On-chain credit scoring is shaking up the world of DeFi lending, offering a tantalizing vision: crypto loans with less collateral, powered by blockchain transparency and algorithmic trust. But as more capital flows into under-collateralized lending protocols, so do the risks. Security concerns are front and center for anyone navigating this new frontier. Let’s break down the top five threats you need to know about if you’re building, borrowing, or investing in on-chain credit systems.

Sybil Attacks and Identity Fraud: The Achilles’ Heel of Decentralized Identity

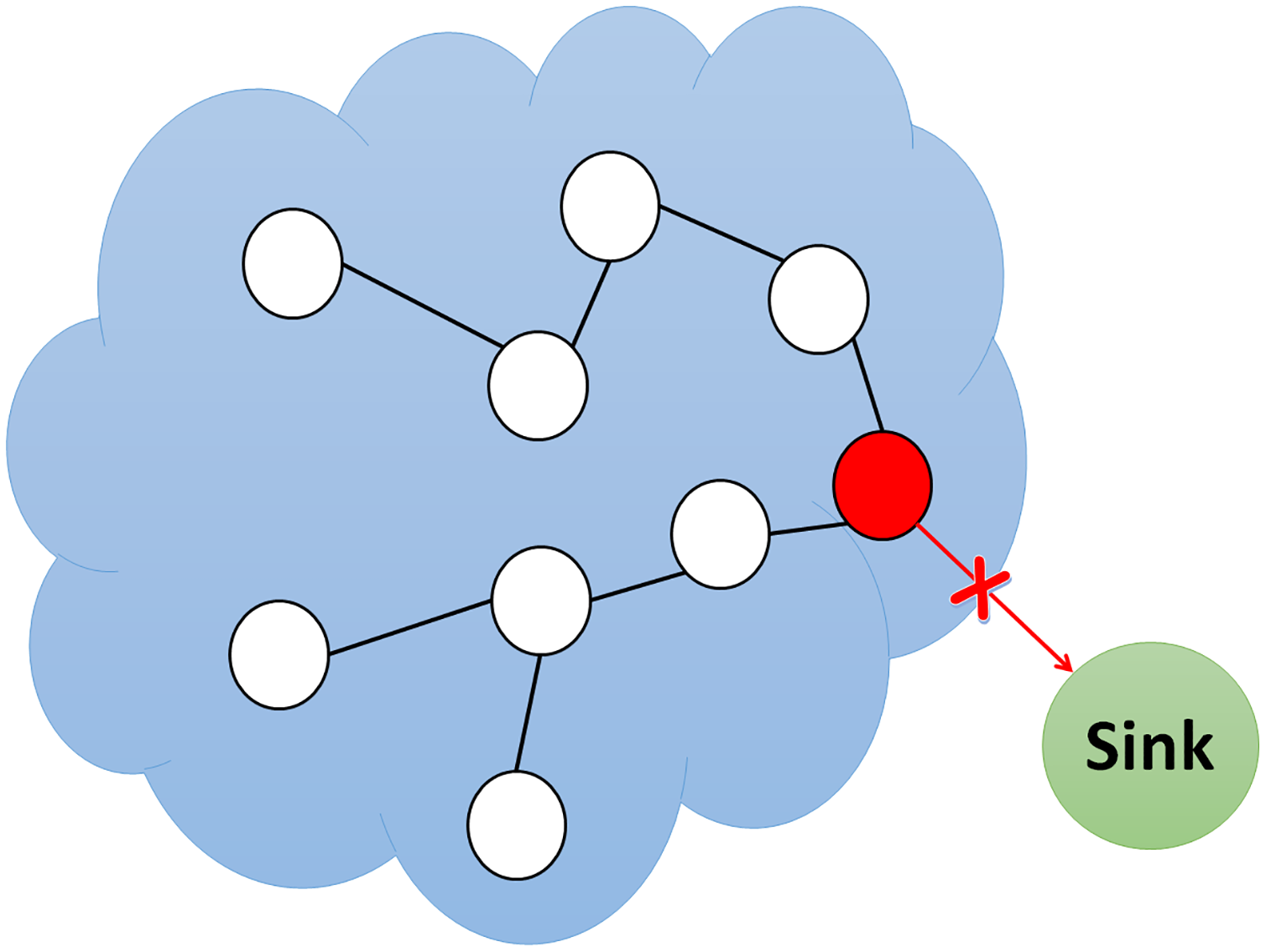

The promise of decentralized identity (DID) is huge for DeFi, but it’s also a double-edged sword. In an ideal world, DID lets users build reputation without revealing their real-world identity. In reality, attackers can spin up countless wallet addresses or game DID frameworks to impersonate multiple unique users. This is known as a Sybil attack. The risk? A single bad actor could access dozens (or hundreds) of under-collateralized loans with no intent to pay back, draining liquidity pools and eroding trust in on-chain credit scores.

"Decentralization offers privacy, but also makes it harder to spot fraudsters gaming the system. "

Protocols are experimenting with everything from social graph analysis to cross-chain identity proofs to fight Sybil attacks, but no solution is bulletproof yet. If you’re a lender or developer in this space, vigilance and layered defenses are non-negotiable.

Flash Loan Exploits: Instant Capital, Instant Chaos

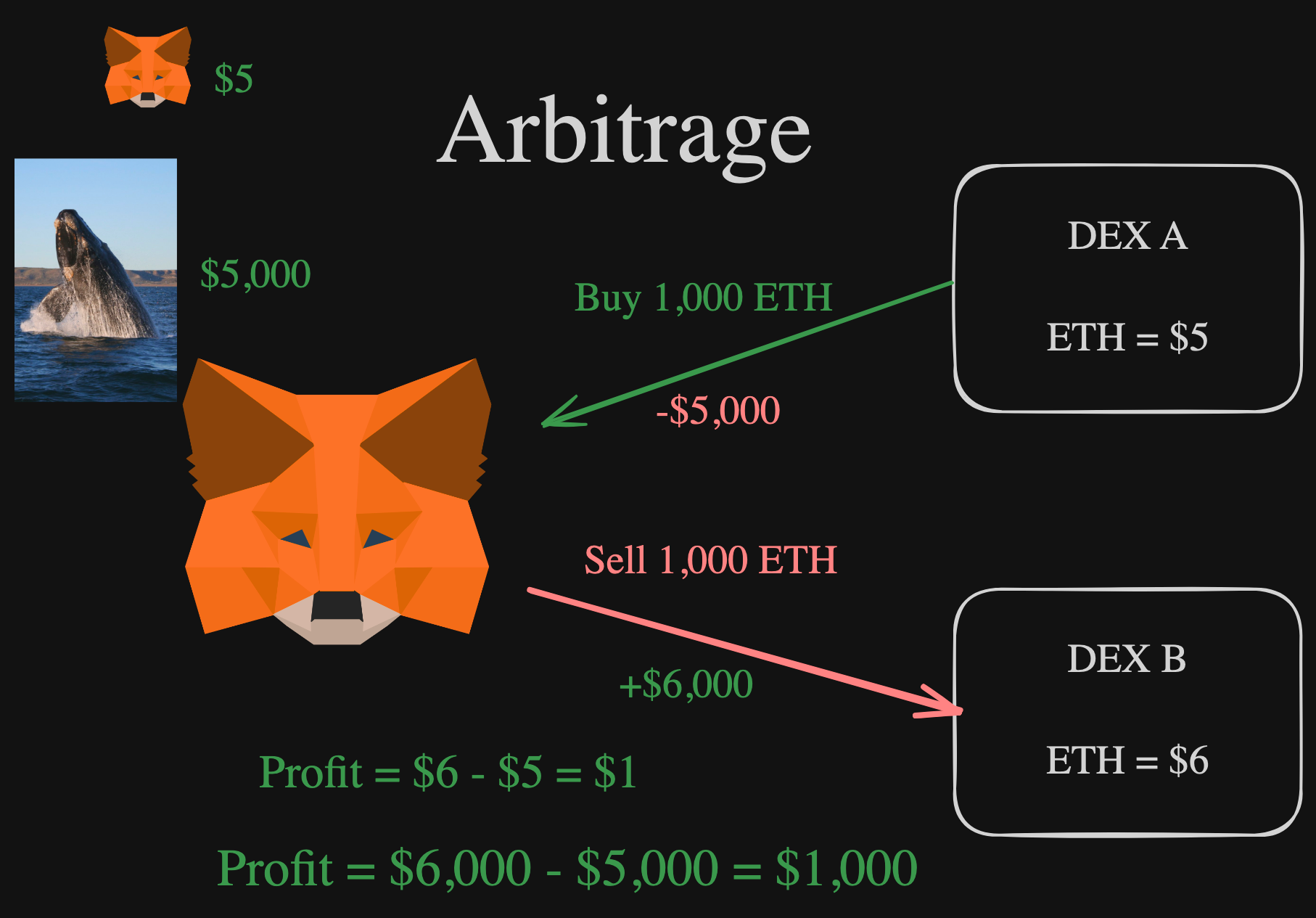

Flash loans have become infamous in DeFi security circles, and for good reason. These zero-collateral loans let anyone borrow massive sums instantly if they repay within a single transaction block. Malicious actors use flash loans to manipulate protocol logic or exploit vulnerabilities at lightning speed.

When it comes to on-chain credit scoring risks, flash loan exploits can be catastrophic. Attackers might artificially inflate their credit score by temporarily boosting wallet balances or orchestrating fake repayments, all funded by capital they never actually own. Or worse: they might target flaws in lending protocol smart contracts themselves, causing cascading liquidations or draining entire pools before anyone catches on.

Data Manipulation and Gaming Credit Scores

The transparency of blockchain means all your repayment history is out there for anyone (and any algorithm) to see. That’s great for accountability, but it also opens the door for sophisticated data manipulation schemes.

Borrows can coordinate wash borrowing/repayment cycles across multiple wallets or protocols in order to artificially boost their on-chain reputation. This gaming of the system creates false positives: users who appear trustworthy on paper but have never taken real risk or demonstrated genuine repayment behavior.

Common Ways Borrowers Game On-Chain Credit Scores

- Sybil Attacks and Identity Fraud: Attackers create multiple fake wallet addresses or manipulate decentralized identity (DID) systems to obtain under-collateralized loans with no intention of repayment. This undermines the reliability of on-chain credit scores and makes it difficult for lenders to assess true risk.

- Flash Loan Exploits: Malicious actors leverage flash loans to manipulate on-chain credit scoring models or exploit vulnerabilities in lending protocols. These attacks can result in rapid, large-scale losses without requiring any upfront capital, as seen in high-profile DeFi incidents.

- Data Manipulation and Gaming Credit Scores: Borrowers may artificially inflate their on-chain repayment histories or coordinate wash borrowing/repayment cycles. This creates misleadingly high credit scores, giving lenders a false sense of borrower reliability.

- Smart Contract Vulnerabilities: Bugs or exploits in smart contracts that manage credit scoring and loan issuance can be targeted by hackers. This can lead to loss of funds or unauthorized access to sensitive user data, as highlighted by several DeFi protocol breaches.

- Privacy Risks and Data Exposure: The transparency of blockchain data means sensitive financial behaviors and identities could be deanonymized. This exposes users to targeted attacks, phishing, or regulatory scrutiny, raising serious privacy concerns.

Lenders relying solely on these scores may be misled about true borrower quality, potentially leading to higher default rates and instability across under-collateralized loan markets.

Smart Contract Vulnerabilities: Code Is Law… Until It Isn’t

No discussion about security in DeFi lending would be complete without talking about smart contract bugs and exploits. On-chain credit scoring systems live and die by their code; if that code has flaws, hackers will find them.

A single unchecked vulnerability could allow unauthorized access to sensitive user data, or even let attackers mint fraudulent credit scores and siphon funds from lending pools. The history of DeFi is littered with high-profile hacks exploiting smart contract weaknesses (see flash loan attacks here). Rigorous audits are essential, but even then, no contract is 100% immune from creative exploits as attack surfaces keep evolving.

Beyond technical flaws, composability in DeFi means that even a minor bug in a single contract can ripple through interconnected protocols, amplifying risk. For under-collateralized loan platforms, where trust hinges on accurate and secure credit scoring, a smart contract exploit can be devastating, wiping out user funds and damaging protocol reputation overnight.

Privacy Risks and Data Exposure

One of the paradoxes of blockchain risk management is that the very transparency enabling open credit scoring also creates privacy hazards. On-chain activity is public by default. As DeFi matures, sophisticated analytics can link wallet addresses to social profiles, IPs, or even real-world identities. This raises the stakes for users seeking under-collateralized loans: not only are your financial behaviors visible, but you could also become a target for phishing attacks or regulatory scrutiny if your activity is deanonymized.

Privacy-preserving technologies like zero-knowledge proofs are making headway (learn more here), but until these tools are widely implemented, borrowers and lenders must be aware that sensitive data exposure remains a critical concern in on-chain credit environments.

Stay Safe: Your Step-by-Step Guide to Secure On-Chain Credit Scoring

The Path Forward: Balancing Innovation with Security

The drive toward open finance is unstoppable, but it demands vigilance. Platforms need robust identity frameworks to counter Sybil attacks, advanced analytics to spot wash trading and score manipulation, continuous smart contract audits, and thoughtful privacy protections at every layer. Lenders should diversify their risk and never rely solely on algorithmic scores without human oversight.

For borrowers, understanding these risks isn’t just about protecting your identity, it’s about building genuine reputation capital that will outlast market cycles and protocol upgrades.

The bottom line? On-chain credit scoring risks aren’t just theoretical, they’re shaping the future of decentralized lending right now. Stay informed, stay cautious, and remember: code may be law in DeFi, but trust is still earned block by block.

No comments yet. Be the first to share your thoughts!