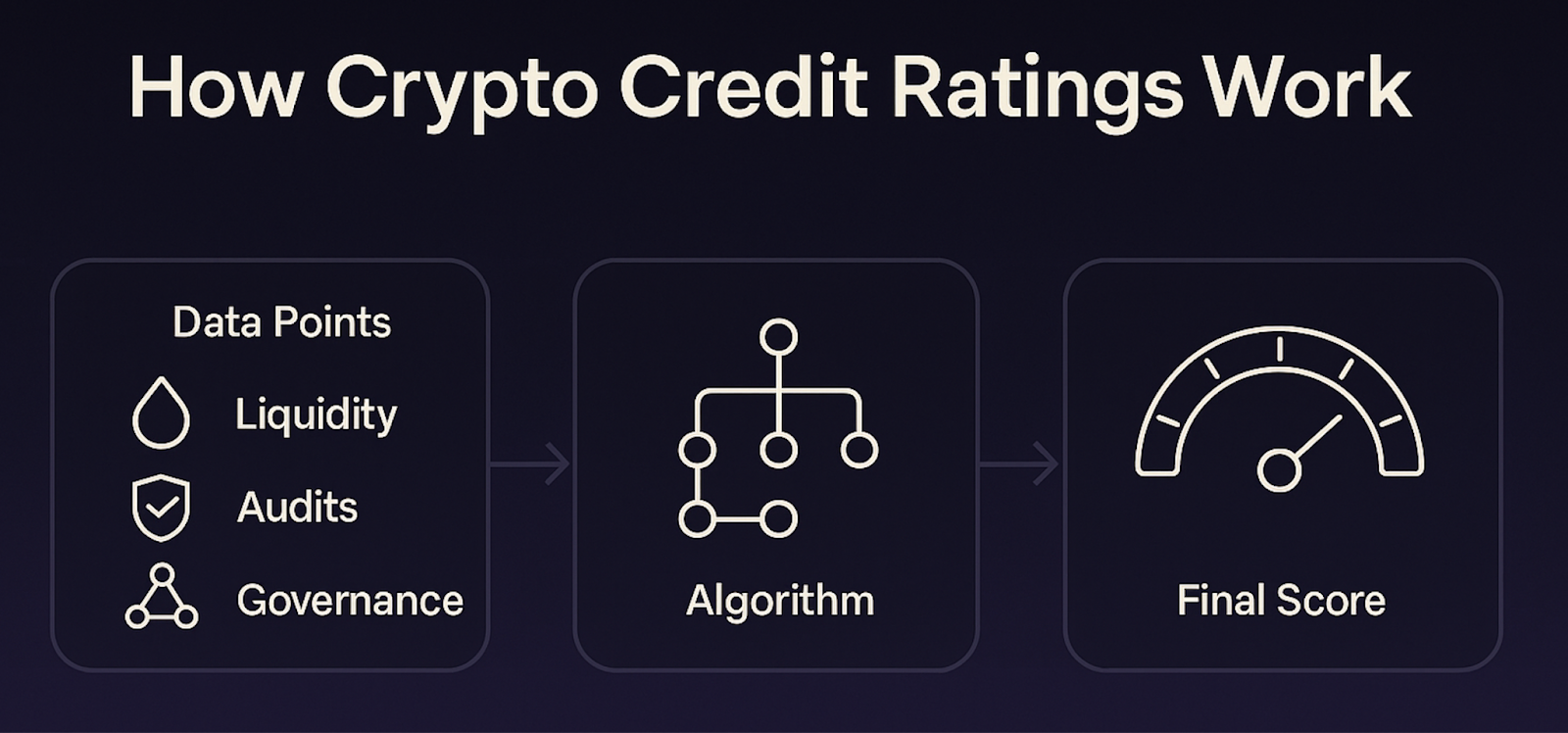

New reporting standards make it easier to separate real DeFi credit data from marketing fluff. Many platforms still claim to "boost" scores without disclosing how their models weight on-chain activity versus traditional bureau data. A DeFi credit score is not a single number; it is a composite of wallet history, collateral health, and repayment behavior. Treat it as a signal, not a guarantee.

Watch for vague metrics like "AI-powered scoring" without explaining the data sources. If a platform does not list which chains or protocols it analyzes, the score is likely based on limited or biased data. Similarly, claims of "instant approval" often hide high fees or risky collateral requirements that can trigger liquidations.

The biggest mistake borrowers make is assuming DeFi lending is anonymous. While transactions are pseudonymous, the data is public. Lenders can trace your history across multiple wallets. If you have a history of defaults or high leverage, that pattern will follow you. Transparency is a feature, but it also means past mistakes are harder to erase.

Focus on platforms that publish their scoring methodology. Look for clear definitions of what constitutes a "good" score and how collateral volatility is factored in. Avoid services that promise score improvements through simple transactions without explaining the underlying risk model.

Defi credit scoring: what to check next

Understanding how decentralized finance interacts with traditional credit systems requires separating the technology from the reporting standards. Below are the most common practical questions regarding DeFi credit scoring and its impact on your financial history.

No comments yet. Be the first to share your thoughts!