On-chain reputation replaces FICO

The foundation of crypto credit is shifting from traditional bureau scores to on-chain wallet behavior. In traditional finance, creditworthiness is determined by debt history and income verification. In decentralized finance, it is determined by asset behavior, collateralization ratios, and repayment consistency.

On-chain credit is more likely to start as wallet reputation. It will probably emerge, just not in the TradFi FICO form people imagine. The first systems will likely rely on transparent ledger data rather than opaque scoring algorithms.

Institutions now augment traditional inputs with on-chain data, such as wallet balances and flows, reserve composition, and transaction behavior. This data provides a real-time view of counterparty and asset risk that static bureau scores cannot match.

To understand the collateral backing these new credit models, we must look at the current market value of the primary assets used: Bitcoin and Ethereum.

How CeFi Lending Bridges TradFi and Crypto

Centralized finance (CeFi) platforms are redefining crypto lending by merging traditional credit infrastructure with blockchain collateral. Unlike pure DeFi protocols that rely solely on over-collateralization, CeFi lenders now integrate with major credit bureaus like TransUnion to assess borrower risk [src-serp-2]. This hybrid model allows platforms to offer unsecured or lower-collateral loans based on a borrower’s off-chain credit history, effectively bridging the gap between traditional banking standards and digital asset liquidity.

The structural difference is significant. In DeFi, your credit score is irrelevant; your loan-to-value (LTV) ratio is determined by algorithmic smart contracts. In CeFi, the platform performs a soft or hard credit pull alongside the collateral lock. This means a borrower with strong traditional credit may secure better rates or lower collateral requirements, while those with poor credit face higher spreads or rejection, regardless of their crypto holdings.

To understand the current value dynamics of these collateralized loans, it is essential to track real-time asset prices. The following widget displays live market data for Bitcoin and Ethereum, the primary collateral assets in these CeFi lending pools.

The following table compares the structural mechanics of CeFi hybrid lending against traditional DeFi models.

| Feature | CeFi (Hybrid) | DeFi (Pure) |

|---|---|---|

| Credit Check | Yes (TransUnion/Experian) | No |

| Collateral Type | Crypto + Credit History | Crypto Only |

| Approval Speed | Hours to Days | Minutes |

| Privacy | Low (KYC Required) | High (Pseudonymous) |

| Loan Types | Secured & Unsecured | Over-collateralized Only |

This integration creates a more familiar borrowing experience for traditional investors but introduces counterparty risk. Users must trust the centralized entity to manage both their crypto assets and their personal financial data securely. As the market evolves, the line between these models continues to blur, with some DeFi protocols beginning to explore privacy-preserving credit scoring mechanisms.

How DeFi Uses Collateral Ratios

Decentralized finance protocols operate on a fundamentally different credit model than traditional banking. Instead of relying on personal credit history, income verification, or identity checks, DeFi lending platforms determine loan terms based entirely on Loan-to-Value (LTV) ratios. This structure removes traditional barriers such as credit scores and lengthy approval processes, allowing anyone with crypto assets to borrow against them instantly.

The core mechanic is simple: you lock up collateral, and the protocol issues a loan based on a percentage of that collateral's value. For example, if a protocol sets a 50% LTV limit, you must deposit $10,000 worth of Bitcoin to borrow $5,000. This over-collateralization acts as the primary risk mitigation tool. If the value of your Bitcoin drops, the loan-to-value ratio rises. If it crosses a predefined threshold, the protocol automatically liquidates your collateral to repay the lender, ensuring the system remains solvent without human intervention.

This model shifts the risk profile significantly. In traditional finance, a bad credit score might disqualify you entirely. In DeFi, the only disqualification is insufficient collateral. However, this comes with the risk of volatility. Because crypto assets can swing wildly in price, the "credit score" is dynamic and tied directly to market performance rather than personal reliability.

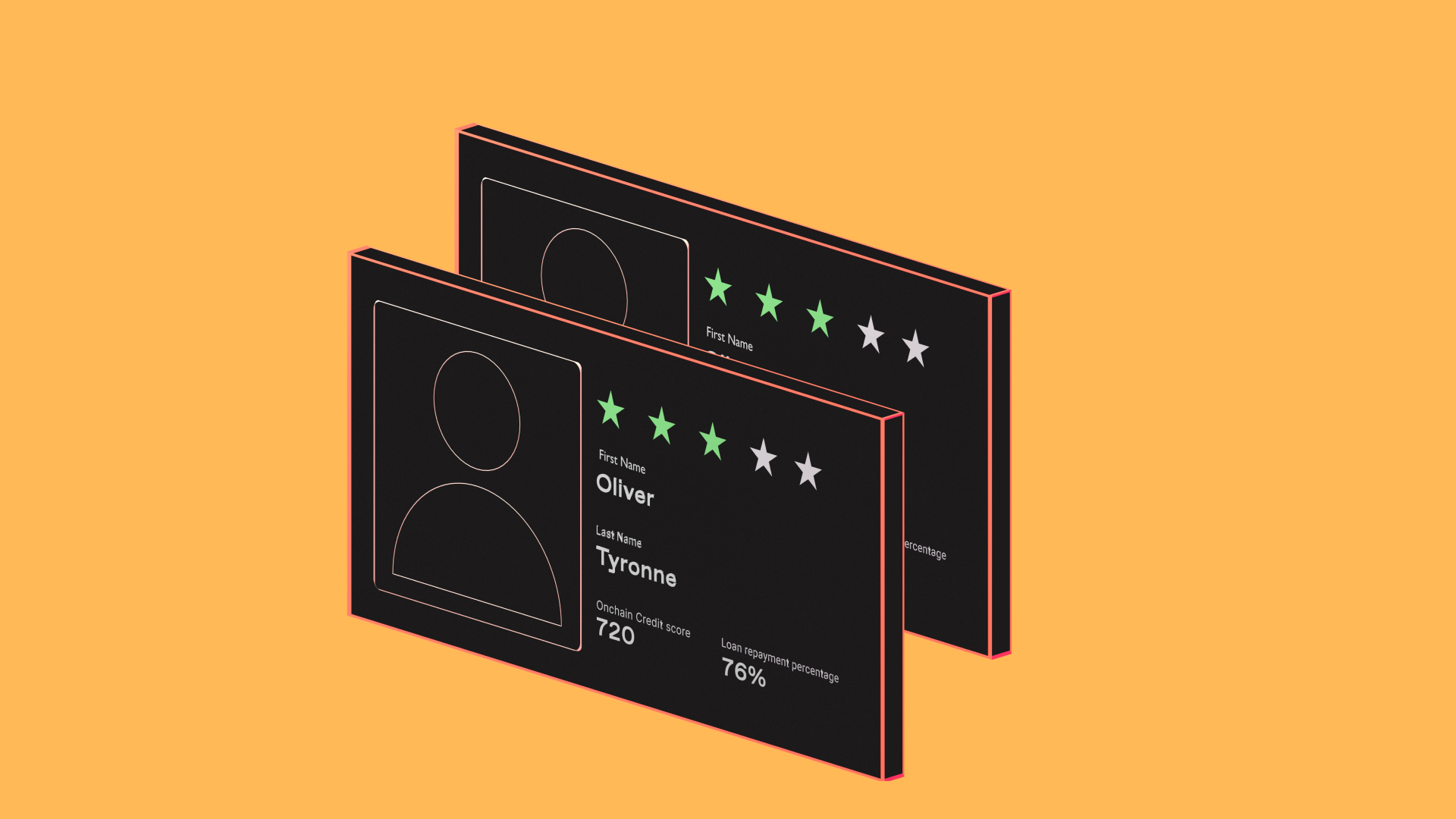

Building credit history on-chain

Building a verifiable credit history in decentralized finance requires treating blockchain transactions as a structured repayment ledger. Unlike traditional banking, where credit scores are derived from opaque internal algorithms, on-chain credit relies on transparent, immutable records of your collateralization behavior and repayment consistency.

To establish a credible on-chain identity, you must follow a disciplined approach to managing your positions. The following steps outline the structural mechanics of building a positive credit footprint.

Start by depositing high-quality collateral, such as ETH or USDC, into a lending protocol that reports to credit bureaus. This initial deposit creates your "credit line." The value of your collateral directly influences your borrowing power and initial risk profile. Use a

to monitor current market values, as volatility can impact your health factor.

Repay your loans on schedule. Even in over-collateralized systems, missing a payment or allowing a position to linger near liquidation thresholds signals risk to credit reporting agencies like TransUnion. Consistent, timely repayments are the primary data point used to calculate your on-chain credit score.

Liquidations are the equivalent of a default in traditional finance. They permanently damage your credit reputation on-chain. Maintain a healthy collateralization ratio by monitoring market conditions and adding margin when necessary. A

can help visualize volatility trends, though always refer to the specific asset you are holding.

Not all DeFi protocols report to external credit bureaus. Choose platforms that have partnerships with agencies like TransUnion or Chainalysis to ensure your positive history is recorded and accessible to traditional lenders. This bridges the gap between your on-chain activity and your off-chain financial identity.

Building this history is not instantaneous. It requires patience and disciplined management of your crypto assets. By treating your on-chain wallet as a financial instrument that requires maintenance, you can eventually access better lending rates and traditional credit products.

The Liquidation Risk in Crypto-Backed Lending

Crypto-backed loans are structured as secured debt, but the collateral is highly volatile. When Bitcoin or Ethereum prices drop, the value of the underlying assets can quickly fall below the loan-to-value (LTV) threshold set by the lender. This triggers an automatic liquidation, where the platform sells your collateral to cover the debt. Unlike traditional mortgages, these processes happen on-chain or in seconds, leaving little time for the borrower to react.

To understand the current exposure, we look at live market data. The following widgets show the real-time values of the two most common collateral assets. A sharp decline in these charts often precedes a wave of forced liquidations across CeFi and DeFi platforms.

The mechanics of credit scoring in this space rely heavily on these collateral buffers. In CeFi, centralized exchanges manage the risk internally, often using automated margin calls. In DeFi, smart contracts enforce liquidations instantly. If the market moves faster than the oracle data feeds, users may face "undercollateralization" penalties or slippage losses during the sale. This structural fragility means that even a short-term dip can result in the total loss of your crypto holdings, regardless of your eventual recovery.

Chainalysis data from 2026 highlights that liquidation events remain a primary vector for value loss in on-chain credit markets. Unlike traditional credit scores, which penalize late payments, crypto credit scores are often binary: you either maintain the collateral ratio, or you are liquidated. This all-or-nothing dynamic creates a high-stakes environment where risk management is not just about repayment ability, but about surviving market volatility.

No comments yet. Be the first to share your thoughts!