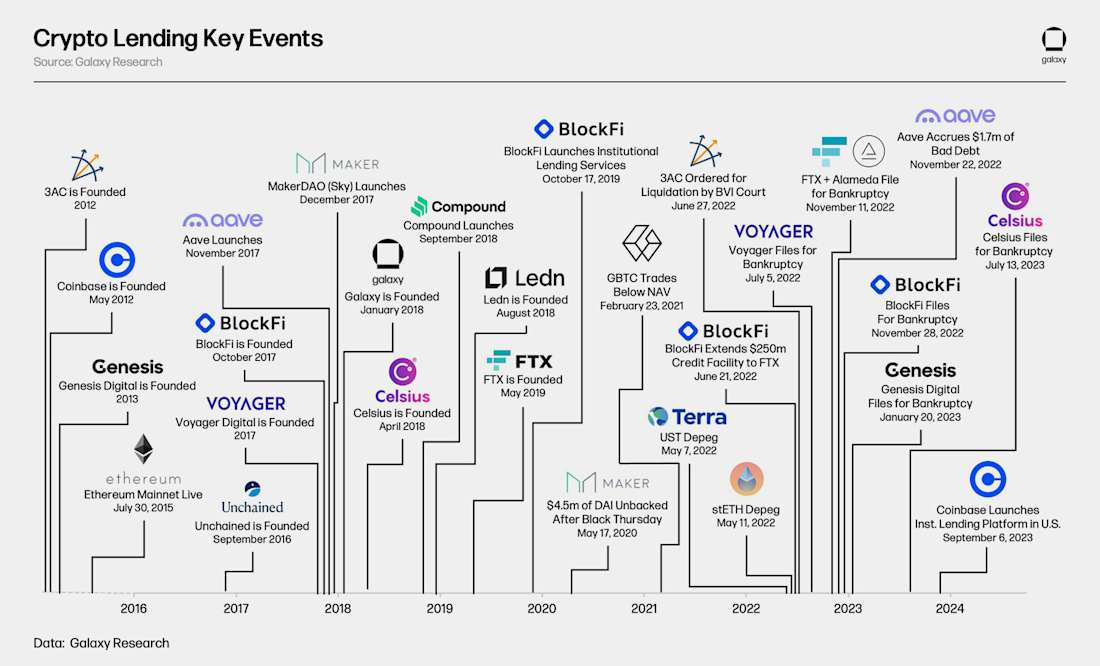

The 2026 shift from collateral to credit

The architecture of decentralized finance is undergoing a structural pivot. For years, the dominant model relied on over-collateralization, where borrowers locked up more value than they borrowed to mitigate risk. This approach removed traditional barriers like credit scores but created capital inefficiency and limited access for users without substantial on-chain assets. In 2026, the market is moving toward hybrid credit models that integrate off-chain and on-chain data to assess borrower risk more accurately.

This shift is driven by the need for more robust risk assessment frameworks. Pure collateralization, while secure, is inherently exclusionary. It prevents individuals with strong repayment histories but low asset holdings from participating in DeFi lending markets. By incorporating off-chain credit data—such as traditional credit bureau scores or verified income streams—protocols can offer unsecured or under-collateralized loans. This "crypto-native credit score" aims to bridge the gap in risk assessment, rendering DeFi lending more inclusive without compromising protocol solvency.

The integration of these data sources requires careful regulatory and technical consideration. Off-chain data must be verified through trusted oracles or decentralized identity protocols to prevent fraud. The goal is not to replace collateral entirely but to supplement it with a more nuanced view of borrower reliability. This evolution marks a departure from the binary security of pure over-collateralization toward a more sophisticated, credit-based economy.

How on-chain credit reporting works

Traditional credit scoring relies on centralized bureaus that aggregate data from banks and lenders. In the decentralized finance (DeFi) ecosystem, this infrastructure does not exist. Instead, a crypto-native credit score is derived directly from on-chain data, offering a transparent but distinct method of risk assessment. This approach replaces the opaque black box of traditional credit reporting with public ledger history, allowing protocols to evaluate counterparty risk without relying on a centralized identity provider.

The mechanics of this scoring system hinge on wallet history and transaction behavior. Aggregators and rating agencies analyze on-chain metrics such as wallet balances, asset flows, reserve composition, and historical transaction patterns. Unlike a FICO score, which penalizes late payments on a credit card, a crypto credit score often rewards liquidity provision and consistent repayment of on-chain loans. It treats the blockchain wallet as a financial entity, assessing its stability and reliability based on its digital footprint.

This shift from centralized to decentralized data collection fundamentally changes how risk is measured. It bridges the gap in risk assessment for DeFi lending, rendering the ecosystem more robust and inclusive for users who lack traditional credit histories. However, it also introduces new complexities. The lack of regulatory standardization means that different protocols may interpret on-chain data differently, leading to varied credit assessments for the same wallet. As the market matures, the industry is moving toward more standardized metrics to ensure that these scores accurately reflect true counterparty risk.

How On-Chain Credit History Lowers DeFi Lending Costs

Verified on-chain credit reporting fundamentally alters the risk calculus for decentralized finance (DeFi) lending protocols. By integrating traditional credit data—such as TransUnion scores—into the on-chain identity layer, lenders can distinguish between borrowers who are merely over-collateralized and those who demonstrate a history of financial reliability. This distinction allows protocols to price risk more accurately, moving beyond the blunt instrument of fixed collateral ratios.

The primary impact is a direct reduction in interest rates for credit-worthy borrowers. In a standard over-collateralized loan, the interest rate is often static, determined solely by the volatility of the underlying asset (e.g., Bitcoin or Ethereum). However, when a borrower’s credit history is verified, the protocol can offer a tiered pricing model. A borrower with a high credit score and a clean on-chain repayment history may qualify for a lower annual percentage rate (APR), as the perceived risk of default decreases. This creates a financial incentive for responsible borrowing behavior, aligning traditional credit discipline with decentralized asset management.

Beyond lower APRs, verified credit history enables higher Loan-to-Value (LTV) ratios. Typically, DeFi loans require borrowers to lock up 150% or more of the borrowed value to protect against market volatility. With a strong credit profile, protocols can reduce this buffer, allowing borrowers to access more liquidity against the same collateral. This efficiency is critical for institutional players and high-net-worth individuals who seek to leverage their crypto assets without tying up excessive capital.

The following table compares standard collateralized loans against credit-scored loans, highlighting the differences in LTV and APR based on borrower profile.

| Feature | Standard Over-Collateralized | Credit-Scored Loan |

|---|---|---|

| LTV Ratio | 50-70% | Up to 90% |

| APR Range | Fixed (e.g., 5-10%) | Tiered (e.g., 3-8%) |

| Collateral Type | Crypto Assets Only | Crypto + Credit History |

| Approval Speed | Instant | Minutes (Verification) |

| Risk Assessment | Asset Volatility | Asset + Borrower Credit |

This shift toward credit-based lending introduces a new layer of complexity to DeFi. While it offers significant cost savings and liquidity benefits, it also requires robust data verification to prevent fraud. Protocols must ensure that credit scores are accurately reported and that on-chain behavior aligns with off-chain credit data. As this model matures, we expect to see more protocols adopt hybrid lending structures that balance the anonymity of DeFi with the accountability of traditional credit systems.

Key players in crypto credit scoring

The landscape for on-chain credit reporting is split between legacy financial institutions and native Web3 protocols. Traditional agencies like TransUnion are entering the space by providing off-chain credit data to blockchain-based lending protocols, allowing users to apply for loans without compromising their privacy. This integration bridges the gap between traditional creditworthiness and decentralized finance (DeFi) lending rates.

Simultaneously, specialized Web3-native providers are building credit scores directly from on-chain activity. Projects like Cred Protocol and ARCx analyze transaction history, wallet age, and asset holdings to generate risk scores. These scores are designed to be portable across different ecosystems, offering a more dynamic view of a user’s financial health than static traditional reports.

The following providers are currently leading the market in credit scoring infrastructure:

Major Credit Scoring Providers

-

TransUnion

A traditional credit bureau partnering with DeFi protocols to integrate off-chain credit scores into on-chain lending decisions. -

ARCx

A Web3-native platform that aggregates on-chain data to provide comprehensive credit scores and risk assessments for crypto assets. -

Cred Protocol

Focuses on decentralized credit scoring, allowing users to build and use their on-chain reputation for borrowing and lending.

This convergence of traditional and decentralized scoring models is reshaping how credit is assessed in the digital asset space, offering users more options for accessing capital while managing risk.

Bitcoin price and lending market trends

Bitcoin's market trajectory directly influences the liquidity and risk parameters of crypto-backed lending. When BTC prices stabilize or rise, lenders perceive lower collateral risk, which often compresses borrowing rates. Conversely, sharp drawdowns trigger margin calls and tighten credit availability across decentralized finance (DeFi) protocols.

The following chart illustrates the recent volatility in Bitcoin's price action, a primary driver of lending market sentiment.

This price volatility dictates the Loan-to-Value (LTV) ratios lenders are willing to offer. In 2026, as on-chain reporting becomes more standardized, lenders can better assess borrower behavior beyond simple collateralization. This shift allows for more nuanced risk pricing, linking Bitcoin's macro performance directly to individual DeFi lending rates.

How on-chain activity affects your credit profile

Buying or trading cryptocurrency does not directly appear on standard credit reports. Traditional credit bureaus do not track wallet addresses or decentralized exchange transactions. Your on-chain history remains invisible to legacy scoring models unless you voluntarily link that data through a specialized reporting service.

The relationship between DeFi activity and credit scores hinges on whether a protocol reports your repayment behavior. Some on-chain credit building platforms submit positive payment history to major bureaus. If you fail to repay a DeFi loan or a crypto-backed line of credit, that default may be reported, potentially damaging your score.

Privacy concerns are valid but manageable. On-chain data is public by default, but credit reporting agencies only receive the data you or your lender explicitly submit. You are not required to disclose your entire transaction history. However, if you use a service that aggregates your on-chain activity to build a credit file, that specific dataset becomes part of your credit report.

No comments yet. Be the first to share your thoughts!